CATEGORY

Getting started

Elon Taking SpaceX Public! $100 Pre-IPO Opportunity Open

Below is an important message from one of our sponsors.

Please read it carefully as they have some special information to share with you.

Dear Reader,

When SpaceX goes public next year…

It’s expected to be the biggest IPO in HISTORY…

As high as $1.5 TRILLION by some estimates.

That is an eye-watering amount of money…

And Wall Street insiders are salivating at the thought of SpaceX’s IPO.

But the best part…

You can get a piece of this SpaceX action before it goes public…in a regular brokerage account.

All thanks pre-IPO play almost no one’s talking about…

And if you act fast, you can get in position for LESS than $100.

Click here NOW for the full story.

But don’t wait…

As soon as word of this opportunity gets out, it could be too late…

And you could miss out on your chance to profit from the biggest IPO in history.

Click here before it’s too late.

Best,

Matt Insley

Publisher, Paradigm Press

This ad is sent on behalf of Paradigm Press, LLC, at 1001 Cathedral St., Baltimore, MD 21201. If you’re not interested in this opportunity from Paradigm Press, LLC, please click here to remove your email from these offers.

P.S. – If you no longer want to receive occasional emails from us and you want to unsubscribe, click here 👉 “Unsubscribe” . Thank you!

The Quiet Billion-Dollar Noise

Don’t forget to cast your vote 👇

Okay — quick thought experiment.

It’s 8:17 p.m.

You open your phone.

You ask ChatGPT something dumb.

You get an answer in seconds.

Feels instant and frictionless.

What you don’t see is the army of servers, power plants, cooling systems, and transmission lines working overtime to make that answer appear.

Somewhere, a transformer is sweating.

Somewhere, a data center is drawing enough power to run a small city.

Somewhere, a local grid operator is praying nothing trips.

There’s actually a technical reason for this — and it has nothing to do with “AI being smart.”

It’s called compute demand.

And right now, it’s growing faster than our power grids.

The Setup

AI is starting to follow a predictable path.

Phase 1: Build giant campuses where land is cheap.

Phase 2: Move compute closer to people, because latency is a product feature.

That’s why the story is shifting.

This is no longer a story about chips or chatbots.

It’s a story about the grid, water, tax deals, and communities asking the obvious question:

Who’s paying for this?

This week gave us the cleanest snapshot yet:

Rural Louisiana. Downtown Chicago. Suburban Indiana.

SPONSOR BREAK presented by TheOxfordClub*

A U.S. “birthright” claim worth trillions – activated quietly

A tiny government task force working out of a strip mall just finished a 20-year mission.

And with almost no media coverage, they confirmed one of the largest U.S. territorial expansions in modern history…

A resource claim worth an estimated $500 trillion.

Thanks to sovereign U.S. law, this isn’t just a national asset.

It’s an American birthright.

That means every citizen now has the legal right to stake a claim…

But very few even know the opportunity exists.

If you want to see how you can get in line for your portion of this record-breaking windfall…

I’ve assembled everything you need to see inside a new, time-sensitive briefing:

Get all the details here – while the claim window remains open.

The Maps

Rural: The Titan Clusters

Meta’s Hyperion project in Richland Parish, Louisiana is the cleanest example of how this game gets played.

A small parish (~20k people) approves financing terms quietly.

The developer is a shell entity (Laidley LLC).

The project has a code name (“Project Sucre”).

A few months later, it’s revealed: this is Meta.

Meta says Hyperion’s first phase opens in 2028, with $10B+ of investment. Zuckerberg has described it as 2GW+ and “large enough to cover a significant part of Manhattan,” with a long-term path to 5GW.

The key detail isn’t the size. It’s leverage.

Louisiana’s incentive package is designed to remove friction:

→ Sales tax exemptions on data center equipment (GPUs, networking, cooling)

→ Public support for power infrastructure expansion.

→ Long-dated power commitments.

Sherwood estimated the GPU sales tax break alone could be $3.3B — big enough to fund years of state-level budgets.

And the jobs math is the part everyone learns too late:

peak construction: 5,000+ skilled trade roles

operations after completion: around 500 full-time jobs

The result on the ground looks like an economic boom … but also:

→ Farmland prices jumping from roughly $6,500/acre to $30,000+, with listings cited as high as $73,000/acre

→ Home prices in the parish up sharply year-over-year.

… rising questions about who really benefits.

This is the “AI factory” pitch: big spend, big excitement, then a smaller steady-state footprint than the headlines implied.

Urban: Inference Comes Downtown

Today’s Chicago story is the pivot.

A former Chicago Board Options Exchange trading floor is being converted into a 33-megawatt data center, set to open later this year.

Pause there — because this is not what people picture when they think “AI data centers.”

This is not a rural, miles-wide “titan cluster.” It’s the opposite.

This is edge compute. This is inference. This is the layer that sits close to users.

Here’s the clean way to understand the difference:

Training = building the brain.

It can happen far away, on massive campuses, where land is cheap and power is abundant.Inference = using the brain.

That has to happen near people, because speed matters.

Why? Because with AI, latency is the product.

If your AI takes 15 seconds to respond, you’ll use it less.

If it responds instantly, you’ll use it all day.

So the industry is calling 2026 the “inversion year” — the moment when more compute is spent on inference than on training.

❗If that shift is real, the real estate map changes.

Suddenly, Downtown real estate got a new use case.

✓ Vacant offices?

✓ Old industrial sites?

✓ Half-empty “powered shells”?

They’re no longer leftovers.

They’re prime inventory for AI.

SPONSOR BREAK presented by TheOxfordClub*

How Mitt Romney Turned $450K Into Up to $100 Million (Tax-Free)

It wasn’t stocks. It wasn’t real estate. It was a little-known investment vehicle that turned Mitt Romney’s $450,000 into as much as $100 million and Peter Thiel used to turn $2,000 into $5 billion within two decades. Now, thanks to a new executive order, regular Americans can access the same type of investment.

Get more details here >>

Suburban: “Social Cost”

Meta’s Indiana announcement is basically the community-relations version of Louisiana.

Lebanon, Indiana is getting a 1-gigawatt data center — a $10B+ project that slots into Meta’s plan to spend up to $135B on AI in 2026 (after ~$72B in 2025).

But the real story is the terms.

This time, Meta showed up with a checkbook, not just a slide deck:

→ It says it will pay the full cost of the energy it uses.

→ $1M per year for 20 years to a community fund for energy bills.

→ A closed-loop water system that supposedly uses “no water most of the year.”

→ $120M+ for local water infrastructure.

→ Upgrades to roads, transmission lines, and local utilities.

Plain English: Meta isn’t just building a data center — it’s pre-paying the backlash.

That’s the new playbook.

source: NPR

Companies are now underwriting the “social cost” up front because otherwise projects get delayed, downsized, or canceled.

And cancellations are no longer theoretical — developers have already started walking away from projects when resistance and regulatory friction stack up.

The Market Angle

All of this — Hyperion in Louisiana, edge sites in Chicago, and Meta’s concessions in Indiana — points to the same reality:

AI is becoming an infrastructure story.

And infrastructure stories are capex stories.

That’s why markets are suddenly less interested in what AI can do in theory, and much more focused on what it costs.

Which brings us to Microsoft.

Microsoft…

Why did Microsoft ( ▼ 2.2% ) sell off after what looked like “good” earnings?

The simplest answer: capex became the product.

Microsoft beat on the numbers that usually matter — revenue and EPS.

But then it disclosed $37.5B in quarterly capex, largely tied to AI infrastructure.

The market’s reaction was: “The payoff is probably real… but the timeline isn’t clear — and the spending is very front-loaded.”

That’s a different kind of risk.

So the selloff read more like a repricing of certainty.

From a trading lens, that matters:

The stock snapped back from oversold levels — classic mean reversion after a violent move.

But it’s still below its 200-day moving average, with no clean base yet.

In trader terms: mean reversion is not trend reversal.

The bigger takeaway is this:

Microsoft isn’t being punished for betting on AI.

It’s being stress-tested for how fast and how much it has to spend to win.

SPONSOR BREAK presented by BanyanHill*

President Trump Just Privatized The U.S. Dollar

A controversial new law (S.1582) just gave a small group of private companies legal authority to create a new form of government-authorized money.

Today, I can reveal how to use this new money… why it’s set to make early investors’ fortunes, and what to do before the wealth transfer begins on February 17 if you want to profit.

Go here for details now — while you still have time to position yourself.

NVIDIA: The Bar Is Set High

Zoom out.

Microsoft is being re-rated because AI capex is front-loaded.

Nvidia’s ( ▲ 0.8% ) upside now depends on that capex actually getting built.

Which is why the battles over data centers in Louisiana, Chicago, and Indiana are the bottleneck in Nvidia’s bull case.

Goldman’s message on Nvidia is simple: Yes, they expect a beat.

They’re modeling roughly $2B of upside to consensus in the current quarter.

But that’s not what will move the stock.

What matters isn’t what Nvidia already earned — it’s how confident investors feel about demand lasting beyond this year.

The debate narrowed to:

→ How durable is that demand?

→ How much share leaks to ASICs or AMD?

→ How smoothly does the Rubin ramp go?

→ And what happens with China?

The question is:

How much of that future is already in the price — and how much is still optionality?

That’s why the bar feels high.

If Nvidia simply meets expectations, the market shrugs.

If it gives clearer visibility into 2027, the stock has fuel.

If anything looks shaky, investors will punish it fast.

So…

AI used to be a story about brains and chips.

Now it’s a story about concrete, power lines, and permits.

That’s why Microsoft got hit on “good” earnings — the bill arrived before the payoff.

And it’s why Nvidia’s bar is so high — its upside depends on all this infrastructure actually getting built.

In other words:

the AI boom is on a construction schedule.

Lesson of the Day

💬 We Want To Hear Your Story:

Got a market or stock you want us to analyze next?

Just drop your request in the comments here.

Was this email forwarded to you? Don’t miss out on future stories — subscribe to the TradingLessons and get our daily market breakdown delivered straight to your inbox.

❗ P.S. – If you no longer want to receive occasional emails from us and you want to unsubscribe, click here 👉 “Unsubscribe” . Thank you!

Big Pharma vs. Big Loophole

Don’t forget to cast your vote 👇

It is a Super Bowl Enigma.

source: sherwood

Last night, millions of people stared at “LX” and quietly Googled what it meant.

LX.

A quick refresher for anyone who needed it: L is 50, X is 10 — which makes Super Bowl LX simply Super Bowl 60.

The small lesson in that moment is useful: the things that look simple often aren’t.

Which brings us to today’s story:

So… about what happened in healthcare today.

While we were still digesting the Super Bowl weekend, Danish pharma giant Novo Nordisk sued Hims & Hers, accusing the telehealth company of infringing a key patent on semaglutide — the active ingredient in Ozempic and Wegovy.

The stock screen told part of the story:

Hims ( ▼ 16.03% ) shares were down roughly 20% premarket.

Novo ( ▲ 3.63% ) initially popped nearly 6%, before giving some of that back.

Hims has built a big part of its business inside a legal gray zone and now that gray zone is being tested in court.

Which raises a bigger question we’ll come back to:

When does “disruption” turn into “infringement”?

And that’s where today’s story begins.

When A Blockbuster Meets A Copycat

For three years, Novo Nordisk looked untouchable.

Wegovy and Ozempic turned weight loss into a trillion-dollar market. Semaglutide became a household word. At one point, Novo even became Europe’s most valuable company.

Then January hit — and the story started to wobble.

→ Novo warned that 2026 sales could fall by as much as 13%.

→ Pricing pressure in the U.S. intensified.

→ Eli Lilly kept gaining ground.

And the patent clock quietly grew louder in the background.

That’s when Hims & Hers decided to test the guardrails.

Last week, Hims rolled out a $49-a-month copy of Novo’s brand-new Wegovy pill — just days after the FDA approved it.

Novo’s version? $149.

In plain English:

Hims tried to beat Novo to consumers with a much cheaper version of a drug that had barely even reached the market.

The reaction was immediate.

→ Novo’s stock sold off.

→ Hims’ stock whipsawed.

And regulators suddenly got very interested.

Within hours, the FDA said it would take “decisive steps” against illegal copycat GLP-1 drugs.

By Friday, HHS had referred Hims to the DOJ.

By Saturday, Hims pulled the pill.

By Monday, Novo filed a lawsuit.

SPONSOR BREAK presented by BanyanHill*

President Trump Just Privatized The U.S. Dollar

A controversial new law (S.1582) just gave a small group of private companies legal authority to create a new form of government-authorized money.

Today, I can reveal how to use this new money… why it’s set to make early investors’ fortunes, and what to do before the wealth transfer begins on February 17 if you want to profit.

Go here for details now — while you still have time to position yourself.

The Pill Problem

Here’s the part most headlines skipped.

→ Making a GLP-1 injection is hard.

→ Making a GLP-1 pill is much harder.

Your stomach is basically designed to destroy proteins like semaglutide, so simply putting the drug in a tablet doesn’t work. To get around that, Novo spent $1.8 billion to buy Emisphere Technologies and its SNAC coating — a proprietary system that protects the drug long enough for it to be absorbed.

That took years of trials, specialized technology, and real clinical data.

Hims took a different route. Its pill relied on “liposomal technology,” but there’s no publicly available human trial data backing it — mostly just animal studies. One expert even said the approach amounted to “quasi-clinical trials on people.”

In short:

→ Novo engineered a proven way to make semaglutide work as a pill.

→ Hims tried to engineer a cheaper workaround — and crossed its fingers that regulators would look the other way.

The Loophole That Made This Possible

So how was Hims able to do this in the first place?

It comes down to a regulatory loophole.

When a drug is officially in shortage, specialty pharmacies are allowed to “compound” — meaning they can legally make customized versions for patients who can’t access the branded product. In 2024, GLP-1 drugs were in short supply, and Hims built a significant part of its business around that gap.

Even after the shortage ended, the company continued selling what it called “personalized” versions.

That argument was already shaky for injectable drugs. For pills, it’s even weaker — tablets are produced in batches, not tailored to individual patients.

Novo has been frustrated for months that regulators didn’t move sooner.

Now, they finally are.

SPONSOR BREAK presented by TheOxfordClub*

How Mitt Romney Turned $450K Into Up to $100 Million (Tax-Free)

It wasn’t stocks. It wasn’t real estate. It was a little-known investment vehicle that turned Mitt Romney’s $450,000 into as much as $100 million and Peter Thiel used to turn $2,000 into $5 billion within two decades. Now, thanks to a new executive order, regular Americans can access the same type of investment.

Get more details here >>

This Isn’t Just NOVO vs. HIMS

At its core, this fight isn’t really about two companies.

It’s about three forces colliding in the same market.

→ On one side are patents — Novo’s legal moat and the foundation of its power.

→ On another is price — Hims’ appeal to consumers who want cheaper, easier access.

And overseeing it all is regulation — the referee that ultimately decides what’s allowed.

If Novo prevails, it keeps its pricing power and tight control over the GLP-1 market.

If Hims prevails, it opens the door to cheaper alternatives and chips away at Big Pharma’s dominance.

Markets already started pricing both possibilities last week.

Novo erased much of its post-Wegovy gains.

Eli Lilly continued to pull ahead with stronger guidance.

And Hims got hit hard — but in doing so, it demonstrated just how massive the demand really is.

So…

The math was simple.

Hims: $49 per month.

Novo: $149 cash-pay.

Consumers loved it. Investors flinched. Novo moved.

Today, Novo sued Hims over its copy of Wegovy — not just the pill, but potentially its injectables too.

What looks like a pricing battle is really something deeper:

If cheaper copies are allowed to scale, Novo’s blockbuster economics weaken.

If regulators shut them down, access shrinks and prices stay high.

That’s the tension at the heart of this fight.

Lesson of the Day

💬 We Want To Hear Your Story:

Got a market or stock you want us to analyze next?

Just drop your request in the comments here.

Was this email forwarded to you? Don’t miss out on future stories — subscribe to the TradingLessons and get our daily market breakdown delivered straight to your inbox.

❗ P.S. – If you no longer want to receive occasional emails from us and you want to unsubscribe, click here 👉 “Unsubscribe” . Thank you!

AI-Layoff Excuse

Don’t forget to cast your vote 👇

So… about yesterday’s market.

After a week that felt held together with tape, Friday snapped back hard.

The Dow ripped past 50,000 for the first time ever.

The S&P 500 jumped nearly 2%. The Nasdaq followed.

Big Tech led the bounce — Nvidia +8%, Broadcom up big, Tesla higher — even as Amazon sank on plans to spend even more on AI.

Crypto bounced too: Bitcoin climbed back above $70K after plumbing 16-month lows. Strategy (MSTR) whipsawed, then finished sharply higher.

On paper, it looked like “risk is back.”

Underneath, it felt more like relief than conviction.

While markets were whipsawing, layoffs were hitting the worst January since 2009 — and many of them were explicitly tied to “AI.”

And here’s the disconnect.

Markets are trying to price an AI boom…

while companies are cutting people in the name of AI.

Which brings us to today’s story.

The Narrative:

In 2023–2024, that story was:

AI was inevitable. Spending was virtuous. Markets rewarded ambition.

Boards signed off. CFOs loosened the purse strings. Investors applauded louder with every new data center and every bigger CapEx number.

It was clean, simple, and comforting.

Then 2025-2026 arrived — and the narrative shifted.

Now the headline version is different:

AI is “eliminating jobs.”

You see it everywhere. It has become the neat, modern explanation for why tens of thousands of people are losing work.

But here’s the tension that doesn’t make the headlines:

If AI is truly replacing workers at scale…

you should see it clearly in productivity and profits.

Right now, you don’t.

So something doesn’t quite line up.

The Headline vs. The Reality

If you just read the headlines, the story sounds simple:

AI is here.

Jobs are disappearing.

Last month, Challenger, Gray & Christmas put a number on it:

Nearly 55,000 U.S. job cuts in 2025 were officially attributed to AI —

a 13× jump from when they first started tracking that category.

Corporate America leaned into that language:

Pinterest trimmed ~15% of staff, citing an “AI-forward approach.”

Dow Chemical announced 4,500 cuts while leaning into “AI and automation.”

Amazon cut 16,000 jobs, extending last year’s reductions.

Microsoft, Meta, and Salesforce all linked layoffs to “AI-driven efficiency.”

If you stopped there, you’d think the robots are already running the show.

But that’s where the story gets slippery.

SPONSOR BREAK presented by Porter&Co*

The #1 Way To Play Gold Right Now

We’re witnessing the greatest gold rush in over 50 years…

But one gold asset has outperformed miners, typical stocks, and gold itself for the last two decades.

Click to discover this little-known gold investment now

The Excuse

Oxford Economics looked at the same data… and came back with a very different read.

Their January report basically said:

AI probably isn’t killing jobs the way headlines suggest.

Why? Because if AI were actually replacing workers at scale, you’d expect a clear jump in productivity.

You don’t see that.

Their implication is blunt: Saying “AI did this” sounds better to investors than admitting weak demand or pandemic-era overhiring.

Yale’s Budget Lab backed that up.

Their analysis found that employment patterns still look mostly like they did before the AI boom — not like a labor market being radically reshaped by machines.

A December Harvard Business Review survey of 1,000+ executives showed exactly that:

60% have already reduced headcount in anticipation of AI

29% slowed hiring for the same reason

Only 2% said they made large layoffs tied to actual AI implementation

So why is AI dominating layoff headlines?

Plain English: Most “AI layoffs” aren’t about AI replacing people.

They’re about expectations — and budgets.

1 The Uncomfortable Math

An MIT study later found something brutal:

Of companies investing heavily in AI… 95% saw zero measurable profit impact.

Billions spent. Almost nothing to show for it — yet.

So if AI isn’t actually replacing workers at scale…

why are companies firing people and blaming it?

Because “AI transformation” is a beautiful story for Wall Street.

Much cleaner than: “We overhired in 2021 and need to shrink now.”

2 The Companies Getting Caught

A few examples show how messy this really is.

Salesforce $CRM ( ▲ 0.73% ) cut 4,000 customer support jobs, saying AI could do “50% of the work.”

Later, a spokesperson admitted hundreds were simply redeployed elsewhere — not replaced by AI.

Klarna $KLAR ( ▲ 0.84% ) became the poster child for AI job replacement after cutting 40% of staff.

Then the CEO clarified:

“We have made 0 layoffs due to AI.”

Most cuts were due to slowing hiring after 2023.

Hold that thought…

IBM and Klarna later reversed some AI customer-service bets after discovering the tech couldn’t handle real-world complexity.

SPONSOR BREAK presented by BanyanHill*

President Trump Just Privatized The U.S. Dollar

A controversial new law (S.1582) just gave a small group of private companies legal authority to create a new form of government-authorized money.

Today, I can reveal how to use this new money… why it’s set to make early investors’ fortunes, and what to do before the wealth transfer begins on February 17 if you want to profit.

Go here for details now — while you still have time to position yourself.

3 What the Data Actually Shows

Yale’s Budget Lab analyzed U.S. labor data from 2022–2025.

Their conclusion:

AI has not caused widespread job destruction so far.

The disruption is far smaller than earlier tech waves like computers or the internet.

Instead, what we’re seeing looks more like:

→ Pandemic overhiring

→ Higher interest rates

→ Corporate belt-tightening

And … AI as the convenient excuse.

Who Actually Gets Hit Hardest

Entry-level workers are the ones catching it.

Between 2022 and 2025, opportunities for 22–25-year-olds in “AI-exposed” fields fell about 13% relative to trend.

Not because companies staged mass layoffs or because AI replaced entire roles overnight.

Because firms simply stopped backfilling junior jobs… fewer openings… period.

That’s what economists call soft attrition.

What workers feel is simpler: doors slowly closing.

And the consequences compound:

Fewer first jobs to break in

More work piling onto the remaining staff

Less training and mentorship for young talent

Bottom line:

The entry ladder got a lot steeper.

So…

… what’s really happening

Here’s the clean version.

AI isn’t marching through offices firing people by itself.

Layoffs aren’t a robot revolt.

They’re a budget reset wrapped in a tech story.

Companies overhired in the boom years.

Rates went up. Growth slowed.

The bills came due.

And “AI transformation” turned out to be the perfect cover.

✓ It sounds futuristic.

✓ It sounds strategic.

✓ It sounds inevitable.

It also sounds a lot better than:

“We staffed like it was 2021 and now we need to unwind it.”

That doesn’t mean AI is fake.

It means its impact is still ahead of its footprint.

Right now, AI is mostly a spending story, not a productivity story.

A narrative story, not a labor-market story.

A CapEx story, not a cash-flow story.

The irony?

The people who feel this the most aren’t executives or shareholders.

They’re the youngest workers — the ones who never got their first shot.

And that’s the AI-layoff loophole.

A budgeting problem — wearing an AI hoodie.

Lesson of the Day

💬 We Want To Hear Your Story:

Got a market or stock you want us to analyze next?

Just drop your request in the comments here.

Was this email forwarded to you? Don’t miss out on future stories — subscribe to the TradingLessons and get our daily market breakdown delivered straight to your inbox.

❗ P.S. – If you no longer want to receive occasional emails from us and you want to unsubscribe, click here 👉 “Unsubscribe” . Thank you!

AI-Layoff Excuse

Don’t forget to cast your vote 👇

So… about yesterday’s market.

After a week that felt held together with tape, Friday snapped back hard.

The Dow ripped past 50,000 for the first time ever.

The S&P 500 jumped nearly 2%. The Nasdaq followed.

Big Tech led the bounce — Nvidia +8%, Broadcom up big, Tesla higher — even as Amazon sank on plans to spend even more on AI.

Crypto bounced too: Bitcoin climbed back above $70K after plumbing 16-month lows. Strategy (MSTR) whipsawed, then finished sharply higher.

On paper, it looked like “risk is back.”

Underneath, it felt more like relief than conviction.

While markets were whipsawing, layoffs were hitting the worst January since 2009 — and many of them were explicitly tied to “AI.”

And here’s the disconnect.

Markets are trying to price an AI boom…

while companies are cutting people in the name of AI.

Which brings us to today’s story.

The Narrative:

In 2023–2024, that story was:

AI was inevitable. Spending was virtuous. Markets rewarded ambition.

Boards signed off. CFOs loosened the purse strings. Investors applauded louder with every new data center and every bigger CapEx number.

It was clean, simple, and comforting.

Then 2025-2026 arrived — and the narrative shifted.

Now the headline version is different:

AI is “eliminating jobs.”

You see it everywhere. It has become the neat, modern explanation for why tens of thousands of people are losing work.

But here’s the tension that doesn’t make the headlines:

If AI is truly replacing workers at scale…

you should see it clearly in productivity and profits.

Right now, you don’t.

So something doesn’t quite line up.

The Headline vs. The Reality

If you just read the headlines, the story sounds simple:

AI is here.

Jobs are disappearing.

Last month, Challenger, Gray & Christmas put a number on it:

Nearly 55,000 U.S. job cuts in 2025 were officially attributed to AI —

a 13× jump from when they first started tracking that category.

Corporate America leaned into that language:

Pinterest trimmed ~15% of staff, citing an “AI-forward approach.”

Dow Chemical announced 4,500 cuts while leaning into “AI and automation.”

Amazon cut 16,000 jobs, extending last year’s reductions.

Microsoft, Meta, and Salesforce all linked layoffs to “AI-driven efficiency.”

If you stopped there, you’d think the robots are already running the show.

But that’s where the story gets slippery.

SPONSOR BREAK presented by Porter&Co*

The #1 Way To Play Gold Right Now

We’re witnessing the greatest gold rush in over 50 years…

But one gold asset has outperformed miners, typical stocks, and gold itself for the last two decades.

Click to discover this little-known gold investment now

The Excuse

Oxford Economics looked at the same data… and came back with a very different read.

Their January report basically said:

AI probably isn’t killing jobs the way headlines suggest.

Why? Because if AI were actually replacing workers at scale, you’d expect a clear jump in productivity.

You don’t see that.

Their implication is blunt: Saying “AI did this” sounds better to investors than admitting weak demand or pandemic-era overhiring.

Yale’s Budget Lab backed that up.

Their analysis found that employment patterns still look mostly like they did before the AI boom — not like a labor market being radically reshaped by machines.

A December Harvard Business Review survey of 1,000+ executives showed exactly that:

60% have already reduced headcount in anticipation of AI

29% slowed hiring for the same reason

Only 2% said they made large layoffs tied to actual AI implementation

So why is AI dominating layoff headlines?

Plain English: Most “AI layoffs” aren’t about AI replacing people.

They’re about expectations — and budgets.

1 The Uncomfortable Math

An MIT study later found something brutal:

Of companies investing heavily in AI… 95% saw zero measurable profit impact.

Billions spent. Almost nothing to show for it — yet.

So if AI isn’t actually replacing workers at scale…

why are companies firing people and blaming it?

Because “AI transformation” is a beautiful story for Wall Street.

Much cleaner than: “We overhired in 2021 and need to shrink now.”

2 The Companies Getting Caught

A few examples show how messy this really is.

Salesforce $CRM ( ▲ 0.73% ) cut 4,000 customer support jobs, saying AI could do “50% of the work.”

Later, a spokesperson admitted hundreds were simply redeployed elsewhere — not replaced by AI.

Klarna $KLAR ( ▲ 0.84% ) became the poster child for AI job replacement after cutting 40% of staff.

Then the CEO clarified:

“We have made 0 layoffs due to AI.”

Most cuts were due to slowing hiring after 2023.

Hold that thought…

IBM and Klarna later reversed some AI customer-service bets after discovering the tech couldn’t handle real-world complexity.

SPONSOR BREAK presented by BanyanHill*

President Trump Just Privatized The U.S. Dollar

A controversial new law (S.1582) just gave a small group of private companies legal authority to create a new form of government-authorized money.

Today, I can reveal how to use this new money… why it’s set to make early investors’ fortunes, and what to do before the wealth transfer begins on February 17 if you want to profit.

Go here for details now — while you still have time to position yourself.

3 What the Data Actually Shows

Yale’s Budget Lab analyzed U.S. labor data from 2022–2025.

Their conclusion:

AI has not caused widespread job destruction so far.

The disruption is far smaller than earlier tech waves like computers or the internet.

Instead, what we’re seeing looks more like:

→ Pandemic overhiring

→ Higher interest rates

→ Corporate belt-tightening

And … AI as the convenient excuse.

Who Actually Gets Hit Hardest

Entry-level workers are the ones catching it.

Between 2022 and 2025, opportunities for 22–25-year-olds in “AI-exposed” fields fell about 13% relative to trend.

Not because companies staged mass layoffs or because AI replaced entire roles overnight.

Because firms simply stopped backfilling junior jobs… fewer openings… period.

That’s what economists call soft attrition.

What workers feel is simpler: doors slowly closing.

And the consequences compound:

Fewer first jobs to break in

More work piling onto the remaining staff

Less training and mentorship for young talent

Bottom line:

The entry ladder got a lot steeper.

So…

… what’s really happening

Here’s the clean version.

AI isn’t marching through offices firing people by itself.

Layoffs aren’t a robot revolt.

They’re a budget reset wrapped in a tech story.

Companies overhired in the boom years.

Rates went up. Growth slowed.

The bills came due.

And “AI transformation” turned out to be the perfect cover.

✓ It sounds futuristic.

✓ It sounds strategic.

✓ It sounds inevitable.

It also sounds a lot better than:

“We staffed like it was 2021 and now we need to unwind it.”

That doesn’t mean AI is fake.

It means its impact is still ahead of its footprint.

Right now, AI is mostly a spending story, not a productivity story.

A narrative story, not a labor-market story.

A CapEx story, not a cash-flow story.

The irony?

The people who feel this the most aren’t executives or shareholders.

They’re the youngest workers — the ones who never got their first shot.

And that’s the AI-layoff loophole.

A budgeting problem — wearing an AI hoodie.

Lesson of the Day

💬 We Want To Hear Your Story:

Got a market or stock you want us to analyze next?

Just drop your request in the comments here.

Was this email forwarded to you? Don’t miss out on future stories — subscribe to the TradingLessons and get our daily market breakdown delivered straight to your inbox.

❗ P.S. – If you no longer want to receive occasional emails from us and you want to unsubscribe, click here 👉 “Unsubscribe” . Thank you!

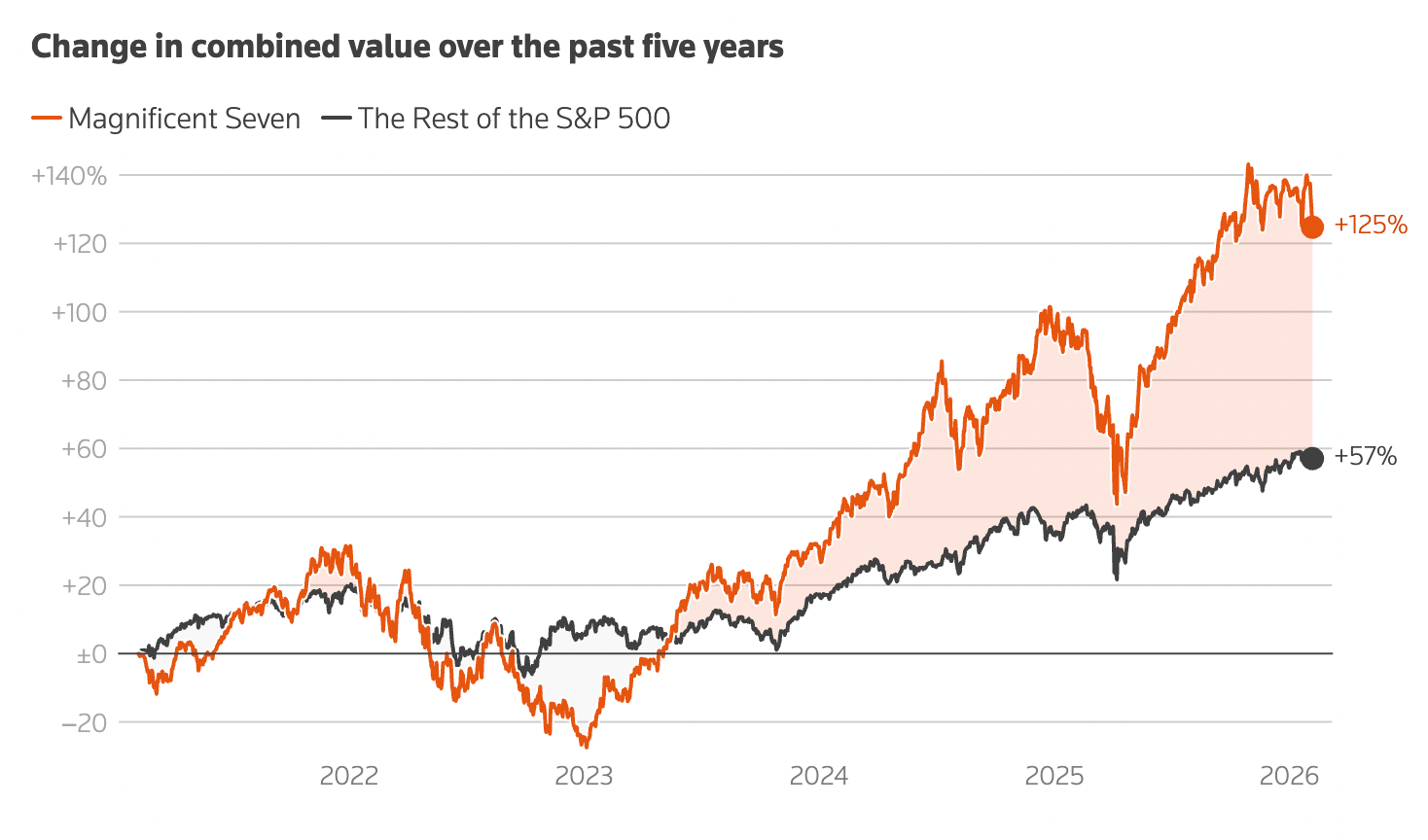

Un-Magnificent Moment

Don’t forget to cast your vote 👇

Did you read yesterday’s edition?

Bitcoin ( ▼ 13.05% ) was wobbling.

Today… it slipped after Treasury Secretary Scott Bessent made it clear the government isn’t riding to the rescue — and crypto took the hint.

While everyone was staring at crypto, something slower — and arguably more important — was happening in the biggest stocks on Earth.

So let’s put Bitcoin on pause for 60 seconds.

Because today’s story isn’t about tokens.

It’s about the “Magnificent Seven.”

For years, “own the Mag 7” was the easiest trade in markets. It worked so well it stopped feeling like a trade at all.

Now it feels… different.

And that’s usually how bigger shifts begin.

What Changed?

Markets have a funny habit. They reward the obvious trade… right up until it becomes too obvious.

For years, “own the Magnificent Seven” was the default setting.

And why not?

Their combined market cap hit $21.5 trillion — bigger than the GDP of every country on Earth except the U.S.

But lately, the “Magnificent” part has started to feel… optional.

Last year, five of the seven — Amazon, Apple, Meta, Microsoft, and Tesla — trailed the S&P 500.

source: Reuters

And that underperformance has carried into 2026, even though their index weight is still doing the heavy lifting.

So what changed?

The Issue

For years, the Mag 7 had the perfect combo:

cash flow rising + growth narrative intact.

Now that combo is breaking.

Gina Martin Adams (HB Wealth) points to the key shift:

Cash flow peaked in 2024

Then it started slipping in 2025

At the same time, spending sped up. These companies are writing bigger checks at the exact moment the cash coming in is no longer accelerating.

And the biggest checks have one label on them:

AI.

Last year, the Magnificent Seven spent an estimated $320B chasing it — buying chips, building data centers, upgrading infrastructure, and picking up AI startups.

So the setup investors are staring at is simple:

High spending today

Payoff later

And cash flow isn’t getting stronger in the meantime

That’s why the stocks feel heavier.

Because the market is asking a more annoying question:

When does this start showing up in results?

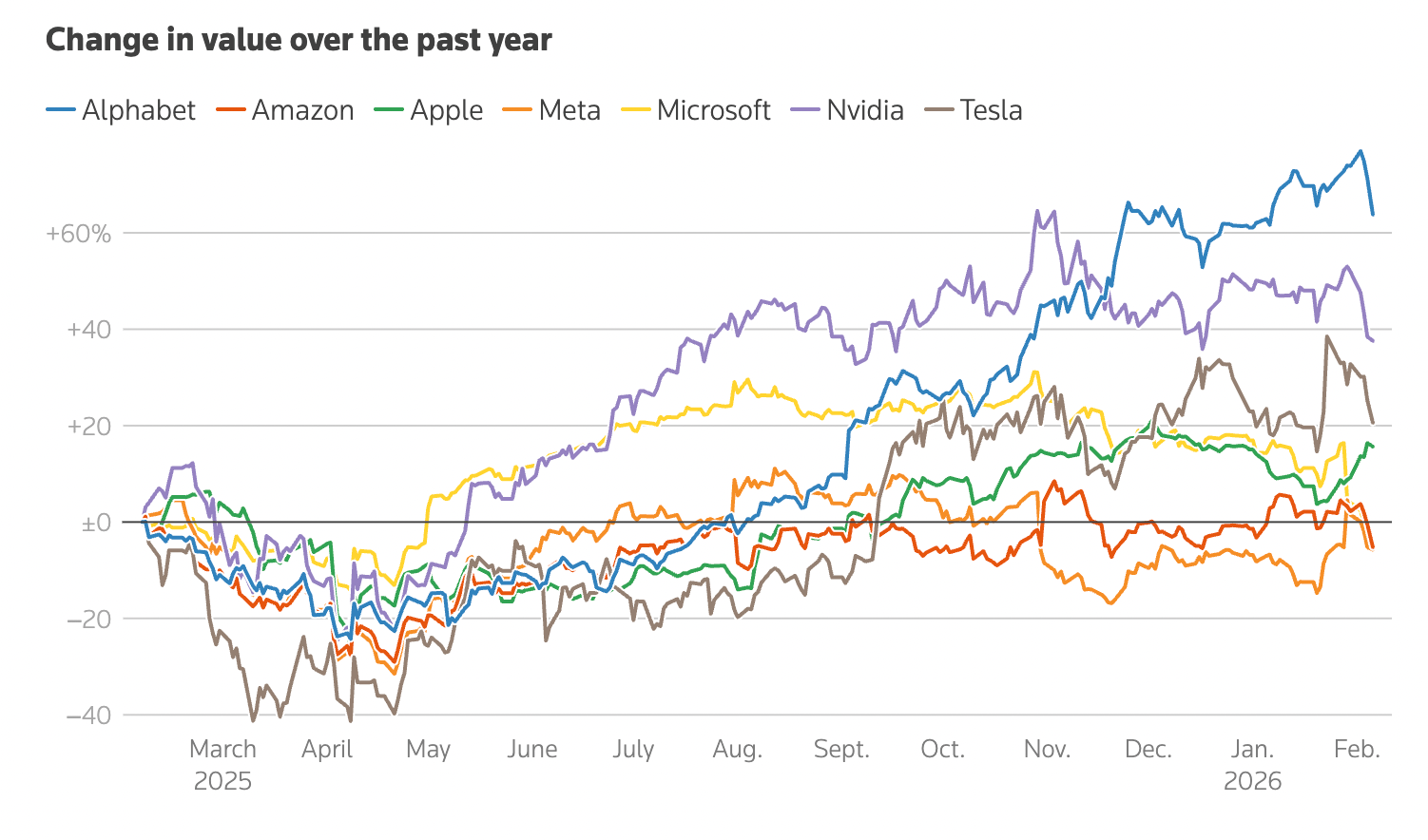

1 Amazon is a clean example of the new math

Amazon tells the story better than any chart.

In 2025, the stock gained 4% — the weakest in the Mag 7, and about 13% behind the S&P 500.

Not a disaster. Not a win either.

What matters is what was happening offstage.

Through the first three quarters of 2025, Amazon’s CapEx hit $89.9B, as CFO Brian Olsavsky put it, to “support demand for AI and core services.”

Then came Q4.

Amazon ( ▼ 4.42% ) just reported earnings — and the stock slid.

→ EPS came in at $1.95 vs. $1.97 expected.

→ Sales beat at $213.4B vs. $211.4B expected.

But guidance is what spooked the market.

❗ For Q1, Amazon sees:

Sales of $173.5B–$178.5B (Street was at $175.6B)

Operating income of $16.5B–$21.5B — below consensus at $22.18B

In short: Big spend today. Unclear payoff tomorrow.

That’s the new math investors are working through — not just for Amazon, but for the whole group.

SPONSOR BREAK presented by TheOxfordClub*

How Mitt Romney Turned $450K Into Up to $100 Million (Tax-Free)

It wasn’t stocks. It wasn’t real estate. It was a little-known investment vehicle that turned Mitt Romney’s $450,000 into as much as $100 million and Peter Thiel used to turn $2,000 into $5 billion within two decades. Now, thanks to a new executive order, regular Americans can access the same type of investment.

Get more details here >>

2 The question isn’t AI hype — it’s AI adoption

Gina Martin Adams makes a simple distinction:

It’s not enough for companies to “try” AI.

It needs to become a must-have, deeply embedded into processes, driving margin expansion and productivity growth.

Right now, full adoption is slower, for boring reasons that still win:

ROI uncertainty

messy legacy systems

skilled labor shortages

decisions that touch engineering, legal, security, compliance, and finance

In other words: the tech moves fast. Organizations don’t.

So while the Mag 7 build, the other 493 stocks in the S&P 500 get a shot at being the better growth story.

And investors are noticing.

3 Why Experts Say That’s “Healthy”

Zoom out.

Tech is the worst S&P 500 sector this year (down ~5%).

Energy and consumer staples are up double digits.

That flip is the whole story.

Stephen Parker at JPMorgan calls it “very healthy” because the market is finally broadening — less “Mag 7 or bust,” more everything else.

Bank of America flow data supports it: In the past month, BofA clients funneled more into consumer staples than any four-week stretch since 2008. And they’ve been net sellers of tech four of the past five weeks.

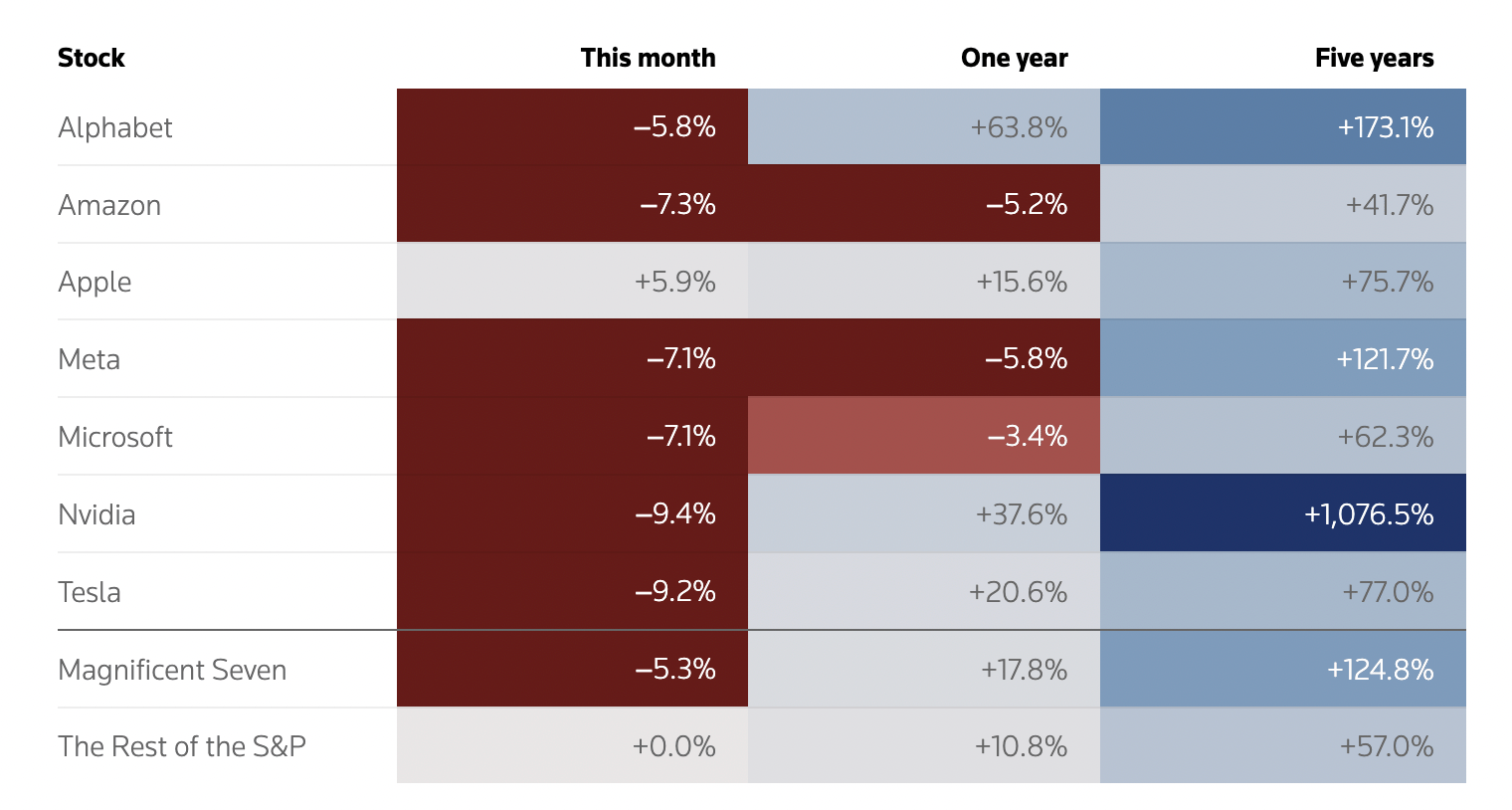

Earnings: mixed results, same theme

source: Reuters

Recent Mag 7 reports didn’t give the market one clear story — they gave it a split screen.

A Microsoft ( ▼ 4.95% ) sold off despite beating on EPS and revenue after tempered Azure guidance

Q2 FY2026 EPS: $4.14 vs $3.86 expected

Revenue: $81.27B vs $80.28B expected

Azure growth near 40%, but guiding 37%–38% next quarter

CapEx in Q2: $37.5B

Market reaction: “Beat” isn’t enough if the spending is still accelerating and growth is decelerating.

B Meta ( ▲ 0.18% ) popped after a blowout and strong guidance

EPS: $8.88; revenue $59.85B (both ahead)

2026 AI CapEx expected $115B–$135B (up from $72B in 2025)

Q1 revenue guidance: $53.5B–$56.5B

Same category of story (spend big on AI)… different market reaction because guidance soothed nerves.

source: Reuters

C Tesla ( ▼ 2.17% ) dropped after an annual revenue decline, then rebounded on a pivot toward robotics

First-ever annual revenue decline (down 3% YoY)

Operating costs up 39% in Q4

Deliveries: 1.636M, nearly 9% fewer than 2024

Forward P/E: 163.65

D Apple ( ▼ 0.21% ) posted record EPS and revenue

EPS: $2.84 vs $2.65 expected

Revenue: $143.76B vs $138.25B expected

Revenue up 16% YoY, EPS up 19% YoY

Greater China up 38% YoY

E Alphabet ( ▼ 0.54% ) posted strong Q4 results

EPS: $2.82 vs ~$2.64 expected

Revenue: $113.83B vs $111.4B expected

Net income: $34.5B (▲ 30% YoY)

Operating margin: 31.6%

Google Cloud revenue: $17.7B (▲ 48% YoY)

Search & other ad revenue: $82.28B

F Amazon ( ▼ 4.42% ) slid on Q4 results

EPS: $1.95 vs $1.97 expected

Revenue: $213.4B vs $211.43B expected

Q1 sales guidance: $173.5B–$178.5B vs $175.62B expected

Q1 operating income guidance: $16.5B–$21.5B vs $22.18B expected

Stock reaction: down ~6.7% after the report

SPONSOR BREAK presented by BehindtheMarkets*

A U.S. “birthright” claim worth trillions – activated quietly

A tiny government task force working out of a strip mall just finished a 20-year mission.

And with almost no media coverage, they confirmed one of the largest U.S. territorial expansions in modern history…

A resource claim worth an estimated $500 trillion.

Thanks to sovereign U.S. law, this isn’t just a national asset.

It’s an American birthright.

That means every citizen now has the legal right to stake a claim…

But very few even know the opportunity exists.

If you want to see how you can get in line for your portion of this record-breaking windfall…

I’ve assembled everything you need to see inside a new, time-sensitive briefing:

Get all the details here – while the claim window remains open.

Meanwhile, software is getting hunted

This part is important because it explains why “tech weakness” doesn’t feel evenly distributed.

Short sellers have posted about $24B in paper gains in the software selloff (S3 Partners data).

Software + AI-related stocks are down roughly 20% since the start of the year.

Leon Gross (S3) called it out:

This is software-specific — the broader Mag 7 is essentially unchanged.

The trigger point in this latest leg:

Anthropic introduced a new productivity tool Monday… and the selloff intensified.

Short interest is rising in names including:

Microsoft

Oracle

Broadcom

Amazon

And the positioning is shifting:

Gross said Microsoft usually behaves like a “reversal stock” with shorts covering on the way down.

But now it’s trading like a momentum-driven distressed name — with shorts increasing into weakness.

The scoreboard

The iShares Expanded Tech-Software ETF (IGV) tells the story cleanly:

Down 8% this week

Down >21% this year

Down 30% from its September all-time high

Individual damage:

Intuit and DocuSign down >30%

Microsoft down 15%

Oracle down 21%

Salesforce, Adobe, ServiceNow down >20%

One small stabilizer:

A banker noted there isn’t too much panic on the credit side yet — revolving credit lines aren’t being drawn.

And the next catalyst is close:

Several software companies report earnings in the coming days.

So…

…the Mag 7 didn’t suddenly become “bad companies.”

But the market is treating them differently:

Cash flow peaked (per HB Wealth)

CapEx is still accelerating

AI adoption is taking longer than the hype cycle

Rotation is showing up in sector returns and real fund flows

Software is facing a separate, more aggressive de-rating with shorts pressing

This doesn’t mean tech is “over.”

It means 2026 is starting to price something the last two years didn’t:

AI spend without immediate payoff.

Lesson of the Day

💬 We Want To Hear Your Story:

Got a market or stock you want us to analyze next?

Just drop your request in the comments here.

Was this email forwarded to you? Don’t miss out on future stories — subscribe to the TradingLessons and get our daily market breakdown delivered straight to your inbox.

❗ P.S. – If you no longer want to receive occasional emails from us and you want to unsubscribe, click here 👉 “Unsubscribe” . Thank you!

Bitcoin’s Quiet Problem

Don’t forget to cast your vote 👇

This one wasn’t on the bingo card.

A few months ago, the Bitcoin bear case sounded reasonable:

Maybe we get a normal pullback. Maybe some chop. Nothing dramatic.

Well… here we are.

Bitcoin isn’t crashing in one violent move.

It’s doing something more unsettling: slowly losing its footing.

That’s usually how trouble starts — with a quiet slide that makes everyone uncomfortable.

The Spark That Started The Chain

Back in November, Michael Purves flagged something most people brushed off: a monthly MACD sell signal.

MACD is basically a speedometer for the market. It tells you how fast (or slow) it’s moving.

When that speedometer flips to “sell,” it means momentum has rolled over. The car is losing steam.

This only happens on Bitcoin’s monthly chart about once in a blue moon — November was just the sixth time ever.

And historically, when that big-picture momentum turns negative, Bitcoin hasn’t had a gentle response. In prior episodes, it eventually fell around 60%.

Back then, that warning sounded like a tail risk.

Today, it sounds less like a warning.

1 The second domino

If the MACD was the spark, the next issue quietly finished forming.

Bitcoin just completed a bearish head-and-shoulders pattern.

If you’ve never seen one, here’s the fast version:

Around $110K → left shoulder

The all-time high → the head

A bounce near $98K → right shoulder

And a neckline drawn across ~$76,000

On most charts, that $76K line would be just another number.

Here, it isn’t.

That level also happens to be Strategy’s $MSTR ( ▼ 3.13% ) average cost basis.

So if Bitcoin loses that level decisively, the conversation changes.

This stops being a debate about patterns — and becomes a debate about leverage.

Not because anyone wants to sell but because leverage eventually makes the call for you.

To their credit, Strategy wasn’t blind to this.

In December, they set aside a $1.44 billion cash reserve to cover interest and dividends — a cushion designed to prevent exactly this kind of forced selling.

Still: when a key technical level lines up perfectly with a massive corporate cost basis, traders treat it like a fault line.

2 Why October still haunts this market

A lot of what we’re seeing today traces back to the October 10 liquidation event.

Back then, illiquid markets on Binance helped trigger tens of billions of dollars in liquidations in a single day.

The scars are still visible.

Crypto market cap: $4.2T → $2.6T

$758M in liquidations in the last 24 hours

Nearly $7B liquidated over the past week

Spot Bitcoin ETFs logged $272M in outflows in one day

That is called a liquidity crunch.

When liquidity dries up, prices don’t fall cleanly – they slide, gap, and overshoot.

Bitcoin is hovering just above $75,000, down more than 40% from its October 6 all-time high — its lowest level since the session after Trump’s 2024 election win.

Alexander Blume, CEO of Two Prime, told Sherwood News that given the spike in volatility and current price levels, “we are likely not far from the bottom.”

Maybe. But “close to the bottom” is not the same as “safe to buy.”

3 The macro wrinkle

This selloff isn’t happening in a vacuum.

Gold and silver just went through their own violent reset — and that spilled over into Bitcoin.

The strange part?

Bitcoin didn’t really participate in the upside of the metals rally…

but it is absolutely participating in the downside.

Add to that:

Citi analysts note that a potential Kevin Warsh Fed nomination (a smaller-balance-sheet guy) could be adding to the angst.

They also highlight $70K as the key “pre-election level” to watch.

SPONSOR BREAK presented by TheOxfordClub*

How Mitt Romney Turned $450K Into Up to $100 Million (Tax-Free)

It wasn’t stocks. It wasn’t real estate. It was a little-known investment vehicle that turned Mitt Romney’s $450,000 into as much as $100 million and Peter Thiel used to turn $2,000 into $5 billion within two decades. Now, thanks to a new executive order, regular Americans can access the same type of investment.

Get more details here >>

The Key Price Zones

Here’s how traders are mapping this:

A $70,000 — pure psychology

Just above the prior cycle’s $69K high.

Break this, and the tone of the market shifts instantly.

B $55,700–$58,200 — the structural zone

Between realized price and the 200-week moving average.

That’s the line between “pullback” and “cycle reset.”

Above that, some traders are watching whether Bitcoin can:

defend the mid-$70,000s, and

reclaim the $78,000–$80,000 zone to repair the chart.

SPONSOR SECTION presented by TheOxfordClub*

There is no question, AI is a game-changer.

$4.8 trillion is expected in new money is expected to be added to the global economy within the decade…

And thousands of Americans are claiming their share of this generational wealth-building opportunity by spending ONE hour per week using the power of AI to target what some are calling “Weekly AI Cash Waves”.

One Georgia millionaire recorded a short video showing how he’s been cashing in using the power of AI.

In it you’ll learn how:

This technique is based on research done by Harvard, the Federal Reserve and many other prestigious institutions

Has provided multiple money-doubling returns within as little as a few hours.

Why you don’t need to be a pro to take advantage of the power of AI

Click here to watch this free video and learn how to target these Weekly AI Cash Waves.

Yours in smart speculation,

Ryan Fitzwater, Publisher

Monument Traders Alliance

Disclaimer: This ad is sent on behalf of Monument Traders Alliance. 105 W. Monument Street Baltimore, MD 21201. If you would like to optout from receiving offers from Monument Traders Alliance, please click here.

Enter Michael Burry — and the domino theory

source: BusinessInsider

This is where your story gets interesting. Burry isn’t just saying “Bitcoin is going down.”

He’s describing a self-reinforcing chain reaction.

His argument, step by step:

1. Bitcoin falls ~40% from its peak.

2. Corporate treasuries holding BTC feel pressure — because treasury assets must be marked to market.

3. Risk managers start advising companies to sell.

4. Miners get squeezed as prices drop.

5. “Tokenized metal futures” (which aren’t backed by physical metal) get forced to liquidate.

6. That selling bleeds into real gold and silver markets.

7. Which feeds back into broader risk markets.

He calls this a potential “collateral death spiral.”

Burry even estimates that up to $1 billion in precious metals may have been liquidated at the end of the month because of falling crypto prices.

If Bitcoin were to fall to $50,000, he argues:

Many miners would go bankrupt, and

Tokenized metal futures could “collapse into a black hole with no buyer.”

He’s blunt about Bitcoin’s role right now:

It hasn’t acted like a debasement hedge like gold.

ETFs may have made it more speculative, not less.

Its correlation with the S&P 500 is now near 0.50.

Nearly 200 public companies hold Bitcoin — which sounds bullish, until you realize that “there is nothing permanent about treasury assets.”

That’s Burry’s core point:

Belief doesn’t move corporate balance sheets. Accounting does.

So…

… is this systemic?

Here’s the counterweight — and it’s important you included this.

Even Burry acknowledges that crypto is probably too small to crash everything.

Bitcoin’s market cap is about $1.5 trillion

Household exposure is still limited

Past collapses (Terra, FTX) didn’t infect traditional markets

Strategy also says:

There are no margin calls right now

No expectation of forced Bitcoin sales

A cash cushion that began in December and has since grown to about $2.25B now covers interest and distributions for more than two years.

So this isn’t 2008 — it’s more like a contained but messy unwind.

Lesson of the Day

💬 We Want To Hear Your Story:

Got a market or stock you want us to analyze next?

Just drop your request in the comments here.

Was this email forwarded to you? Don’t miss out on future stories — subscribe to the TradingLessons and get our daily market breakdown delivered straight to your inbox.

❗ P.S. – If you no longer want to receive occasional emails from us and you want to unsubscribe, click here 👉 “Unsubscribe” . Thank you!

Beyond the Bullion

Don’t forget to cast your vote 👇

Gold and silver have been everywhere last week.

At this point, even my dog probably has a view on gold.

So before we all start seeing bullion in our dreams, let’s give the metals a quick timeout today.

We’re turning our head to two other stories that are just as interesting.

Enjoy reading.

SpaceX Just Ate xAI

This didn’t just get closer to a deal. It got closer to a public company.

Bloomberg first said SpaceX and xAI were in “advanced talks.”

Now there’s an internal memo saying they’ve merged — with a target valuation around $1.25–$1.5 trillion.

On the surface, this looks like Elon Musk combining two of his companies.

Underneath, it looks like him designing a story the public markets can actually price.

1 Here’s why.

SpaceX alone is an extraordinary business — rockets, satellites, Starlink, manufacturing, launch contracts — but it’s still a capital-intensive, long-cycle company. Great technology. Harder multiples.

xAI, on the other hand, is pure future optionality.

High-margin. High-growth. Very “marketable” to public investors.

Put them together, and you don’t just get a space company.

You get a space + AI platform.

Rockets + satellites + compute + data + distribution (X). That’s a stack.

From an IPO perspective, that matters.

Public markets tend to pay up for:

→ Platforms

→ Ecosystems

→ Vertical integration

→ AI exposure

→ Scarce assets with network effects

A standalone SpaceX IPO would have been massive.

A combined SpaceX/xAI IPO is designed to be legendary.

2 In fact, the timeline now looks real.

SpaceX is reportedly targeting a mid-June IPO, possibly around June 9 — when Jupiter and Venus align in the night sky. (Of course Musk would time a $1.5 trillion IPO to a cosmic event.)

The company is aiming to raise up to $50 billion, which would make this the largest IPO by capital raised in history. At a ~$1.5 trillion valuation, it would likely be the second-most valuable IPO ever, behind only Saudi Aramco.

OpenAI might try to rival it this year — but SpaceX would still be the heavyweight.

And retail investors are already positioning.

A private fund that holds SpaceX shares has seen inflows surge more than 200% since IPO rumors began. People are already trying to get in before this thing ever hits the public tape.

For Musk personally, the stakes are staggering.

He owns roughly 42% of SpaceX — which could be worth $600+ billion at the target valuation. That’s more than triple the value of his current Tesla stake.

3 There’s another signal buried in the reporting though: Tesla fading to the background.

Earlier leaks floated Tesla as part of the tie-up.

Now, in the latest stories that move the deal forward, Tesla is barely mentioned.

Translation:

Musk isn’t trying to blur SpaceX with Tesla — he’s trying to separate their destinies.

1) SpaceX becomes the space + AI powerhouse.

2)Tesla stays the robotics, autonomy, and energy company.

Two different public-market stories. Cleaner. Easier to value.

Then there’s the “data centers in space” angle.

Most people read that as sci-fi. Markets will read it as capex with a moonshot narrative.

If SpaceX can even partially pull this off, it turns satellites into:

→ Power infrastructure

→ Compute infrastructure

→ AI infrastructure

So when you hear “$1.25 trillion IPO,” don’t think big number.

Think:

Musk is packaging scarcity (rockets), distribution (Starlink), and AI into one ticket — and selling it to public investors as the next-generation infrastructure company.

In other words:

This merger isn’t just about control.

It’s about valuation.

SPONSOR BREAK presented by BehindtheMarkets*

A U.S. “birthright” claim worth trillions – activated quietly

A tiny government task force working out of a strip mall just finished a 20-year mission.

And with almost no media coverage, they confirmed one of the largest U.S. territorial expansions in modern history…

A resource claim worth an estimated $500 trillion.

Thanks to sovereign U.S. law, this isn’t just a national asset.

It’s an American birthright.

That means every citizen now has the legal right to stake a claim…

But very few even know the opportunity exists.

If you want to see how you can get in line for your portion of this record-breaking windfall…

I’ve assembled everything you need to see inside a new, time-sensitive briefing:

Get all the details here – while the claim window remains open.

Washington’s $12B Safety Net

Rare earths are boring… You don’t hear much about them and mostly only notice them when something breaks — or when Washington starts spending $12 billion.

That’s what Project Vault is.

A new U.S. critical-minerals stockpile — basically the Strategic Petroleum Reserve, but for metals most of us can’t pronounce, like gallium, cobalt, and lanthanum that sit inside EVs, chips, satellites, and defense systems.

Roughly $12 billion in capital — $10 billion from the U.S. Export-Import Bank plus about $1.7 billion from private investors — aimed at creating a civilian critical-minerals reserve.

Here’s how it’s supposed to work (quickly):

• Manufacturers commit to buy certain materials at a set price in the future.

• They pay some fees up front.

• Trading houses (Hartree, Traxys, Mercuria) source and store the metals.

• Companies can draw down their stash in a crisis — as long as they refill it later.

Plain English:

Washington would be helping industry pre-fund a shared inventory, so companies aren’t exposed if global supply suddenly seizes up.

Why is this happening?

Because China still dominates the processing of many critical minerals — and last year’s export controls made that dependence feel very real, very fast.

The market reacted immediately.

Rare-earth and critical-metals stocks jumped in premarket trading — names like MP Materials, USA Rare Earth, Critical Metals, NioCorp, and U.S. Antimony.

Here is how they ended:

→ MP Materials $MP ( ▲ 0.58% )

→ USA Rare Earth $USAR ( ▼ 1.38% )

→ Critical Metals CRML ( ▼ 4.4% )

→ NioCorp NB ( ▲ 4.41% )

→ United States Antimony UAMY ( ▲ 7.23% )

Long-term demand became more visible — and policy-backed.

One more detail: This would be a civilian stockpile. The U.S. already has reserves for defense needs. Project Vault is aimed at automakers, tech firms, and other manufacturers.

That’s new.

SPONSOR SECTION presented by BehindTheMarkets*

On September 14th, 2023, something big happened.

You didn’t see it on the news. They didn’t want you to.

The price gap between London gold and Shanghai gold blew out to $120 an ounce.

For years, that gap was a few dollars. Maybe $5. Sometimes $10.

$120 is a 20x jump. In seconds.

That’s not a ‘glitch.’ That’s the system breaking.

Traders saw it. They tried to buy gold in London to sell it in Shanghai. Easy money, right?

But they hit a wall.

Why? The London vaults were empty.

The screen said ‘Gold for Sale.’ But when they went to get it… there was nothing there.

Since that day, gold has hit 53 all-time highs. It keeps running.

I’ve found one stock set to capture the bulk of this wealth transfer. I call it the ‘Shadow Miner.’

Get the name and ticker here >>>

“The Buck Stops Here”

Behind the Markets

So…

Here’s where we start the week.

We’ll keep an eye on who’s quietly getting ready — and why it matters for you.

More on Wednesday.

Lesson of the Day

💬 We Want To Hear Your Story:

Got a market or stock you want us to analyze next?

Just drop your request in the comments here.

Was this email forwarded to you? Don’t miss out on future stories — subscribe to the TradingLessons and get our daily market breakdown delivered straight to your inbox.

❗ P.S. – If you no longer want to receive occasional emails from us and you want to unsubscribe, click here 👉 “Unsubscribe” . Thank you!

Metals Took a Hit. Is the Story Over?

Don’t forget to cast your vote 👇

Don’t worry — we noticed too.

We spent most of the week talking about gold.

About silver.

About why everyone suddenly cared again.

Which makes Friday’s move… inconvenient.

Gold and silver didn’t just pull back.

They reset.

Gold briefly fell more than 10% intraday, its sharpest one-day drop since the 1980s — worse than its worst day during the 2008 financial crisis.

Silver was hit harder, sliding nearly 30% at one point — its biggest percentage drop since 1980.

For assets known as safe havens, that’s uncomfortable.

But it’s also revealing.

Gold’s Trade Just Got Crowded

This wasn’t a slow, thoughtful reassessment.

It was a crowded trade hitting the exit at the same time.

Over the past few weeks, gold and silver weren’t just being bought by long-term allocators or central banks. They were being chased.

Retail enthusiasm exploded.

Leverage crept in.

Leveraged ETFs became popular ways to “juice” exposure.

And that’s where things broke.

Take silver.

The ProShares Ultra Silver ETF (2× daily exposure) had become one of the most crowded ways to play the move. When silver futures settled Friday afternoon, that ETF had to rebalance.

Which meant selling.

A lot of selling.

All at once.

That mechanical unwind amplified what was already a fragile setup.

This wasn’t a change in the long-term story.

It was positioning snapping back.

The Part Most People Miss

“Safe haven” doesn’t mean prices don’t move.

It means something else.

Gold and silver are usually bought for how they feel to own — not because they promise stability, but because they offer reassurance when everything else feels uncertain.

For a while, that reassurance quietly turned into confidence.

➝ Prices kept rising.

➝ The trade felt increasingly obvious.

➝ Risk started to feel… optional.

That’s usually the moment the market starts changing the rules.

Not because the story breaks — but because positioning does.

Silver is almost always the first to react.

It’s thinner than gold, more volatile, and far more sensitive to flows. When trades get crowded, silver doesn’t absorb pressure the way gold can.

It reflects it.

So gold pulled back. Silver lurched.

Whether you call it volatility or whiplash, the message was the same.

SPONSOR BREAK presented by BehindtheMarkets*

A U.S. “birthright” claim worth trillions – activated quietly

A tiny government task force working out of a strip mall just finished a 20-year mission.

And with almost no media coverage, they confirmed one of the largest U.S. territorial expansions in modern history…

A resource claim worth an estimated $500 trillion.

Thanks to sovereign U.S. law, this isn’t just a national asset.

It’s an American birthright.

That means every citizen now has the legal right to stake a claim…

But very few even know the opportunity exists.

If you want to see how you can get in line for your portion of this record-breaking windfall…

I’ve assembled everything you need to see inside a new, time-sensitive briefing:

Get all the details here – while the claim window remains open.

Where Things Snapped

Silver shows it most clearly.

As precious metals ripped higher, leveraged ETFs tied to gold and silver futures quietly became some of the most popular ways to play the move. They offered speed, leverage, and simplicity — especially as prices went parabolic.

That popularity mattered.

One of the largest silver products offers 2× the daily move, using futures contracts rather than physical metal. And like all leveraged ETFs, it has to rebalance every day to stay on target.

On Friday afternoon — right around 1:25 p.m. ET — silver futures hit their daily settlement.

That’s when the rebalance happened.

In this case, rebalancing meant selling futures into an already falling market.

So this move picked up speed.

Gold dipped.

Silver whiplashed.

Why Silver Feels So Unstable

Here’s the part that often gets misunderstood:

Most silver moves aren’t really about silver.

They’re about everything around it.

When investors get uneasy — about growth, inflation, trade policy, or politics — they tend to reach for familiar hedges. Gold. Silver. Things that don’t rely on earnings calls or balance sheets.

That’s when silver shows its personality.

Unlike gold, silver lives in two worlds at once.

It’s a financial hedge and an industrial input. The same metal that gets bought during moments of fear also ends up inside solar panels, smartphones, semiconductors, and data centers.

That overlap is powerful, and also destabilizing.

When macro anxiety rises, investment demand shows up quickly. When industrial demand stays firm at the same time, supply doesn’t have much room to breathe. Prices can move fast — in both directions.

That’s why silver rarely drifts. It surges, and then it snaps back.

SPONSOR BREAK presented by BanyanHill*

President Trump Just Privatized The U.S. Dollar

A controversial new law (S.1582) just gave a small group of private companies legal authority to create a new form of government-authorized money.

Today, I can reveal how to use this new money… why it’s set to make early investors’ fortunes, and what to do before the wealth transfer begins on February 17 if you want to profit.

Go here for details now — while you still have time to position yourself.

What This Move Really Did

It didn’t end the conversation around gold and silver.

It changed who’s still in it.

➝ Short-term, leveraged positioning was flushed out.

➝ Longer-term capital now has room to reassess — without the same momentum pressure.

That’s how markets reset without breaking.

So…

Yes — we basically turned into a gold newsletter this week.

That wasn’t an accident.

Big moves attract attention.

Big reversals reveal structure.

And that’s what this week was really about.

Not gold versus silver.

Not predictions.

Not calling tops or bottoms.

It was about crowding, leverage, and how quickly confidence can shift once a trade stops feeling effortless.

The long-term questions:

What role do gold and silver actually play when uncertainty lasts longer than a headline?

… haven’t gone anywhere.

Lesson of the Day

💬 We Want To Hear Your Story:

Got a market or stock you want us to analyze next?

Just drop your request in the comments here.

Was this email forwarded to you? Don’t miss out on future stories — subscribe to the TradingLessons and get our daily market breakdown delivered straight to your inbox.

❗ P.S. – If you no longer want to receive occasional emails from us and you want to unsubscribe, click here 👉 “Unsubscribe” . Thank you!

Weaker Dollar: The Hidden Math

Don’t forget to cast your vote 👇

Most days, the dollar sits quietly behind everything you buy, sell, invest, or save. It prices your coffee, your portfolio, your vacation, your oil, your gold — and then politely stays out of the spotlight.

Stocks move.

Crypto swings.

Commodities spike.

The dollar usually just… exists.

Which is why it’s worth paying attention when the dollar suddenly becomes the headline.

This week, the greenback dropped about 1.3% ▼ in a single session — its sharpest daily slide in months — and briefly touched levels not seen since early 2022. Over the past year, it’s now down roughly 10%.

The spark wasn’t a data miss or a central bank surprise. It came from a simple comment.

When asked whether the currency had fallen too far, President Trump said he was comfortable with the move and described a weaker dollar as “great.”

Markets didn’t debate the nuance.

They reacted to the signal.

Weak Dollar Isn’t Always Bad News

Everyone likes a good deal.

You feel it when your favorite coffee suddenly costs a dollar less.

You feel it when flights drop overnight.

You feel it when something you’ve been putting off suddenly feels easier to afford.

Cheaper feels like winning.

But sometimes “cheaper” just means the bill shows up somewhere else.

That same logic quietly applies to currencies — even if most of us never think about it that way.

A weaker dollar isn’t automatically bad news.

In fact, the early effects often look constructive.

→ U.S. products suddenly feel cheaper to buyers overseas, so exports sell faster.

→ Companies that earn money abroad see those profits stretch a little further when they come home.

→ Tourism and travel get a quiet boost as price advantages shift.

Governments sometimes tolerate — or even quietly welcome — a softer currency because a softer dollar + modest inflation, slowly reduces the real burden of fixed debt. When trillions of dollars are owed, even small shifts in purchasing power matter.

And markets tend to enjoy this phase.

Until the trade-offs start surfacing.

→ Imports get more expensive.

→ Inflation pressure creeps in.

→ Investors begin paying closer attention to where their capital actually wants to sit.

The benefits arrive quickly. The consequences tend to move more slowly.

And that’s the uncomfortable part.

Which sets up the real question:

When the dollar weakens… do the pros actually outweigh the cons? 👇

You don’t have to guess.

You can watch where the money is going.

As the dollar slid, capital started repositioning almost immediately.

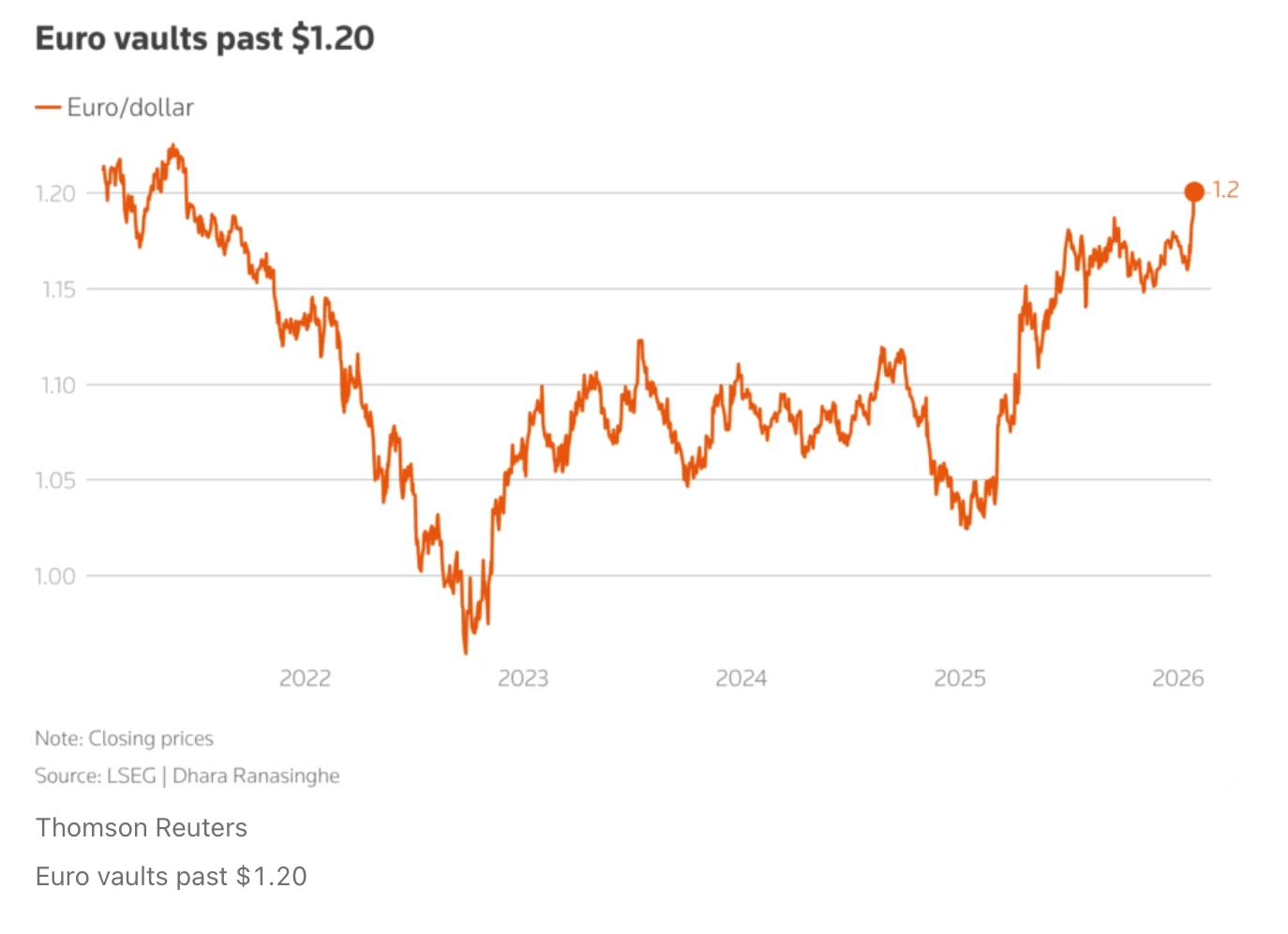

Gold ( ▲ 3.68% ) climbed to fresh record highs above $5,300, extending a rally that’s been quietly building in the background. The euro ▲ ( 1 EUR ≈ $1.20 USD ) pushed into territory it hasn’t seen in years. The Swiss franc ▲ ( 1 CHF ≈ $1.30 USD ) picked up demand as investors leaned toward familiar safe havens. Even the yen caught a bid as policy chatter crept back into the conversation.

Nothing dramatic on its own.

But together, it tells a simple story: money started exploring alternatives.

Some strategists have framed this less as a technical currency move and more as a confidence shift. When leadership signals comfort with a weakening currency, the psychological backstop under the dollar naturally feels thinner. That doesn’t trigger panic. It triggers optionality.

Capital likes options.

Crypto hasn’t joined the party yet in a meaningful way, especially compared with gold. But several macro investors have noted that if confidence erosion continues — and if traditional hedges become crowded — alternative reserve assets like bitcoin may eventually start catching more of that flow.

The point is that the race has already started.

Which brings us back to the trade-off.

SPONSOR BREAK presented by BanyanHill*

President Trump Just Privatized The U.S. Dollar

A controversial new law (S.1582) just gave a small group of private companies legal authority to create a new form of government-authorized money.

Today, I can reveal how to use this new money… why it’s set to make early investors’ fortunes, and what to do before the wealth transfer begins on February 17 if you want to profit.

Go here for details now — while you still have time to position yourself.

What Keeps the Dollar Trend Up?

Currency trends don’t reverse just because prices feel stretched.

They reverse when the reasons for owning them start to shift.

→ As long as growth differentials favor the U.S., capital tends to stay home.

→ As long as real yields remain attractive, global money tolerates volatility.

→ As long as policymakers signal stability, confidence holds.

As long as those advantages remain in place, capital tends to stay comfortable — even if prices wobble along the way.

That’s why Treasury Secretary Scott Bessent emphasized this week that the U.S. continues to operate under a strong-dollar framework grounded in sound fundamentals. In his view, healthy policies ultimately attract capital, regardless of short-term market noise.

Markets constantly recalibrate around growth expectations, yield differences, and global opportunity. That process is less about drama and more about quiet adjustment.

Most currency trends evolve the same way.

Gradually. Rationally. Boringly.

Until something genuinely changes.

What Would Naturally Shift the Momentum

For the dollar’s direction to meaningfully adjust, markets would typically look for changes in a few familiar drivers:

→ How U.S. growth compares with the rest of the world

→ Whether dollar assets continue offering attractive real returns

→ How predictable policy remains over time

As these inputs evolve, capital allocation naturally adapts.

This is a healthy and ongoing process within global markets — not a signal of instability.

SPONSOR BREAK presented by BehindtheMarkets*

A U.S. “birthright” claim worth trillions – activated quietly

A tiny government task force working out of a strip mall just finished a 20-year mission.

And with almost no media coverage, they confirmed one of the largest U.S. territorial expansions in modern history…

A resource claim worth an estimated $500 trillion.

Thanks to sovereign U.S. law, this isn’t just a national asset.

It’s an American birthright.

That means every citizen now has the legal right to stake a claim…

But very few even know the opportunity exists.

If you want to see how you can get in line for your portion of this record-breaking windfall…

I’ve assembled everything you need to see inside a new, time-sensitive briefing:

Get all the details here – while the claim window remains open.

A Fresh Signal From the Fed

Another piece of the puzzle landed today.

The Federal Reserve left interest rates unchanged at its first meeting of 2026, keeping the benchmark range at 3.5%–3.75% after three straight cuts last year. Two officials wanted another quarter-point cut, but the broader group chose to stay patient.

At the same time, policymakers quietly upgraded their view of the economy from “moderate” to “solid,” pointing to stronger growth momentum, while still acknowledging that inflation hasn’t fully cooled.

Translation: the Fed isn’t hitting the gas — and it isn’t slamming the brakes either.

Rates aren’t being rushed lower. Growth still looks healthy. Inflation is behaving… but not perfectly. And the committee keeps emphasizing that decisions will follow the data, not headlines.