CATEGORY

Getting started

The First Post-Buffett Shock

The New Era.

For decades, Berkshire Hathaway was one of the few things investors felt they understood. Warren Buffett bought businesses with durable advantages, held them forever, ignored the noise, and let compounding do the heavy lifting.

The playbook rarely changed.

Now the person holding that playbook is gone.

And this morning, Greg Abel gave the market its first real glimpse of what Berkshire Hathaway might look like without Warren Buffett calling the shots.

The result?

→ UnitedHealth is out.

→ Amazon is out.

→ Mastercard and Visa are out.

→ Delta and Macy’s are in.

And suddenly, Berkshire looks a lot less predictable.

Here’s the story ⇩

SPONSOR BREAK presented by BrowntoneResearch*

They Consulted Him to Help End “The Pelosi Paradox”

How is Nancy Pelosi worth $413 million on a $174,000 salary?

For decades, the revolving door between Washington and Wall Street kept regular folks like you locked out.

Thanks to a brand-new law…

(One Jeff Brown was consulted by Congressional offices on…)

The “Pelosi Paradox” is coming to a swift end.

And it’s lighting a fuse under an over $2 quadrillion corner of the tech market.

Click here to discover how you could profit from this landmark moment.

In what’s set to be the biggest wealth transfer in America in 53 years.

Buffett’s Portfolio Is Changing

Every quarter, institutional investors managing more than $100 million are required to file something called a 13F — a public document showing the stocks they owned at the end of the quarter.

Usually, nobody outside Wall Street cares.

But Berkshire Hathaway is different.

For decades, Buffett’s filings were treated like investment scripture. Investors studied every addition, every trim, every quiet exit looking for clues about where “The Oracle of Omaha” thought the economy, valuations, and markets were headed next.

But this filing is different.

Because for the first time in decades… it doesn’t really belong to Buffett anymore.

Greg Abel officially became Berkshire Hathaway CEO on January 1, 2026. This filing — showing holdings as of March 31 — is a first glimpse at whether the new CEO will stay true to Buffett’s philosophy or start to put his own stamp on the world’s most famous investment portfolio.

This filing is his opening statement.

What Berkshire sold — fully exited ❌

The biggest headline was UnitedHealth.

Berkshire completely exited its roughly 5 million-share stake in UNH — a position Buffett himself only started building last year.

This was not some ancient Berkshire holding quietly fading away over time. This was one of Buffett’s final major bets before handing the company to Abel.

Now it’s gone.

The market noticed immediately.

UnitedHealth fell sharply after the filing became public, despite the company recently beating earnings estimates and raising guidance.

That’s the strange power Berkshire still has over markets:

→ When Berkshire buys something, investors call it validation.

→ When Berkshire sells something, investors assume there’s a problem.

Even if the business itself hasn’t fundamentally changed overnight.

SPONSOR BREAK presented by BanyanHills*

After “33X” call, Hall of Fame Trader Jon Najarian reveals NEW Tesla prediction…

Jon Najarian put his neck out on national TV for Tesla in 2014… Before Tesla stock flew to peak gains of 3,392% today! But this “33X” call on Tesla might pale in comparison to Jon’s newest prediction about Elon Musk… That a potential $44 TRILLION plan could be coming next.

Click here to see what Jon Najarian is predicting now.

But UnitedHealth wasn’t the only surprise. ❌

Company | Move | Context |

|---|---|---|

UnitedHealth | Full exit | Buffett first bought UNH in Q2 2025 — less than a year ago. Abel sold the entire position. UNH dropped 5% premarket on the news. The stock has been volatile amid rising medical costs and DOJ scrutiny of its billing practices, though it beat Q1 earnings and raised guidance. |

Amazon | Full exit | Berkshire first bought Amazon in 2019 — one of Buffett’s rare tech bets. Abel quietly closed the position entirely in Q1. |

Mastercard | Full exit | One of the great “toll road” stocks — Mastercard takes a small cut of every transaction on its network. Buffett loved this model. Abel sold it all. |

Visa | Full exit | Same story as Mastercard. Berkshire held both payment network giants. Both are now gone. |

Domino’s | Full exit | A relatively recent Buffett addition. Abel did not hold it for long. |

Pool Corp | Full exit | A distributor of swimming pool supplies — one of Buffett’s more unusual picks. Gone under Abel. |

Liberty Latin America | Full exit | A telecom holding in Latin America. Fully exited in Q1. |

Some of those names are especially interesting.

Mastercard and Visa, for example, are exactly the kind of businesses Buffett historically loved — capital-light “toll booth” companies that quietly collect a piece of global commerce every time money moves.

Now both are gone.

Amazon disappearing from the portfolio also stands out because Buffett famously admitted Berkshire was late to big tech. Amazon was one of the rare moments Berkshire fully embraced a modern platform business.

Abel just walked away from it.

Taken together, these moves tell a story Berkshire investors are not used to seeing:

Less permanence.

More repositioning.

More willingness to reverse course quickly.

What Berkshire cut — reduced positions ↓

Company | Move | Context |

|---|---|---|

Chevron | Cut 35.2% | Berkshire has been trimming its Chevron position for several quarters. The energy giant remains a significant holding but is getting smaller. |

Nucor | Cut 39% | The steel manufacturer saw a significant cut — nearly 40% of Berkshire’s position sold in a single quarter. |

SPONSOR BREAK presented by BrownstoneResearch*

While the whole world is watching Elon, the real money is moving somewhere else

When Elon Musk ran a Twitter poll in 2021, Tesla lost $30 billion in a single day.

When he changed the Twitter logo to Dogecoin, the coin surged 30% overnight.

No one alive moves markets the way Elon does.

Larry Benedict — the trader who delivered a 279% return on cash in 2025 — says Elon’s next move is his biggest yet.

And there’s ONE ticker, overlooked by almost everyone, positioned to capture it.

Click here to find out what it is before the “Final Phase” begins.

What Berkshire bought — new positions ↑

Then came the move nobody expected.

Delta Air Lines.

Berkshire revealed a new 39.8 million-share stake in the airline giant — a remarkable decision considering Buffett famously dumped every airline holding during the pandemic and publicly admitted the investment was a mistake.

Buffett spent years avoiding airlines because of their brutal economics:

→ cyclical demand

→ razor-thin margins

→ fuel price shocks

→ labor costs

→ constant competition

Abel clearly sees something differently.

Maybe it’s a bet on consumer resilience.

Maybe it’s confidence in post-pandemic travel demand.

Maybe he simply believes the industry structure has improved.

Whatever the reason, the symbolism matters.

Company | Move | Context |

|---|---|---|

Delta Air Lines | New position | One of Abel’s most surprising moves. Buffett famously sold all airline holdings in 2020 during COVID, calling it a mistake to have ever bought them. Abel just bought 39.8 million shares of Delta. A significant bet on air travel recovery and consumer demand. |

Macy’s | New position | The struggling department store chain that has been closing locations and fighting for relevance against e-commerce for years. An eyebrow-raising addition to the world’s most watched portfolio. |

SPONSOR BREAK presented by Paradigm*

Altucher: This is My Favorite FREE Starlink Pre-IPO Ticker

Legendary investor James Altucher just gave out one of his TOP stock picks for the coming Starlink IPO – 100% FREE.

Usually he holds these plays “close to the vest”…

But with Starlink going public as soon as June 9th…

NOW is the time to act.

You can watch James’ latest video for yourself, right here.

It’s a brief, 3-minute video, and reveals the name and ticker symbol for FREE.

Click here to check it out now.

What Berkshire added to — increased positions ↑

Company | Move | Context |

|---|---|---|

Alphabet | Increased | Abel added to Berkshire’s Alphabet position — a tech bet that signals some comfort with AI-era big tech, even as Amazon was being sold. |

New York Times | Increased | Berkshire has had a long relationship with media and journalism — Buffett owned newspapers for decades. Abel adding to the NYT position suggests that thread continues. |

The portfolio suddenly looks more cyclical… more consumer-driven… and more willing to rotate with changing conditions than the classic Buffett-era Berkshire most investors grew up with.

SPONSOR BREAK presented by BanyanHill*

$44 Trillion “Super Convergence”: Elon’s Biggest Move EVER?

After being invited to the SpaceX launch headquarters in Cape Canaveral from one of Elon’s top lobbyists… Hall of Fame Trader Jon Najarian now says EVERYONE is missing an even bigger story about the SpaceX IPO… That it’s just the start of an Elon Musk $44 trillion “Superconvergence…” An event that could kick off as soon as June 9th.

Click here now to watch hall of fame trader Jon Najarian’s full prediction.

The Bigger Shift

The most important thing about this filing is not any individual stock.

It’s the tone.

For decades, Berkshire investors felt like they understood the rules:

→ Buy great businesses.

→ Ignore short-term noise.

→ Hold forever.

Greg Abel’s first filing introduces something new: unpredictability.

And markets are still trying to figure out whether that is exciting… or dangerous.

1 Maybe Abel saw risks in UnitedHealth Buffett underestimated.

2 Maybe Delta becomes one of Berkshire’s best-performing positions over the next decade.

3 Or maybe the new CEO simply wanted to make one thing unmistakably clear from the beginning:

This is his portfolio now.

And the new manager just introduced himself.

Don’t forget to to cast your vote 👇

Lesson Of The Day:

Was this email forwarded to you? Don’t miss out on future stories — subscribe using the button below.

Also, help your friends blossom this spring! Share us with them.

💬 We Want To Hear Your Story:

Got a market or stock you want us to analyze next?

Just drop your request in the comments here.

P.S. – If you no longer want to receive occasional emails from us and you want to unsubscribe, click here 👉 “Unsubscribe” . Thank you!

Who Wins When SpaceX Goes Public?

Retail investors are waiting for SpaceX. Wall Street isn’t.

Because before the biggest IPO in years even files publicly, money is already flowing into the companies orbiting around it.

→ Rocket builders.

→ Satellite operators.

→ Signal intelligence firms.

→ Space infrastructure plays.

Some are doubling revenue.

Most are still building before the profits arrive.

All of them are racing to establish their niche in the space economy before SpaceX hits public markets.

The race already started.

Here’s the story ⇩

SPONSOR BREAK presented by BrownstoneResearch*

While the whole world is watching Elon, the real money is moving somewhere else

When Elon Musk ran a Twitter poll in 2021, Tesla lost $30 billion in a single day.

When he changed the Twitter logo to Dogecoin, the coin surged 30% overnight.

No one alive moves markets the way Elon does.

Larry Benedict — the trader who delivered a 279% return on cash in 2025 — says Elon’s next move is his biggest yet.

And there’s ONE ticker, overlooked by almost everyone, positioned to capture it.

Click here to find out what it is before the “Final Phase” begins.

The Ones Building Rockets

1 Rocket Lab RKLB ( ▼ 5.87% )– The SpaceX doppelganger

Of all the publicly traded space companies, Rocket Lab is the one most often compared to SpaceX.

It builds rockets today with its Electron launch vehicles, while developing its larger Neutron rocket — designed to carry heavier payloads to orbit, much like SpaceX’s Falcon system.

But Rocket Lab has already evolved beyond launches.

Its space systems division — selling satellite parts, kick-stage engines, and entire satellites — now generates twice the revenue of its launch business.

→ Q1 revenue is expected to rise 54.5% to $189.4 million, while losses continue narrowing.

Growing fast.

Still not profitable.

2 Firefly Aerospace FLY ( ▼ 4.6% ) – The moon lander

Firefly recently accomplished something most private aerospace companies never do.

It landed on the Moon.

Revenue is beating expectations and guidance is decent.

The company is now valued around $5.5 billion and sits at the center of growing investor interest around lunar infrastructure and defense-related launches.

Revenue is improving and guidance remains solid.

But profitability is nowhere close.

Firefly is still burning cash aggressively while trying to scale a business that requires enormous upfront investment.

B. Riley analyst Mike Crawford maintains a $60 price target.

The question with Firefly is not whether the technology works.

It is whether the business model catches up before the runway runs out.

SPONSOR BREAK presented by Paradigm*

Altucher: This is My Favorite FREE Starlink Pre-IPO Ticker

Legendary investor James Altucher just gave out one of his TOP stock picks for the coming Starlink IPO – 100% FREE.

Usually he holds these plays “close to the vest”…

But with Starlink going public as soon as June 9th…

NOW is the time to act.

You can watch James’ latest video for yourself, right here.

It’s a brief, 3-minute video, and reveals the name and ticker symbol for FREE.

Click here to check it out now.

The Ones Watching From Orbit 🛰️

1 BlackSky BKSY ( ▼ 9.17% ) – The eye in the sky

BlackSky operates a constellation of AI-enhanced Earth observation satellites, on track to become the world’s largest very high-resolution constellation by end of 2026.

Its satellites can image objects as small as 35 centimeters across — four to six times sharper than Planet Labs, its main competitor.

The company believes demand for real-time geospatial intelligence will surge as governments and corporations increasingly rely on satellite data.

The financial picture is less exciting.

Q1 revenue is expected to decline 8% year over year to $27.3 million, while losses widen.

Strong technology.

More difficult near-term execution.

2 Redwire RDW ( ▲ 0.5% ) – The infrastructure supplier

Redwire makes the components that make satellites work.

→ Solar arrays.

→ Docking systems.

→ Sensors.

→ Cameras.

Think of it as a behind-the-scenes supplier for orbital infrastructure.

Last year the company made a major move by acquiring drone firm Edge Autonomy for $925 million — expanding aggressively into autonomous defense systems.

→ That acquisition is expected to drive Q1 revenue growth of nearly 70% to $104.6 million.

Profitability, however, remains a future goal.

The company is still in expansion mode.

SPONSOR BREAK presented by MarketWise*

Wall St. Insider Warns: This Could Leapfrog Elon’s SpaceX IPO

Elon Musk could take SpaceX public in 2026, at an estimated $1.75 trillion valuation. The IPO would include Elon’s AI model, Grok. But according to Louis Navellier, a radical new AI model will launch this year… over 1,000 times more powerful than Elon’s. And the company behind it could outperform SpaceX in the process.

Click here for full details (including Louis’ new pick — free).

3 HawkEye 360 HAWK ( ▲ 0.94% ) – The listener

We covered HawkEye in depth on Wednesday — the company that uses satellites to listen to radio frequency signals from space.

It raised $416 million in its IPO last week, priced at the top of its range, and jumped 30% on day one.

The Iran war has made signals intelligence one of the most valuable commodities in defense right now, and HawkEye’s government customer base is not going anywhere.

Currently trading at 26x revenue — a premium that reflects both the quality of the business and the heat of the moment.

SPONSOR BREAK presented by BanyanHill*

$44 Trillion “Super Convergence”: Elon’s Biggest Move EVER?

After being invited to the SpaceX launch headquarters in Cape Canaveral from one of Elon’s top lobbyists… Hall of Fame Trader Jon Najarian now says EVERYONE is missing an even bigger story about the SpaceX IPO… That it’s just the start of an Elon Musk $44 trillion “Superconvergence…” An event that could kick off as soon as June 9th.

Click here now to watch hall of fame trader Jon Najarian’s full prediction.

The Honest Picture

Here’s the part investors need to understand.

→ Rocket Lab Q1 revenue growth → +54.5%

→ Redwire Q1 revenue growth → +70%

→ BlackSky Q1 revenue growth → -8%

→ HawkEye IPO day-one move → +30%

Companies consistently profitable → Almost none

Revenue across the sector is growing.

Profitability is a different story entirely — building the future is expensive.

That doesn’t necessarily mean these are bad businesses.

It means most of them are still early.

Building rockets, deploying satellites, and creating space infrastructure is enormously capital intensive.

The SpaceX Effect

Here is the question every investor in the sector is wrestling with right now.

What happens when SpaceX finally arrives?

The company is targeting a valuation north of $1.75 trillion and could raise as much as $75 billion in what may become the largest IPO in history.

Its private market valuation has already exploded higher over the last few years.

Meanwhile, Wall Street is already preparing for it.

Nine space-related ETFs have launched or filed in just the past three months.

The infrastructure around the IPO is being built before the IPO itself even exists.

And when SpaceX finally lands in public markets, two very different outcomes could emerge.

Don’t forget to to cast your vote 👇

Lesson Of The Day:

Was this email forwarded to you? Don’t miss out on future stories — subscribe using the button below.

Also, help your friends blossom this spring! Share us with them.

💬 We Want To Hear Your Story:

Got a market or stock you want us to analyze next?

Just drop your request in the comments here.

P.S. – If you no longer want to receive occasional emails from us and you want to unsubscribe, click here 👉 “Unsubscribe” . Thank you!

One ship. One virus. Six stocks. 72 hours.

The Headline That Lit The Match

Earlier this month, passengers aboard the MV Hondius started getting sick while crossing the Atlantic.

Health officials later identified suspected cases tied to the Andes strain of hantavirus. A few deaths were reported. Two Americans were transported in biocontainment units.

The setup looked familiar.

COVID permanently rewired how markets react to health scares.

Back in 2020, the biggest money was made when vaccine names started ripping before the rest of Wall Street fully understood what was happening.

So now, every time a virus story hits the tape, traders immediately ask the same question:

“Which stock moves first if this becomes bigger?”

That reflex kicked in almost instantly last week.

Here’s the story ⇩

SPONSOR BREAK presented by BanyanHill*

44 Trillion “Super Convergence”: Elon’s Biggest Move EVER?

After being invited to the SpaceX launch headquarters in Cape Canaveral from one of Elon’s top lobbyists… Hall of Fame Trader Jon Najarian now says EVERYONE is missing an even bigger story about the SpaceX IPO… That it’s just the start of an Elon Musk $44 trillion “Superconvergence…” An event that could kick off as soon as June 9th.

Click here now to watch hall of fame trader Jon Najarian’s full prediction.

First — what is hantavirus? 🦠

Earlier this month, passengers aboard the MV Hondius — a cruise ship crossing the Atlantic — started getting sick.

Health officials identified seven cases of the Andes strain of hantavirus. Three people died. Seventeen American passengers were repatriated, two of them in biocontainment units.

Hantavirus in plain English: Hantaviruses are a family of viruses spread primarily by rodents. Most strains cannot pass between people at all. The Andes strain — found mainly in Argentina and Chile — is one of the rare exceptions where limited human-to-human transmission has been documented.

The WHO, CDC, and every major health organization said the same thing:

→ this is not another COVID.

→ It does not spread through the air.

→ It requires close, prolonged physical contact.

→ The total number of confirmed cases on the ship was seven.

That did not stop the market from reacting like it might be. ⇩

SPONSOR BREAK presented by BrownstoneResearch*

Millionaire warns: “Move your money now.”

Larry Benedict generated $274 million in profits for his clients by knowing where money flows when the Federal Reserve shifts.

He says Trump’s Fed Takeover is triggering the most significant shift in U.S. markets in nearly 20 years.

He’s already identified the one ticker he expects billions to flood into… and he’s giving away the name for free.

Click here to get the full details before the window closes.

The stocks — one by one

1 Moderna MRNA ( ▼ 0.77% ) – The most connected play

→ +12% Fri – May 8

→ +8% Mon AM – May 11

→ -3.6% Mon PM – May 11

Moderna is the only company in this group with a documented, active connection to hantavirus research. It disclosed that it has been conducting preclinical research on hantaviruses in collaboration with the US Army Medical Research Institute of Infectious Diseases and the Vaccine Innovation Center at Korea University — research that predates the outbreak entirely.

Moderna also lists both “Hantaan virus” and “Hantaviruses causing Hanta Pulmonary Syndrome” as permitted pathogens on its mRNA Access program, which lets researchers use its technology to develop vaccines. The mRNA platform that powered its COVID vaccine is theoretically adaptable to new pathogens quickly.

That is the real bull case here — not this specific outbreak, but the platform’s ability to respond to whatever comes next.

The reality check: analysts at Evercore ISI were blunt. “Hantavirus is a low-incidence, structurally small market. We see no meaningful revenue opportunity.”

Even if Moderna fast-tracked a vaccine, the total addressable market is a fraction of a fraction of what COVID represented.

→ Moderna sold $18.4 billion in vaccines in 2021. A hantavirus vaccine would not move that needle.

● Connection: Real — but revenue opportunity is minimal.

SPONSOR BREAK presented by MarketWise*

Massive 512,000-Line Data Leak Exposes Shocking AI Breakthrough

60-year Wall Street veteran and financial technology pioneer Marc Chaikin recently reviewed a massive data leak inside one of the world’s biggest AI labs. He discovered a hidden mechanism in the code that could create extraordinary wealth for savvy investors – and inflict grave financial hardships on everyone else. Click here for the full story.

2 Inovio Pharmaceuticals INO ( ▲ 1.49% ) – The 2011 grant story

Spiked premarket → -3.1% by close

Inovio’s connection to hantavirus is real — but old.

In 2011, the company received a US Defense Department grant to develop a device for delivering DNA vaccines, intended for testing against the Hantaan virus and other pathogens.

In 2015, several Inovio employees co-authored a paper evaluating the device’s efficacy, concluding it was a low-cost tool for rapid mass vaccination. Sounds promising.

The catch: that was 2015. Inovio has never produced a commercial product from this research — not a vaccine, not a treatment, not a single approved product tied to hantavirus.

The stock moved on a fifteen-year-old grant and a paper that never became a product.

● Connection: Technically real — commercially nonexistent.

3 Novavax NVAX ( ▲ 1.3% ) – The COVID association play

Spiked premarket → -5.4% by close

Novavax has no active hantavirus program. No research. No grants. No pipeline.

It moved purely because it was a COVID-era standout — the sole provider of an approved non-mRNA vaccine during the pandemic.

The market saw “health scare” and bought the last vaccine company it remembered winning.

By Monday afternoon, investors appeared to remember that association is not the same as relevance. Novavax gave back more than anyone else in the group.

● Connection: None — purely a COVID memory trade.

SPONSOR BREAK presented by Paradigm*

Altucher: This is My Favorite FREE Starlink Pre-IPO Ticker

Legendary investor James Altucher just gave out one of his TOP stock picks for the coming Starlink IPO – 100% FREE.

Usually he holds these plays “close to the vest”…

But with Starlink going public as soon as June 9th…

NOW is the time to act.

You can watch James’ latest video for yourself, right here.

It’s a brief, 3-minute video, and reveals the name and ticker symbol for FREE.

Click here to check it out now.

4 QuidelOrtho QDEL ( ▲ 3.08% )– The diagnostic play

Moved on diagnostic testing demand thesis

QuidelOrtho makes diagnostic testing equipment — the kind used to identify viruses quickly in clinical settings.

The thesis here is straightforward: if hantavirus spreads, demand for rapid diagnostic tests goes up, and QuidelOrtho is positioned to supply them. A reasonable logic chain, but one that requires a scale of outbreak that health officials say is extremely unlikely to materialize.

● Connection: Logical — but depends on an outbreak that experts say will not happen.

5 3M MMM ( ▼ 1.35% ) – The N95 play

Moved on PPE demand thesis

3M is one of the world’s largest suppliers of N95 respirator masks that became impossible to find in early 2020.

The hantavirus trade swept it up on the same PPE demand logic that drove mask manufacturers during COVID.

Like QuidelOrtho, the connection is real but contingent on a scale of outbreak that the evidence does not currently support.

● Connection: Real product — wrong scale of outbreak.

5 Carnival, Royal Caribbean & cruise stocks – The obvious losers

Declined on outbreak news

While biotech stocks spiked, cruise lines moved in the opposite direction — the most intuitive trade of the whole episode.

A virus originating on a cruise ship is bad for cruise ship bookings. The broader concern is that fearful travelers may get cold feet about upcoming trips.

However, analysts noted that cruise lines are already facing a much bigger headwind from spiking energy prices driven by the Iran war. Hantavirus added noise to an already difficult backdrop.

● Connection: Direct — but energy costs are the bigger problem

The Pattern:

What happened last week is not unusual.

Fear arrives faster than analysis. By the time the analysis catches up, the trade has already run.

The stocks that move most in these moments are not always the ones with the strongest connection to the actual event. They are the ones the market most strongly associates with the last time something similar happened.

The honest takeaway from last week is about how fear trades work — and how quickly the market corrects itself when the facts do not match the fear.

Don’t forget to to cast your vote 👇

Lesson Of The Day:

Was this email forwarded to you? Don’t miss out on future stories — subscribe using the button below.

Also, help your friends blossom this spring! Share us with them.

💬 We Want To Hear Your Story:

Got a market or stock you want us to analyze next?

Just drop your request in the comments here.

P.S. – If you no longer want to receive occasional emails from us and you want to unsubscribe, click here 👉 “Unsubscribe” . Thank you!

Not SpaceX

The Trade Before the Trade

Everyone is staring at the menu waiting for SpaceX. But while you were deciding what to order, the appetizer just arrived — and it jumped 30% on the first day.

HawkEye 360 raised $416 million, priced at the top of its range, and immediately traded higher.

Not a household name and not a massive revenue story.

But a very clean signal.

Today we talk about HawkEye 360… and tomorrow we talk about the main course.

Here’s the story ⇩

SPONSOR BREAK presented by BrownstoneResearch*

Larry Benedict generated $274 million for his clients by finding the trade most missed.

He says The Final Phase of Elon’s Master Plan is about to trigger one of the biggest wealth transfers in market history.

He’s already identified the ONE ticker positioned to capture it. It isn’t SpaceX, Tesla, or anything you’d expect.

He’s giving away the name, free.

Click here to get the full details before the window closes.

The “Ears” in Orbit

Most satellites look down at earth.

HawkEye 360’s satellites listen.

The company operates a constellation of more than 30 satellites in low earth orbit, all designed to detect, locate, and analyze radio frequency emissions from anywhere on the planet.

Every ship, aircraft, military unit, and piece of electronic equipment on earth emits some kind of radio signal.

HawkEye HAWK ( ▲ 0.46% ) collects those signals, analyzes them, and sells the intelligence to the people who need it most:

→ defense agencies,

→ intelligence services, and

→ national security organizations around the world.

Founded in 2015 and based in Herndon, Virginia, HawkEye has spent a decade building its satellite constellation and its relationships with US government agencies. In December it acquired ISA, a firm specializing in signal processing and classified intelligence systems, deepening its ties with agencies that cannot be named publicly but whose budgets are not shrinking anytime soon.

SPONSOR BREAK presented by Paradigm*

Altucher: This is My Favorite FREE Starlink Pre-IPO Ticker

Legendary investor James Altucher just gave out one of his TOP stock picks for the coming Starlink IPO – 100% FREE.

Usually he holds these plays “close to the vest”…

But with Starlink going public as soon as June 9th…

NOW is the time to act.

You can watch James’ latest video for yourself, right here.

It’s a brief, 3-minute video, and reveals the name and ticker symbol for FREE.

Click here to check it out now.

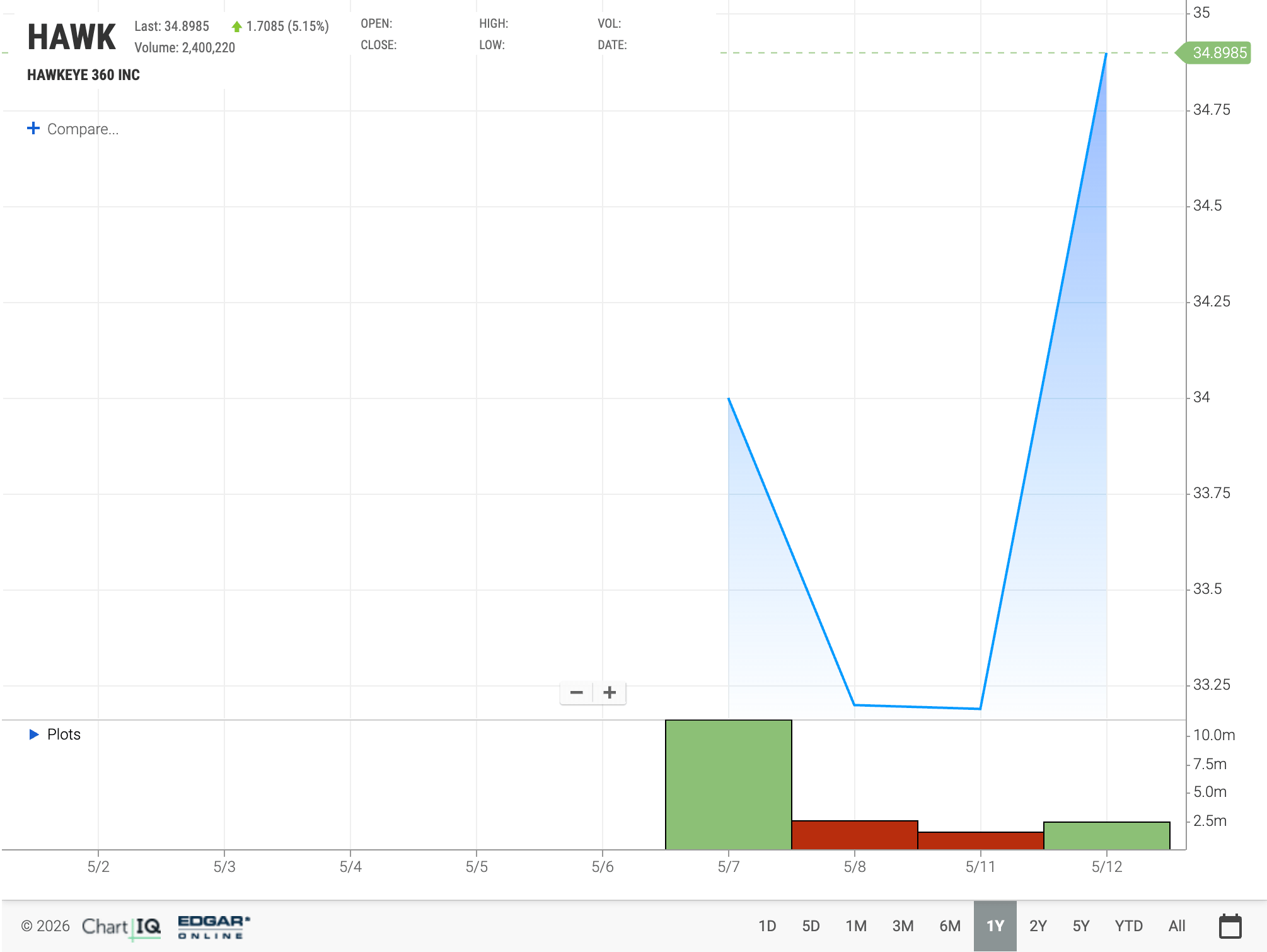

The IPO (what just happened)

Here’s how the debut played out:

→ IPO price: $26

→ Open: ~$33.8

→ Day-one move: +30%

→ Capital raised: $416M

→ Valuation: ~$3.15B

Two things stand out immediately:

It priced at the top of the range

It still popped hard on open

That combination usually means one thing:

institutional demand was strong before it even started trading

Goldman Sachs, Morgan Stanley, RBC Capital Markets, and Jefferies were among the underwriters — a blue-chip lineup that tells you the serious money took this listing seriously.

SPONSOR BREAK presented by BanyanHill*

$44 Trillion “Super Convergence”: Elon’s Biggest Move EVER?

After being invited to the SpaceX launch headquarters in Cape Canaveral from one of Elon’s top lobbyists… Hall of Fame Trader Jon Najarian now says EVERYONE is missing an even bigger story about the SpaceX IPO… That it’s just the start of an Elon Musk $44 trillion “Superconvergence…” An event that could kick off as soon as June 9th.

Click here now to watch hall of fame trader Jon Najarian’s full prediction.

The Valuation Question 🤔

This is where the story shifts.

HawkEye generates roughly:

→ ~$117M in revenue

→ ~$3.1B valuation

Which puts it at: → ~26x its annual revenue of $117 million.

To put that in context:

→ U.S. software average: trades at ~3.7x revenue

→ Even HawkEye’s closest peers in the defense tech space trade at around ~5.3x.

HawkEye is trading at five times that peer average.

What does 26x revenue actually mean?

When you buy a stock at 26x revenue, you are not paying for what the company earns today. You are paying for what you believe it will earn in the future, not current scale.

SPONSOR BREAK presented by BanyanHill*

Pre-IPO Access to America’s Top AI Defense Startup — for $50.

No waiting lists. No special status.

Just one 4-letter ticker that gives you a seat at the table.

Click here now to get the ticker + 3 steps to invest.

Bull vs Bear

1 The bull case is straightforward.

The Iran war has made signals intelligence one of the fastest-growing areas in defense spending. HawkEye’s customer base — US government and allied nations — is not going anywhere. And the company is still early in building out its constellation, meaning revenue should grow significantly as more satellites come online.

2 The bear case is equally clear.

At 26x revenue, a lot of that future growth is already priced in. If defense procurement priorities shift, if a larger competitor enters the space, or if growth disappoints, the valuation has a long way to fall. Government contracts are sticky — until they are not.

Neither case is obviously right. Both deserve to be taken seriously.

The SpaceX Connection 🚀

HawkEye did not go public in a vacuum.

The entire space technology sector is holding its breath waiting for SpaceX — the most anticipated IPO in years, targeting a valuation of over $1.75 trillion and a raise as large as $75 billion.

When SpaceX eventually files publicly, it will be the loudest rocket in a room that is already getting very crowded.

HawkEye’s debut tells us something important about that moment.

The market is hungry for space defense technology.

Institutional investors are willing to pay a significant premium for companies with government relationships and proprietary technology.

A 30% first-day pop at the top of the range is a preview of the appetite that exists for the right kind of space story.

What HawkEye cannot tell us is whether that appetite will survive the SpaceX listing itself. When a $1.75 trillion company enters the room, smaller players often get overshadowed — not because they are worse businesses, but because the oxygen in the room suddenly goes somewhere else.

Or SpaceX’s listing could do the opposite — validate the entire sector and lift every space stock alongside it. It has happened before in other industries when a dominant player goes public and draws fresh attention to the whole ecosystem.

Nobody knows which way it goes.

→ But HawkEye just proved the table is set.

!!! Tomorrow we talk about the main course. 👀

Don’t forget to to cast your vote 👇

Lesson Of The Day:

Was this email forwarded to you? Don’t miss out on future stories — subscribe using the button below.

Also, help your friends blossom this spring! Share us with them.

💬 We Want To Hear Your Story:

Got a market or stock you want us to analyze next?

Just drop your request in the comments here.

P.S. – If you no longer want to receive occasional emails from us and you want to unsubscribe, click here 👉 “Unsubscribe” . Thank you!

This IPO Runs on Coffee

The Habit…

Most people don’t think about capital markets at 7:30 in the morning.

They’re thinking about coffee — how fast they can get it, whether the line is moving, if their usual order is already waiting.

What feels like a routine… is actually one of the most efficient cash-flow machines in America.

And now, it’s heading back to Wall Street.

Dunkin’ is preparing to go public again — this time inside a private equity-built restaurant portfolio that looks a lot bigger than it actually is.

On paper, it’s diversification.

In reality, it’s something else.

Here’s the story ⇩

SPONSOR BREAK presented by Mode Mobile**

The Next Breakout Might Be in Your Pocket

Everyone’s hunting for the next Unicorn.

The type of “category disruptor” that grows fast and turns early believers into big winners.

59,000+ investors think that Mode Mobile could be one of those rare finds.

Americans spend 4 ½ hours on their phones daily, and Mode Mobile is monetizing that screentime. With $1B+ earned by over 490M customers and 32,481% revenue growth, Mode’s EarnPhone is turning smartphones into income generating assets.

Their previous raises sold out, and the company is now offering pre-IPO shares at $0.50/share with up to 20% bonus, exclusive to early investors.

Being early is everything, and this window is still open.

>> Review the offer before it closes

Disclaimers *Please read the offering circular and related risks at invest.modemobile.com.

Mode Mobile recently received their ticker reservation with Nasdaq ($MODE), indicating an intent to IPO in the next 24 months. An intent to IPO is no guarantee that an actual IPO will occur.

The Deloitte rankings are based on submitted applications and public company database research, with winners selected based on their fiscal-year revenue growth percentage over a three-year period.

**Please read InvestingPie, LLC’s full disclaimer in the footer.

The Dunkin’ Paradox

Inspire Brands presents itself as a collection of major restaurant concepts — six brands, global reach, billions in revenue. Structurally, it should behave like a diversified portfolio.

But diversification only works when each piece can stand on its own.

Here, one piece clearly does more than the rest.

Dunkin’ isn’t just part of the portfolio — it is the portfolio. The rest adds scale, but not equal contribution.

Dunkin’ has also been the only brand genuinely investing in its future. Since 2021 it has been rolling out next-generation stores with mobile order pickup, digital kiosks, and drive-thru upgrades — scaling from 1,000 updated locations to 4,000 by mid-2024.

The honest version of this IPO is not “buy a restaurant empire.” It is “buy Dunkin’ — and get five other brands you did not ask for.”

That is not necessarily bad. But it is worth knowing.

The Setup (what you’re actually looking at)

On paper, this is what the market is being asked to price:

→ ~33,300 locations globally

→ ~$33.4 billion in systemwide sales

→ ~$20 billion target valuation

Looks like scale.

Looks like diversification.

The Reality (what’s actually driving it)

Underneath that, the picture gets a lot simpler:

→ ~50% of the entire system = Dunkin’

→ $12.5 billion in U.S. sales alone

→ More than 2× Sonic

→ Nearly 3× Arby’s

→ Both Sonic and Arby’s declining year-over-year

That’s not diversification.

That’s concentration… with branding.

SPONSOR BREAK presented by Mode Mobile**

The Next Breakout Might Be in Your Pocket

Everyone’s hunting for the next Unicorn.

The type of “category disruptor” that grows fast and turns early believers into big winners.

59,000+ investors think that Mode Mobile could be one of those rare finds.

Americans spend 4 ½ hours on their phones daily, and Mode Mobile is monetizing that screentime. With $1B+ earned by over 490M customers and 32,481% revenue growth, Mode’s EarnPhone is turning smartphones into income generating assets.

Their previous raises sold out, and the company is now offering pre-IPO shares at $0.50/share with up to 20% bonus, exclusive to early investors.

Being early is everything, and this window is still open.

>> Review the offer before it closes

Disclaimers *Please read the offering circular and related risks at invest.modemobile.com.

Mode Mobile recently received their ticker reservation with Nasdaq ($MODE), indicating an intent to IPO in the next 24 months. An intent to IPO is no guarantee that an actual IPO will occur.

The Deloitte rankings are based on submitted applications and public company database research, with winners selected based on their fiscal-year revenue growth percentage over a three-year period.

**Please read InvestingPie, LLC’s full disclaimer in the footer.

The PE Playbook

This setup didn’t happen by accident.

In 2020, Roark Capital took Dunkin’ private for $11.3 billion. At the time, the company wasn’t broken — it was simply undervalued relative to what it could become.

That’s where private equity operates best.

1 Take the asset off the public market.

2 Improve what actually drives value.

3 Bring it back when the story is cleaner.

For Dunkin’, that meant focusing on efficiency — not reinvention.

Over the past few years:

→ Store formats were upgraded

→ Digital ordering expanded

→ Drive-thru throughput improved

The business didn’t change at its core. It just got better at what it already did.

Six years later, Roark wants to sell. And the asking price is $20 billion — nearly double what they paid.

The IPO Window

Inspire isn’t stepping into the market alone.

A growing list of companies that stayed private through 2025 are starting to move:

→ Jersey Mike’s filed for an IPO last month, targeting a valuation of at least $12 billion.

→ SpaceX is reportedly planning a listing that could value the company at over $1 trillion.

→ Several other consumer and retail companies have already gone public this year after a long drought.

The IPO market, which was essentially frozen through most of 2025 due to tariff uncertainty and market volatility, is thawing.

It is worth watching how the first few big listings actually trade before getting too excited.

SPONSOR BREAK presented by Paradigm*

Altucher: This is My Favorite FREE Starlink Pre-IPO Ticker

Legendary investor James Altucher just gave out one of his TOP stock picks for the coming Starlink IPO – 100% FREE.

Usually he holds these plays “close to the vest”…

But with Starlink going public as soon as June 9th…

NOW is the time to act.

You can watch James’ latest video for yourself, right here.

It’s a brief, 3-minute video, and reveals the name and ticker symbol for FREE.

Click here to check it out now.

The Timing Problem

But the backdrop isn’t entirely clean.

At the same time this IPO is coming together, some of the strongest operators in the space are starting to flag pressure on the consumer.

Higher gas prices.

Tighter budgets.

More selective spending.

Even companies like McDonald’s and Domino’s — which tend to hold up well across cycles — are acknowledging the shift.

Fast food sits in an interesting middle ground.

It feels essential.

But behaves like discretionary when conditions tighten.

Gas is heading toward $5 a gallon nationally. When that happens, the first thing consumers cut back on is discretionary spending.

Dunkin’ has proven more resilient, partly because its average ticket is lower than competitors and partly because coffee is the last habit people give up.

But the environment still matters.

And right now, those conditions are stable… but not easy.

Don’t forget to to cast your vote 👇

Lesson Of The Day:

Was this email forwarded to you? Don’t miss out on future stories — subscribe using the button below.

Also, help your friends blossom this spring! Share us with them.

💬 We Want To Hear Your Story:

Got a market or stock you want us to analyze next?

Just drop your request in the comments here.

P.S. – If you no longer want to receive occasional emails from us and you want to unsubscribe, click here 👉 “Unsubscribe” . Thank you!

AI… or Just a Better Story?

… just add AI.

Almost every single earnings call last week mentioned AI. Not once or as a footnote… but as the whole thesis.

→ DoorDash: AI will know what you want for dinner before you do.

→ CrowdStrike: AI will catch your hacker before they know they’ve been caught.

→ McDonald’s: AI is how we’re going to personalize your value meal.

→ Burger King: AI is how we’re going to fix the soda machine experience.

At some point you have to ask — is this a technology revolution or is “AI” just the new way to say “we have a plan” on an earnings call?

Let’s look at two companies where the answer actually matters.

One just proved the demand is real with 933 million orders.

The other is being priced like the proof already arrived — three weeks before they even report.

Here’s the story ⇩

SPONSOR BREAK presented by Brownstone*

Better than SpaceX? Grab this ticker instead.

Larry Benedict generated $274 million for his clients by finding the trade most missed.

He says The Final Phase of Elon’s Master Plan is about to trigger one of the biggest wealth transfers in market history.

He’s already identified the ONE ticker positioned to capture it. It isn’t SpaceX, Tesla, or anything you’d expect.

He’s giving away the name, free.

Click here to get the full details before the window closes.

Hungry?

Doordash DASH ( ▼ 4.03% ) reported 933 million orders in one quarter.

933 million orders… that’s the population of India ordering delivery.

DoorDash beat on earnings.

→ EPS came in at $0.42, beating estimates by 13%.

→ Revenue jumped 33% to $4.04 billion — slightly below forecasts but nobody cared because everything else was on fire.

→ Gross order value hit $31.6 billion, up 37%.

→ Record DashPass memberships.

→ Record monthly active users.

→ More first-time US consumers than any quarter before.

And Deliveroo — the British delivery app everyone thought was a distraction when DoorDash bought it — is now growing at its fastest rate in four years. Without Deliveroo, core GOV still grew 24%.

The mothership is healthy.

The stock jumped on earnings report 10%.

SPONSOR BREAK presented by BanyanHill*

Hidden in Tesla’s Filing: A $12 Billion “Super Startup”

Pull up Tesla’s most recent SEC filing. Page 5.

And you’ll see a single line showing $12 billion in revenue from a brand-new “super startup” Elon Musk has been quietly incubating inside Tesla.

This new “super startup” has nothing to do with cars or robots or space or AI…

But it sits at the center of what Blackstone calls “a $23 trillion investment opportunity.”

And on July 22, Elon is expected to pull back the curtain and reveal exactly what he’s building.

But Adam O’Dell already knows… and he reveals it all in this urgent video.

Built to Predict You

DoorDash’s co-founder and CEO, Tony Xu, has a bigger ambition than delivering your burrito.

He wants DoorDash to know what you want before you do. He calls it “agentic ordering” – AI that learns your habits well enough to order on your behalf.

Your usual Thursday night pad thai, your Sunday morning grocery run, your last-minute birthday cake. All of it, anticipated and handled before you even open the app.

To build that, DoorDash is doing something most companies talk about but never actually do – they’re tearing down their entire platform and rebuilding it from scratch. Several hundred million dollars. Runs into early 2027. Messy, expensive, and completely intentional.

They’re also building something called a digital catalog. Every restaurant dish, every grocery item, every product on every shelf — structured and searchable so an AI can make decisions on your behalf instantly.

That’s the long game.

The short game has a $50 million headache – driver gas relief costs from the Iran war-driven oil surge hitting Q2. Management says they’ll offset it elsewhere.

→ Q2 GOV guidance of $32.4B to $33.4B still came in ahead of Wall Street.

!!! The bull case is simple. DoorDash is no longer just food. It’s grocery, electronics, apparel, auto parts, restaurant reservations through SevenRooms. They’re building the operating system for the physical world. AI is just how they make it feel invisible.

The question is whether invisible is worth the price of rebuilding everything to get there.

SPONSOR BREAK presented by BehindTheMarkets*

Iran War TRUTH: There’s a strategy behind the Iran war.

I know because two private meetings with U.S. Congressmen on March 2nd — three days after the first missiles fell — sent me down a research path I wasn’t expecting.

What I found at the end of it: a coordinated operation, a shadow group running it, and one company at the dead center of all of it.

Click here to see the strategy behind the Iran war.

The market already wrote the ending.

CrowdStrike doesn’t report earnings until June 3.

The stock is already up 28% this month anyway.

CrowdStrike is a cybersecurity company. Their Falcon platform sits on top of companies’ entire digital infrastructure — endpoints, cloud workloads, identity, data — and watches everything in real time. Their AI tool, Charlotte, acts like a security analyst.

→ The business is genuinely strong.

→ Revenue growing 23% year over year.

→ EPS growing 30% annually.

→ They’ve beaten earnings estimates four quarters in a row.

The numbers are not the problem.

The problem is the price you’re paying for those numbers.

→ 98 times forward earnings.

→ A price-to-sales ratio of 24.76x against an industry average of 3.75x.

→ A DCF model that puts fair value at $357 while the stock sits at $468.

The stock is currently priced on what believers think it becomes.

Bull vs Bear.

The market got so excited about their AI story that it didn’t wait for the CrowdStrike numbers.

It just assumed. Priced it in. Moved on. That’s either the most confident trade of 2026 or the most expensive assumption.

Bulls say the stock is worth $692.

Bears say $113.

In short…

Nobody in tech invented anything new last week. AI was everywhere — in the earnings calls, in the guidance, in the stock prices.

DoorDash proved the demand is real. 933 million orders don’t lie.

CrowdStrike is betting the market stays patient long enough for the proof to catch up with the price. At 98x earnings, that’s not a small ask.

The AI revolution is happening. The question is who gets there first — and who was just really good at saying they would. 😉

Don’t forget to to cast your vote 👇

Lesson Of The Day:

Was this email forwarded to you? Don’t miss out on future stories — subscribe using the button below.

Also, help your friends blossom this spring! Share us with them.

💬 We Want To Hear Your Story:

Got a market or stock you want us to analyze next?

Just drop your request in the comments here.

P.S. – If you no longer want to receive occasional emails from us and you want to unsubscribe, click here 👉 “Unsubscribe” . Thank you!

All About The SpaceX IPO

This IPO Breaks Every Rule

The fine print on the SpaceX IPO is extraordinary.

→ You can’t sue.

→ You can’t vote.

→ You can’t fire Musk. The only person who can fire Musk is Musk.

And yet the line to get in stretches around the block.

SpaceX is expected to be the biggest IPO in history:

→ $75 billion in proceeds,

→ a $1.75 trillion valuation, and

→ an unusually generous 30% allocation for retail investors.

That last part almost never happens at this scale. Musk is letting everyday investors in early, which sounds generous until you read what you’re actually agreeing to.

Here’s the story ⇩

SPONSOR BREAK presented by Paradigm*

Altucher: This is My Favorite FREE Starlink Pre-IPO Ticker

Legendary investor James Altucher just gave out one of his TOP stock picks for the coming Starlink IPO – 100% FREE.

Usually he holds these plays “close to the vest”…

But with Starlink going public as soon as June 9th…

NOW is the time to act.

You can watch James’ latest video for yourself, right here.

It’s a brief, 3-minute video, and reveals the name and ticker symbol for FREE.

Click here to check it out now.

The Trade They Won’t Miss Twice

But before we get into the fine print, it’s worth asking why the line is so long in the first place.

One word: Tesla.

Back in 2010, Tesla went public at $17 a share.

Hold that through the noise, the volatility, the near-death moments… and you’re looking at ~42% annualized returns.

And for retail investors who missed it — or didn’t hold long enough — SpaceX feels like a second chance at the same bet.

This year, Tesla has been the second most traded stock by value among retail investors, accounting for roughly 30% to 40% of all discretionary trading volumes.

The “Musk faithful” are not a small group. They’re a market force. And after losing 30% of its value from mid-December to early April, Tesla is already back up 20% in the past month.

So what’s driving it?

→ Could be positioning into earnings.

→ Could be early anticipation around SpaceX.

→ Or it could be something simpler:

The same crowd… coming back.

Because when a trade changes people’s lives once, they don’t forget it.

And when the next version shows up — they don’t want to miss it twice.

SPONSOR BREAK presented by BanyanHill*

The REAL Reason Trump Is Invading Iran

For a moment… Forget about Trump’s ties to Israel. Forget about reports of Iran’s nuclear program.

Because my research has led me to believe we’re risking World War 3 with Iran for a completely different reason.

Click here to find out what it is.

If you have even a single dollar invested in the U.S. stock market, this is going to directly impact you.

Discover the reason here.

The Musk Multiplier

Both Tesla and SpaceX run on the same playbook.

Start with an idea most people dismiss as impossible.

Scale it like it’s inevitable.

Then tie compensation to numbers so big they sound like fiction.

At Tesla, the long-term target sits around $8.5 trillion.

At SpaceX, it’s roughly $7.5 trillion.

For context, the entire U.S. economy is about $28 trillion.

He wants both companies to be worth more than a quarter of that. Combined.

And yet retail is buying. Because Tesla already broke the template once.

And that changes how people process risk the second time around.

So when SpaceX goes public — possibly as soon as June — the question everyone is asking is what happens to Tesla.

→ Does retail trim their position to buy SpaceX?

→ Do they hold both?

→ Or does the excitement around SpaceX actually pull more money into the entire Musk ecosystem?

Nobody agrees.

1 Some experts say nothing changes — two great stories can coexist and retail capital rotates out of other things.

2 Others say something — Tesla holders trim a little, buy SpaceX, end up holding both.

3 And then there’s a third camp that says everybody wins — that SpaceX anticipation is already drawing retail back into Tesla, the same way SPACs pulled retail into anything celebrity-linked in 2021.

Back then, the company didn’t matter.

The association did.

This time, the association is Elon Musk.

And the story… is a lot bigger than cars – this one is aiming for Mars.

SPONSOR BREAK presented MarketWise*

Trump Admin to Pump $1 Billion into this “Off-the-Radar” AI Stock

The U.S. government pumped more than $1 billion into Intel. The stock popped 128%. It pumped $400 million into MP Materials. The stock popped 200%. It bought 10% of Trilogy Metals. The stock popped 500%. And now, Trump has chosen this AI stock for a $1 billion payday.

Click here for the full story and stock pick (free).

One Signature Away

There’s one more detail buried in the structure — and it matters more than it looks.

The same supervoting setup that gives Elon Musk ~83.8% control doesn’t just shape decisions.

It controls outcomes. Including M&A.

Which means, in theory, it opens the door to something bigger:

A potential merger between SpaceX and Tesla.

Two companies that already share the same narrative…

→ the same capital base…

→ and arguably, the same long-term vision.

In practice, they’re separate. But structurally?

They’re one approval away from being something else entirely.

And that’s the part most people skip over.

Now… about that fine print.

SPONSOR BREAK presented by BanyanHill*

Pre-IPO Access to America’s Top AI Defense Startup — for $50.

No waiting lists. No special status.

Just one 4-letter ticker that gives you a seat at the table.

Click here now to get the ticker + 3 steps to invest.

The Fine Print

Here’s what makes this IPO different from almost anything that’s come before it.

SpaceX is structured to move fast and stay focused.

→ No activist investors.

→ No proxy fights.

→ No shareholder proposals slowing things down.

The people building the rockets… stay in control of the rockets.

1 Elon Musk holds roughly 42.5% of the equity… but 83.8% of the voting power, thanks to supervoting shares that carry 10x the influence of a regular share.

So even as a public company, control doesn’t dilute.

The setup goes further.

2 SpaceX is incorporated in Texas — a state that’s been actively rewriting corporate rules to give founder-led companies more freedom to operate without the usual friction.

Disputes don’t play out in public courts.

They go through arbitration — faster, quieter, less disruptive.

3 And if you want a say as a shareholder?

You need real size.

At least $1 million in stock or 3% ownership just to bring a proposal forward.

So the tradeoff is pretty clear.

In short…

History doesn’t repeat itself. But Musk has a habit of making it rhyme.

SpaceX is asking you to believe again. Bigger stage. Same man.

The governance is unconventional. The valuation is enormous. And retail investors are getting a 30% allocation that almost never happens at this scale.

Shang Chou from Dishmi Capital said it best: ‘You focus less on valuation and more on the fact that you’ve been offered a seat on a rocket ship.’

The IPO lands as soon as June. The line forms to the left. 😉

Don’t forget to to cast your vote 👇

Lesson Of The Day:

Was this email forwarded to you? Don’t miss out on future stories — subscribe using the button below.

Also, help your friends blossom this spring! Share us with them.

💬 We Want To Hear Your Story:

Got a market or stock you want us to analyze next?

Just drop your request in the comments here.

P.S. – If you no longer want to receive occasional emails from us and you want to unsubscribe, click here 👉 “Unsubscribe” . Thank you!

The $5 Meal Economy 🍔

Same Menu… Different Reality

Four burger chains reported earnings this week.

→ One is on the best run in years.

→ One is quietly bleeding out.

→ One just went up in smoke.

→ And one is promising it’ll be fine by Christmas.

Welcome to the fast food earnings wars — where your lunch order is somebody’s stock price, the soda machine is a political statement, and a CEO eating a burger on camera can move markets more than a Fed announcement.

Here’s the story ⇩

SPONSOR BREAK presented by BanyanHill*

The REAL Reason Trump Is Invading Iran

For a moment… Forget about Trump’s ties to Israel. Forget about reports of Iran’s nuclear program.

Because my research has led me to believe we’re risking World War 3 with Iran for a completely different reason.

Click here to find out what it is.

If you have even a single dollar invested in the U.S. stock market, this is going to directly impact you.

Discover the reason here.

The Grind Paid Off

Burger King QSR ( ▲ 2.05% ) just had its best run in years.

US same-store sales jumped 5.8% ▲ — about five points ahead of the industry, and nearly two points ahead of McDonald’s.

But this wasn’t one of those “one good quarter” stories. This was four years of work finally showing up.

They called it Reclaim the Flame — a slow rebuild of the business:

→ fixing restaurants

→ cleaning up the menu

→ updating the brand

Nothing flashy. Just consistent upgrades, one piece at a time.

Even the Whopper got an upgrade – new bun, better mayo, fresher toppings.

And…crucially, a box instead of paper wrapping so it stops arriving smushed.

Customers had been asking for that for years.

BK president Tom Curtis listened. Literally. He posted his phone number on TikTok after going viral for taking an enthusiastic bite of the Whopper (the internet loved it), and ended up talking to 1,500 real customers.

His takeaway was simple: This isn’t a growing market. Every gain comes from somewhere else.

This quarter, most of it came from McDonald’s.

Even the soda machine became a signal.

While McDonald’s is pulling back on self-serve refills, Burger King is leaning into it.

“If they want a refill, they can have a refill.”

Nothing about this quarter looked accidental.

It just took a while to show up.

SPONSOR BREAK presented MarketWise*

Trump Admin to Pump $1 Billion into this “Off-the-Radar” AI Stock

The U.S. government pumped more than $1 billion into Intel. The stock popped 128%. It pumped $400 million into MP Materials. The stock popped 200%. It bought 10% of Trilogy Metals. The stock popped 500%. And now, Trump has chosen this AI stock for a $1 billion payday.

Click here for the full story and stock pick (free).

Beat With an Asterisk(*)

On paper, a clean beat.

→ Revenue topped estimates.

→ EPS cleared the bar.

→ US same-store sales grew for the fourth consecutive quarter.

→ Global systemwide sales hit $34 billion.

→ Loyalty program revenue crossed $9 billion across 70 markets.

By any traditional measure, McDonald’s MCD ( ▼ 0.05% ) had a good quarter.

The stock popped about 3% in premarket.

Then the tone shifted.

CEO Chris Kempczinski told analysts the consumer environment “may be getting a little bit worse.”

The pop evaporated.

But the real story isn’t in the beat. It’s in how McDonald’s is winning right now.

Value.

For nearly two years, the company has been stacking options:

→ $5 meal deal in 2024

→ $1 options in January 2025

→ A menu capped under $3 in April

→ $4 breakfast

Not one-off promos. A system built around tighter wallets.

As Kempczinski put it, customers have “a limited amount of money in their pocket.”

Even the Big Arch helped too. The oversized burger launched in March. The CEO’s tasting video made the rounds — mostly for the wrong reasons.

Still drove traffic. Sometimes attention works either way.

Then there’s the soda machine story.

Self-serve soda fountains are being phased out by 2032.

In their place: a new lineup of specialty drinks — refreshers, flavored sodas, customizable options — all priced to compete with chains like Starbucks and Dutch Bros.

The CosMc’s concept didn’t make it.

McDonald’s is the strongest chain in the world at capturing stressed consumers.

And right now, that means value.

The only question is how much further that shift goes.

SPONSOR BREAK presented by BanyanHill*

Pre-IPO Access to America’s Top AI Defense Startup — for $50.

No waiting lists. No special status.

Just one 4-letter ticker that gives you a seat at the table.

Click here now to get the ticker + 3 steps to invest.

The One That’s Bleeding Out.

Under the same RBI umbrella that just delivered Burger King’s best quarter in years, Popeyes is having its worst. The 6.5% comp drop is the biggest in multiple years. And it didn’t happen by accident — it happened by drift.

Here’s the diagnosis, laid out by Popeyes’ new US president Peter Perdue back in February. Think of it like a chain reaction — each failure feeding the next:

1 Step one: Popeyes leaned hard on limited-time offers to bring in new customers. It worked — new guests came in. But the complexity it added to operations was brutal. Service got slower and sloppier. The new guests didn’t come back. Neither did some of the loyal ones.

2 Step two: Chasing LTOs meant losing focus on the Louisiana heritage that made the brand. The core menu got blurry. The messaging got generic. Popeyes started to feel like any other chicken chain.

3 Step three: With identity weakened and service suffering, everyday value eroded. Price-sensitive customers — the backbone of fast food — stopped showing up.

One failure caused the next. → Classic chain reaction.

The fix is underway. Tighter chicken tender specs rolling out system-wide by June — early results show meaningful improvement in customer satisfaction.

→ A $5 Faves value offer.

→ Permanent Chicken Wraps at $3.99.

Kobza says Popeyes can return to positive comps by year-end.

Now the hard part is moving fast enough that customers give it another shot before forming new habits elsewhere.

SPONSOR BREAK presented by InvestorPlace*

Starting June 16, This AI Lab Could Take Off Dramatically

Time magazine recently named this lab “the most disruptive company in the world.” It’s not SpaceX or OpenAI. In fact, its annualized revenues have already surpassed both of these firms. And this 60-year Wall Street legend believes it’s gearing up for a watershed product launch that could send its sales soaring even higher starting June 16.

Click here to learn how you can access a “pre-IPO backdoor” into this firm for just $40 a share.

The One in Smoke.

Shake Shack SHAK ( ▼ 28.92% ) went down 30% in a single session. Worst day in the company’s history.

If you’re looking for what happens when a premium brand runs into a stretched consumer and rising costs at the same time— this is the case study.

The headwinds came from every direction at once.

→ Winter storms hurt Q1 traffic.

→ Beef costs rose in the low teens — record highs driven by dwindling US cattle supplies that have now hit multiple chains.

→G&A expenses jumped from $41M to $54M on marketing and

→ tech investments that didn’t show up in the results.

→ And the Middle East conflict is disrupting its licensed locations in the region — temporary closures, reduced hours, delivery-only operations, slowed inbound tourism at high-traffic locations.

Same-store sales actually grew 4.6%. In most quarters, that’s a good number. But Shake Shack needed 4.7%, and in a quarter where you’ve also swung to an operating loss and missed badly on EPS, almost isn’t close enough.

The structural problem here is what Shake Shack doesn’t have that McDonald’s does: a value floor.

When consumers tighten up, McDonald’s has a value layer to catch them.

Shake Shack doesn’t. There’s no safety net at the bottom of the menu. Premium positioning is a great place to be in a healthy consumer environment. But this isn’t one- with costs climbing and consumers counting dollars.

There’s no buffer.

And not much room to get it wrong.

In short…

What ties all four stories together is simpler than it looks: the consumer is under pressure, and every chain is being stress-tested by it.

Some were ready for it.

McDonald’s and Burger King spent the last few years reinforcing the basics — value, product, consistency.

That work is showing up now.

Disclaimer 😉:

No burgers were harmed in the making of this newsletter.

But a lot of lettuce was reconsidered.

Don’t forget to to cast your vote 👇

Lesson Of The Day:

Was this email forwarded to you? Don’t miss out on future stories — subscribe using the button below.

Also, help your friends blossom this spring! Share us with them.

💬 We Want To Hear Your Story:

Got a market or stock you want us to analyze next?

Just drop your request in the comments here.

P.S. – If you no longer want to receive occasional emails from us and you want to unsubscribe, click here 👉 “Unsubscribe” . Thank you!

Nobody Had These On Their Bingo Card 👀

The Market Finally Caught Up

In 2001, Corning was dying.

The internet bubble had just burst, and demand for fiber optic cables — Corning’s entire business — collapsed almost overnight.

Revenue fell 70% in a single year.

The stock dropped 99% from its peak.

Employees were laid off by the thousands.

The company that had been making specialty glass since 1851 was suddenly fighting for its life.

The painful irony? Corning was not failing because fiber optics was a bad idea. It was failing because the world was not ready for it yet. The infrastructure was being built decades too early — before there was enough internet traffic to justify it, before streaming existed, before anyone had a smartphone in their pocket.

Fast forward 25 years, and Jensen Huang just wrote Corning a $500 million check.

Because the world is finally ready. And this time, there is not enough fiber — not even close.

Here’s the story ⇩

SPONSOR BREAK presented by BanyanHill*

Pre-IPO Access to America’s Top AI Defense Startup — for $50.

No waiting lists. No special status.

Just one 4-letter ticker that gives you a seat at the table.

Click here now to get the ticker + 3 steps to invest.

WHY?

As AI data centers grow bigger and more powerful, the amount of data moving between chips, servers, and buildings becomes almost incomprehensible.

Copper cables — the traditional wiring inside data centers — have a speed and distance problem at that scale.

Fiber optics solves it.

Think of it like this:

Copper is a garden hose. Fiber is a fire hydrant. When you are trying to move the entire internet’s worth of data between AI servers in real time, you need fire hydrants — a lot of them. Nvidia is building the biggest city in history and just realized it is running out of fire hydrants. Corning makes fire hydrants. Jensen just locked in the supply before everyone else figures out they need the same thing.

As part of the deal, Corning GLW ( ▲ 12.01% ) will build three new US factories, expanding optical connectivity manufacturing by 10x and fiber production by 50%.

Nvidia is buying 3 million Corning shares at essentially zero — $0.0001 each — and has warrants to buy 15 million more shares at $180 each within three years.

Translation: if Corning’s stock keeps climbing, Nvidia profits twice. Once from the partnership. Once from the equity.

Corning jumped 12% today and hit an all-time high.

It is already up more than 100% this year.

And most investors still could not pick its ticker out of a lineup.

Worth noting: this is not a one-off. Nvidia has also invested $2 billion each into Marvell MRVL ( ▲ 2.02% ) , Coherent COHR ( ▲ 2.66% ) , and Lumentum LITE ( ▼ 5.06% ) — all fiber and optical communications companies. Jensen is systematically locking in the supply chain that makes his chips actually useful at scale, one check at a time.

SPONSOR BREAK presented by BanyanHill*

The REAL Reason Trump Is Invading Iran

For a moment… Forget about Trump’s ties to Israel. Forget about reports of Iran’s nuclear program.

Because my research has led me to believe we’re risking World War 3 with Iran for a completely different reason.

Click here to find out what it is.

If you have even a single dollar invested in the U.S. stock market, this is going to directly impact you.

Discover the reason here.

Nobody bet on this one.

For the last two years, the spotlight hasn’t really moved.

1 GPUs took it and held it. They trained the models, handled the heavy lifting, and turned Nvidia into the center of the trade. Everything else felt secondary.

2 CPUs were still there — just not part of the conversation.

That’s starting to change.

Advanced Micro Devices AMD ( ▲ 18.62% ) jumped 16% this week, and the focus wasn’t on GPUs. It was on CPUs — the chip that sits inside just about everything.

The shift is subtle, but it’s important.

Training a model is one thing. Running it millions of times a day is something else entirely.

That’s where CPUs start to show up again.

The CPU-to-GPU mix used to lean heavily one way — sometimes as wide as one-to-eight. Now it’s moving closer to even.

That kind of change doesn’t stay isolated.

AMD raised its estimate for the CPU server market to $120 billion by 2030. Analysts adjusted just as quickly.

Nothing flashy about it.

Just a different part of the system getting a lot more attention. 👀

SPONSOR BREAK presented by InvestorPlace*

Trump Just Named His Secret AI Project. It’s Called “Golden Dawn.”

When a secretive project gets a name, it means we’re closer to a breakthrough than most people think. Behind the razor wire of a hidden government lab in Tennessee, 40,000 scientists are finishing work on an AI computer 283 trillion times more powerful than today’s data centers — spanning more than 700 miles and built to speed up AI breakthroughs by 36,000%. When Golden Dawn launches, it could instantly leapfrog ChatGPT, Gemini, and Grok — and trigger a $100 trillion reset of the AI markets. Louis Navellier is revealing the one stock at the center of it — down to the ticker — but only through May 5th.

It Was Supposed to Turn

Micron Technology makes memory chips — the component that allows computers to hold and quickly access information.

Historically, memory has been one of the most punishing businesses in tech. Strong demand, oversupply, collapse… then do it all over again. Investors learned to expect it.

But something broke that cycle.

Micron MU ( ▲ 4.12% ) just crossed a $700 billion market cap. It is up 690% over the past year.

What changed is where the demand is coming from.

Training models is only the first step. Once they’re deployed, they need to constantly read, write, and update information in real time.

That’s a different kind of workload. And it doesn’t really pause.

Companies like Meta, Microsoft, and Apple all pointed to the same pressure last week — rising memory costs.

Three of the largest technology companies on earth.

→ Same complaint. → Same week.

As one analyst put it, the driver this time looks more persistent.

SPONSOR BREAK presented by BanyanHill*

Hidden in Tesla’s Filing: A $12 Billion “Super Startup”

Pull up Tesla’s most recent SEC filing. Page 5.

And you’ll see a single line showing $12 billion in revenue from a brand-new “super startup” Elon Musk has been quietly incubating inside Tesla.

This new “super startup” has nothing to do with cars or robots or space or AI…

But it sits at the center of what Blackstone calls “a $23 trillion investment opportunity.”

And on July 22, Elon is expected to pull back the curtain and reveal exactly what he’s building.

But Adam O’Dell already knows… and he reveals it all in this urgent video.

The landlord lesson…

Hut 8 HUT ( ▲ 35.31% ) started as a bitcoin miner — rows of machines, cheap power, solving math problems for crypto.

Not exactly where you’d expect a $9.8 billion lease to show up.

Somewhere along the way, the business shifted.

Hut 8 realized that what it actually had was something far more valuable than bitcoin: land, power, and the infrastructure to run enormous amounts of compute.

In this market, that’s a different category entirely.

Today, Hut 8 signed a 15-year, $9.8 billion lease for its Texas AI data center campus. The tenant wasn’t named. Just described as “high-investment-grade.”

Someone willing to commit nearly $10 billion without putting their name on it.

The stock jumped 34% before lunch.

Same day, earnings missed expectations.

About today…

Every company that won big today — Corning, AMD, Micron, Hut 8 — is not trying to build artificial intelligence. They are building the physical world that artificial intelligence needs to exist.

→ Fiber to move the data.

→ Memory to hold it.

→ CPUs to process the decisions.

→ Power and land to run it all.

The AI boom is the biggest construction project in human history. And for two years, the market rewarded the architects while largely ignoring the construction crew.

Today, the construction crew had a very good day.

And based on the checks being written, the leases being signed, and the market estimates being doubled overnight — it is just getting started. 👀

Don’t forget to to cast your vote 👇

Lesson Of The Day:

Was this email forwarded to you? Don’t miss out on future stories — subscribe using the button below.

Also, help your friends blossom this spring! Share us with them.

💬 We Want To Hear Your Story:

Got a market or stock you want us to analyze next?

Just drop your request in the comments here.

P.S. – If you no longer want to receive occasional emails from us and you want to unsubscribe, click here 👉 “Unsubscribe” . Thank you!

Applause (Not Included)

When winning is not enough

Imagine you ran a marathon, finished in the top 1%, broke your personal record by 20 minutes, and crossed the finish line to find the crowd booing.