CATEGORY

Getting started

Oops, We Did It Again.

Sometimes the wrong turn is worth $32 billion.

Bravo 👏

It was a practice round at 2020 Augusta National.

The tradition at The Masters is simple: players try to skip their tee shot across the pond in front of the green. You aim low, you hope it bounces, you try to land it somewhere on the putting surface. Most shots skip once or twice and die in the water. That’s the expected outcome. That’s physics.

Jon Rahm‘s ball skipped four times. It kicked to the back of the green. It fed down the slope. And then — in front of exactly nobody, because it was a Tuesday practice round with no crowd — it dropped into the hole.

A hole-in-one. Off a water skip.

He did something that had no business working.

Here is the thing about the skip shot: it only works if the ball goes somewhere it wasn’t supposed to go. The trajectory is wrong by design. The landing zone is technically an error.

And yet, sometimes, the wrong path is the only one that ends in the hole.

Today, I found four stories across the market, and every single one of them involved something that launched correctly — and landed somewhere completely different than planned.

Three of them landed in the water. One of them found the hole. ⇩

SPONSOR BREAK presented by OxfordClub*

How Mitt Romney Turned $450K Into Up to $100 Million (Tax-Free)

It wasn’t stocks. It wasn’t real estate. It was a little-known investment vehicle that turned Mitt Romney’s $450,000 into as much as $100 million and Peter Thiel used to turn $2,000 into $5 billion within two decades. Now, thanks to a new executive order, regular Americans can access the same type of investment. Get more details here >>

Aimed For Orbit. Hit The Pond.

Elon has 9,500+ satellites circling the planet. If one goes sideways, he launches three more next Tuesday before lunch.

AST SpaceMobile is playing a completely different game – and honestly, it’s a bolder one.

Their whole thesis: you don’t need thousands of satellites if each one is smart enough. Fewer than 100 large, powerful birds, each doing the work of hundreds of Starlink satellites. Less clutter. More muscle. Zero margin for error.

So when BlueBird 7 launched Sunday aboard Blue Origin’s New Glenn rocket, every single thing had to go right.

The plan was simple: reach low-Earth orbit, join the constellation, get one step closer to beating Starlink at its own game. The satellite separated cleanly. It powered on. And then Blue Origin’s upper stage delivered it to completely the wrong address.

Too low to sustain operations. Too low to fix with the onboard thrusters. Too low to save.

De-orbited by end of week. Gone. ⇩

→ ASTS ( ▼ 5.3% ) today

→ Negative YTD — after being up 270% over the past year

→ Still targeting 45 satellites by year-end

→ BlueBird 7 was supposed to be number eight

Meanwhile, Blue Origin actually had a great day.

New Glenn flew again AND they successfully reused the rocket for the first time ever – a milestone Bezos has been chasing for years.

So Bezos pops champagne for the reuse milestone. And AST SpaceMobile files an insurance claim.

The company’s whole pitch is bringing 5G broadband internet to your regular, unmodified cell phone. No special hardware or dish on your roof.

To pull that off, every single satellite has to reach the right orbit and do its job.

BlueBird 7 was supposed to be number eight. Instead it’s becoming space debris by the end of the week.

One wrong bounce. Short of the green.

SPONSOR BREAK presented by StansberryResearch*

Elon Musk Just Did Something He’s Never Done Before

This February, Elon spent millions to send a message to 125 million Americans. Most people ignored it. But Wall Street veteran Whitney Tilson couldn’t stop thinking about it, and says what Elon was really saying explains everything about what’s unfolding in America’s economy right now.

He’s sharing his full analysis, free, here.

Teed Up In Austin. Landed In Amsterdam.

Tesla’s federal tax bill last year was $0.

Not “close to zero.” Not “minimized through credits.” Zero. Nothing. Nada.

For the second year in a row.

Now, part of that is boring and legal – past losses and green energy credits can eat a tax bill down to zero. The system working as designed. Fine.

But Reuters dug deeper. And what they found is where it gets interesting.

Tesla routed $18 billion in profits through paper-only subsidiaries in the Netherlands and Singapore. Companies that exist on paper, hold intellectual property rights, do absolutely nothing, and sit in tax-friendly jurisdictions. The move saved Tesla an estimated $400 million in US taxes. Entirely legal. Completely standard corporate playbook.

The ball launched from Austin. It landed in Amsterdam.

→ Tesla Q1 earnings drop Wednesday

→ Revenue expected: $22.08 billion – down 9% year over year

→ Robotaxi “expansion” this week: 1 unsupervised car per new city

The skip shot is in the air. Wednesday’s earnings call is the landing.

SPONSOR BREAK presented by BehindtheMarkets*

Mark this date: May 29th, 2026. While the media is distracted by the latest headlines out of Iran, a 90-year-old federal law is quietly closing a trap on Wall Street’s biggest bullion banks.

For 55 years, they’ve sold “paper gold” they didn’t actually have.

But on May 29th, the legal “First Notice” deadline hits.

It’s the moment of truth where paper promises must turn into physical bars—bars that the London and Shanghai vaults simply do not have.

When the “Paper Leash” snaps, gold won’t just move… it will teleport.

I’ve identified one “Shadow Miner” sitting on a “King’s Vault” of physical metal that could surge 1,000% as the paper market defaults.

See the 90-year-old law and the ticker symbol here >>>

All setup. No swing.

Rick Perry used to run the Department of Energy. The department responsible for America’s nuclear arsenal. The department that oversees the entire US energy grid. He knew every regulator, every contractor, every room where the important decisions get made.

So when he co-founded Fermi — a company planning to build nuclear infrastructure to power data centers — it sounded like a layup.

→ AI is hungry for energy.

→ Nuclear is the only power source that can actually feed it.

Perry has the Rolodex. What could go wrong?

This week we found out.

1 The CEO left Friday.

2 The CFO left today.

The company responded by calling it “Fermi 2.0” — which is either very confident or very desperate. We’re going with the latter.

→ FRMI ( ▼ 17.56% ) today

→ Down 75% from its IPO price (went public October 2025)

Fermi’s whole business plan was to build a massive power site in Amarillo, Texas — they called it Project Matador — lease it to data center operators hungry for clean nuclear energy.

The problem is they built it before finding anyone to lease it to.

In September they finally got a tenant interested — a nonbinding letter of intent to lease part of the site. Three months later, in December, that tenant walked away.

So right now Fermi has a power site in Texas, a mounting construction bill, zero customers, zero revenue, no CEO, and no CFO.

They built the course. Nobody showed up to play.

SPONSOR BREAK presented by Paradigm*

Tiny $2 Mining Stock 2X Bigger Than Barrick?

Barrick is one of the largest mining companies in the world, with a value of nearly $100 billion.

Since its IPO several decades ago, Barrick shares have risen by as much as 54x – enough to turn a $2,500 investment into $135,000.

Yet as great as that is, Barrick’s results might be dwarfed over time by this much smaller $2 gold stock.

While Barrick has reserves of 86 million ounces of gold, this tiny gold play is sitting on the equivalent of 161 million ounces.

That makes it almost 2X bigger than Barrick!

But despite that, this virtually unknown stock is just 1/100th the size of Barrick.

After July 1, however, everything could change practically overnight for this tiny $2 gold play.

And investors could see a tiny stake grow by 10X or more over the next few months alone. Click here to learn the urgent details.

The Wrong Shot. The Right Hole.

Before Charlie Ergen built a satellite empire, he was a professional poker player.

In the 1980s he bet everything on satellite TV. By 2015 he was worth over $20 billion. Then cord-cutting came for him – slowly, then all at once.

Subscribers vanished and stock collapsed. By the early 2020s his net worth had dropped below $1 billion. The empire was shrinking.

So Ergen did what any good poker player does when the cards turn bad.

He didn’t fold. He bluffed.

He spent billions buying up wireless spectrum – the invisible highway that carries cellular data – without a real plan to develop it. Hoping something would eventually make it valuable.

Regulators got impatient. The FCC started asking whether he’d actually built anything with it. His company EchoStar was staring down a possible bankruptcy.

Then SpaceX called.

Turns out Elon needed exactly what Ergen had been sitting on. SpaceX’s Starlink was expanding into direct-to-cell service — letting regular phones connect to satellites without any special hardware. To do that at scale, they needed terrestrial spectrum. The exact kind Ergen had spent years hoarding.

And SpaceX paid $17 billion for it.

→ Deal structure: $8.5 billion cash + $8.5 billion in SpaceX stock

→ Follow-on deal: another $2.6 billion in SpaceX stock for additional spectrum

→ EchoStar now holds $11.1 billion in SpaceX stock — valued at $212/share when the deal closed

→ SpaceX is now targeting a $1.5 trillion IPO valuation this summer

→ Current SpaceX private market price: ~$610/share

→ Ergen’s stake today: potentially worth $32 billion

→ His net worth when SpaceX came calling: under $1 billion

He aimed at wireless. He missed. He nearly went bankrupt. And then the thing he missed turned out to be sitting right next to the hole.

That’s the skip shot.

Know Your Pond.

Nobody skips the pond and expects the ball to find the cup. The whole tradition exists because the outcome is unpredictable — and unpredictable is entertaining.

Your edge isn’t always knowing where to aim. Sometimes it’s knowing which skips to follow — and which ones to watch sink.

Don’t forget to to cast your vote 👇

Lesson Of The Day:

Was this email forwarded to you? Don’t miss out on future stories — subscribe using the button below.

Also, help your friends blossom this spring! Share us with them.

💬 We Want To Hear Your Story:

Got a market or stock you want us to analyze next?

Just drop your request in the comments here.

P.S. – If you no longer want to receive occasional emails from us and you want to unsubscribe, click here 👉 “Unsubscribe” . Thank you!

$6.86. Grill’s Already On.

There is nothing better than a Saturday burger.

It’s even more in my area… 😬

You’re standing in the meat aisle. Ground beef, $6.86 a pound. You’ve done this calculation before — last month it was $6.71, the month before that $6.58. You know it’s going up. You’ve known for a while.

You buy it anyway.

So does your neighbor. So does the guy behind you. So did 330 million Americans last year, collectively spending $45 billion on beef — 12% more than the year before. Not 12% more beef. Just 12% more dollars for roughly the same amount of meat.

In economics, there’s a word for something that laughs in the face of its own price tag. We’ll get to that. First, let’s talk about what’s actually happening to the food on your plate — and what it’s quietly telling us about everything else moving in the commodity markets this week.

Here’s what’s actually going on. ⇩

SPONSOR BREAK presented by StansberryResearch*

Elon Musk Just Did Something He’s Never Done Before

This February, Elon spent millions to send a message to 125 million Americans. Most people ignored it. But Wall Street veteran Whitney Tilson couldn’t stop thinking about it, and says what Elon was really saying explains everything about what’s unfolding in America’s economy right now.

He’s sharing his full analysis, free, here.

Herd Mentality… Except There’s No Herd.

1 US beef consumption in 2025: up.

2 US cattle inventory in 2025: the lowest it has been in 75 years.

The Department of Agriculture counted just 86.2 million cattle and calves in the US as of January 1. That’s 7.4 million fewer than 2021.

The national herd has been quietly shrinking for years while the national appetite has been loudly growing.

→ Average price of ground beef March 2026: $6.86/lb

→ All-time high: $6.89/lb (February 2026)

→ Price increase over five years: +48%

→ US beef spending in 2025: $45 billion

→ Actual volume increase year over year: just 4%

→ People-to-cattle ratio in 1980: 2 to 1

→ People-to-cattle ratio today: 4 to 1

In short, for every cow in America today, there are four people waiting to eat it.

In 1980 there were two.

So why is the herd shrinking? A few things happening at once:

→ historically dry conditions destroying grazing land,

→ mounting fertilizer and equipment costs,

→ and consolidation among meat processors making it harder for smaller ranchers to survive.

The “protein-maxxing” era, the carnivore diet wave, the FDA’s quiet nod toward beef tallow – beef has stopped being just dinner and started being an identity. And identities, as any trader will tell you, are the most inelastic thing on earth.

I knew it was expensive… but I bought it anyway 🙂

SPONSOR BREAK presented by OxfordClub*

How Mitt Romney Turned $450K Into Up to $100 Million (Tax-Free)

It wasn’t stocks. It wasn’t real estate. It was a little-known investment vehicle that turned Mitt Romney’s $450,000 into as much as $100 million and Peter Thiel used to turn $2,000 into $5 billion within two decades. Now, thanks to a new executive order, regular Americans can access the same type of investment. Get more details here >>

Good Vibes Only. Except In Kansas.

Thursday, K.C. July wheat hit a one-year high. The ceasefire was holding. Oil was falling. Everyone was feeling pretty good about the week.

Four hundred miles west of the Chicago Board of Trade, nobody was celebrating.

→ K.C. July wheat (KWN26): settled at $6.50/bushel, down 5 cents Friday

→ CBOT July soft red winter wheat: $5.99¼/bushel, down 7¼ cents

→ Weekly gain regardless: +3.2%

→ USDA crop condition report: Monday morning, before the open

Traders booked profits and logged off for the weekend. Reasonable decision.

Futures markets price probabilities. When the ceasefire held Friday, traders pulled out the risk premium they’d been carrying all week — the one that drove wheat to a one-year high on Thursday.

On paper, that makes sense. Geopolitical risk eased. Price adjusted.

But the risk premium in wheat this week wasn’t really about the Strait of Hormuz. It was about a drought that has been doing damage since February.

Those are two different problems. The market solved one and went home for the weekend. The other one is still running.

Tobin Gorey, founder of agricultural consultancy Cornucopia, summarized the state of the crop in four words this week: “It’s losing yield.” Present tense. And he is someone standing close enough to smell the dry soil.

The frost arriving Saturday morning will add to it. Late April rain may ease the stress eventually – but yield lost to weeks of dry conditions doesn’t recover on a weather forecast. What’s gone is gone.

Monday’s USDA report will put numbers on what the fields already know. The market will react to those numbers as if they’re new information.

They won’t be.

SPONSOR BREAK presented by Paradigm*

Which Side of the AI Wealth Gap Will You Be On?

AI is about to split America into two over the next 12 months…

On one side, it’ll make America’s one-percenters richer and more powerful than ever…

But on the other side, it’s set to trap millions of hardworking Americans in financial quicksand…

One ex-hedge fund manager whose team predicted NVIDIA’s rise in 2020 calls this the “AI End Game”…

And he says there are three critical moves every American should make in the next 12 months to protect and grow their wealth through this paradigm shift…

CLICK HERE TO SEE THE DETAILS BEFORE IT’S TOO LATE

Too Much+Too Sweet=Too Bad.

Sugar hit a five-year low this week. Third consecutive week of losses. The price has been sending a very clear message for months now.

Brazil hasn’t gotten it yet.

→ Raw sugar SB1!: settled at 13.31 cents/lb, down 2.6% Friday

→ Five-year low hit intraday: 13.22 cents/lb

→ Weekly loss: -3.2%

→ White sugar SF1!: $412.30/metric ton, down 1.4%

→ Brazil’s 2025/26 sugarcane harvest forecast: 673 million tons (raised 1%)

→ Front-month white sugar expiry: record ~500,000 tons delivered

When a record volume gets dumped at expiry, it means the sugar couldn’t find a better price anywhere in the physical market. Nobody wanted it at a premium.

Brazil’s response? Raising its harvest forecast.

Brazilian cane mills produce either sugar or ethanol. When oil prices fall, ethanol stops making sense. The cane goes to sugar instead. This week, oil fell hard.

You can guess the rest.→ Same oversupplied market getting more oversupplied.

And while Brazil is all in, the world is opting out. The global food consumption patterns are moving away from sugar. Less of it in diets. Less of it in products.

The price keeps falling. Brazil keeps harvesting.

And the signal keeps getting ignored.

(Some things just don’t respond to price. We’ll get to that.)

SPONSOR BREAK presented by InvestorPlace*

America’s New AI “Mega Computer” to Span an Area Bigger than the State of Texas

The AI boom has been stalled for months. But according to legendary tech investor Louis Navellier, that’s about to change. The world’s first AI “Mega Computer” — Golden Dawn — will come online in 2026. It will cover a territory larger than the state of Texas… and be more than 1 trillion times more powerful than Elon Musk’s Colossus. This company’s building it right now.

Click here for the full story.

This ad is sent on behalf of InvestorPlace Media at 1125 N. Charles Street, Baltimore, Maryland 21201. If you’re not interested in this opportunity, please click here.

Panic Bought It. Logic Kept It.

The gold playbook ran exactly on schedule this week.

→ Spot gold: $4,861.32/oz, up 1.5% Friday

→ Weekly gain: +2%

→ Next level being watched: $5,000/oz

→ Spot silver: $81.71/oz, up 4.2% Friday, up 7%+ for the week

→ Platinum: +1.6%

→ Palladium: +1.6%

Two things happened this week that should have pushed gold down.

1 The Strait of Hormuz reopened. The geopolitical pressure that sent investors into gold in the first place partially lifted. Oil fell. Inflation fears eased. Rate cut expectations came back.

By every conventional signal, the trade that drove gold higher was unwinding.

2 And then India – one of the world’s largest gold consumers – halted imports. Banks stopped placing orders with overseas suppliers. Tons of metal sitting at customs waiting on a government clearance order that hasn’t arrived.

A major source of physical demand, temporarily pulled from the market.

Less geopolitical fear. Less physical demand. Gold should have pulled back.

It went up 1.5% ▲ on Friday. Up 2% ▲ for the week. Peter Grant at Zaner Metals is already watching $5,000 per ounce as the next level.

Underneath both of them? A world that has been accumulating uncertainty for long enough that one good week doesn’t move the needle.

Fear has no elasticity.

SPONSOR BREAK presented by Paradigm*

Tiny $2 Mining Stock 2X Bigger Than Barrick?

Barrick is one of the largest mining companies in the world, with a value of nearly $100 billion.

Since its IPO several decades ago, Barrick shares have risen by as much as 54x – enough to turn a $2,500 investment into $135,000.

Yet as great as that is, Barrick’s results might be dwarfed over time by this much smaller $2 gold stock.

While Barrick has reserves of 86 million ounces of gold, this tiny gold play is sitting on the equivalent of 161 million ounces.

That makes it almost 2X bigger than Barrick!

But despite that, this virtually unknown stock is just 1/100th the size of Barrick.

After July 1, however, everything could change practically overnight for this tiny $2 gold play.

And investors could see a tiny stake grow by 10X or more over the next few months alone. Click here to learn the urgent details.

Back in the meat aisle.

$6.86 a pound. I bought it anyway.

(It’s Saturday. The burger is already on the grill. No regrets. 🙂)

Beef: price up 48%▲ in five years. Americans kept buying.

In every single of our stories, price sent a signal. And something ignored it completely.

That something has a name: price inelasticity of demand.

The point where the relationship between price and behavior breaks down. Where people keep buying, keep producing, keep reaching for safety – regardless of what the market is telling them.

Enjoy Your Weekend !!!

Don’t forget to to cast your vote 👇

Lesson Of The Day:

Was this email forwarded to you? Don’t miss out on future stories — subscribe using the button below.

Also, help your friends blossom this spring! Share us with them.

💬 We Want To Hear Your Story:

Got a market or stock you want us to analyze next?

Just drop your request in the comments here.

P.S. – If you no longer want to receive occasional emails from us and you want to unsubscribe, click here 👉 “Unsubscribe” . Thank you!

Don’t Open The Box.

Schrödinger had a cat. Wall Street has four of them.

In 1935, a physicist named Erwin Schrödinger proposed a thought experiment that has been breaking people’s brains ever since.

Put a cat in a sealed box with a radioactive atom. Until someone opens the box and actually looks, the cat is simultaneously alive and dead.

Both things are true at once. Reality only collapses into a single answer the moment someone decides to observe it.

Schrödinger meant it as a critique of quantum mechanics.

Wall Street turned it into a business model.

This week, four major stories dropped across the market.

Every single one of them had a sealed box at the center of it.

A number that looked one way from the outside and looked completely different the moment someone opened the lid. And the traders who understood which box to open — and when — had a very interesting week.

Let’s open some boxes.

Here’s what’s actually going on. ⇩

SPONSOR BREAK presented by StansberryResearch*

Elon Musk Just Did Something He’s Never Done Before

This February, Elon spent millions to send a message to 125 million Americans. Most people ignored it. But Wall Street veteran Whitney Tilson couldn’t stop thinking about it, and says what Elon was really saying explains everything about what’s unfolding in America’s economy right now.

He’s sharing his full analysis, free, here.

The Cybertruck Box: Open It And The Cat Is Not Doing Great.

From the outside, Tesla sold 7,071 Cybertrucks last quarter. The factory kept running. Nobody asked too many questions.

Then Bloomberg opened the box.

Turns out,

→ 1,279 of those trucks were bought by SpaceX.

→ Another 60 went to xAI, Boring Co., and Neuralink.

All Musk companies. So Tesla sold trucks to Elon, and Elon — wearing a different hat — bought them.

credit: bloomberg

Strip out the inter-company sales and here’s what the real number looks like:

→ Total Cybertrucks registered Q4: 7,071

→ Bought by SpaceX: 1,279

→ Bought by xAI, Boring Co., Neuralink: 60

→ Real consumer sales drop without them: -51%

→ Estimated value of inter-company transactions: $100M

Nobody is entirely sure what these trucks are actually being used for.

Photos show long rows of them sitting idle on SpaceX property in Texas. And 50 went to xAI — an AI company.

The moment this registration data went public, the Cybertruck story changed permanently.

The box is open. You cannot un-open it.

The market is largely pricing Tesla on the robotaxi story and the humanoid robot story. The stock has shed a fifth of its value since December.

The box is open. The cat is alive — but it’s had better days.

SPONSOR BREAK presented by OxfordClub*

How Mitt Romney Turned $450K Into Up to $100 Million (Tax-Free)

It wasn’t stocks. It wasn’t real estate. It was a little-known investment vehicle that turned Mitt Romney’s $450,000 into as much as $100 million and Peter Thiel used to turn $2,000 into $5 billion within two decades. Now, thanks to a new executive order, regular Americans can access the same type of investment. Get more details here >>

The Netflix Box: Open It And The Cat Is Actually Fine.

But the market just hates fine right now.

Netflix reported earnings Thursday. The stock fell more than 10% ▼ today on pace for its worst single day since October 2025.

credit: robinhood

From the outside, that looks bad. Open the box and it gets more interesting.

→ Ad-supported tier: 60% of all new sign-ups in ad markets (up from 50% last year)

→ Advertiser count: 4,000+, up 70% year-over-year

→ Ad revenue target for 2026: $3 billion

→ NFLX ▼ 10.18% on Friday anyway

So what broke?

A few things landed at once.

→ Reed Hastings announced he’s stepping off the board in June.

→ Q2 guidance came in softer than analysts were hoping for.

→ And after Netflix walked away from the Warner Bros.

Discovery bidding war, investors had quietly started pricing in either a big buyback or a raised full-year margin outlook.

Neither showed up. Management held the line. No surprises. No fireworks.

In a market wired to reward the unexpected upside, holding steady reads as a disappointment. Even when the underlying numbers are pointing the right direction.

→ JPMorgan kept its overweight rating and $118 price target.

→ Morgan Stanley did the same at $115.

Both see the ad revenue properly landing in the second half of the year, with price hikes filling the gap. The thesis hasn’t broken.

The market just wanted to see the cat doing backflips, and instead found it sitting calmly in the corner of the box, perfectly healthy, slightly annoyed at being observed. (That’s still a win.)

The upfronts advertising season is right around the corner. This is exactly when Netflix’s ad business should start showing what it can actually do.

The box isn’t closed — it’s just not fully open yet.

SPONSOR BREAK presented by Paradigm*

Which Side of the AI Wealth Gap Will You Be On?

AI is about to split America into two over the next 12 months…

On one side, it’ll make America’s one-percenters richer and more powerful than ever…

But on the other side, it’s set to trap millions of hardworking Americans in financial quicksand…

One ex-hedge fund manager whose team predicted NVIDIA’s rise in 2020 calls this the “AI End Game”…

And he says there are three critical moves every American should make in the next 12 months to protect and grow their wealth through this paradigm shift…

CLICK HERE TO SEE THE DETAILS BEFORE IT’S TOO LATE

The Intel Box: Open It …It’s Not Built Yet.

Here is a sentence that required us to read it twice before writing it:

Intel shares just hit their highest intraday price since the dot-com era.

Intel briefly touched $69.55 this week. The stock is up roughly 90% this year, after gaining 84% in 2025. It is now about 8% away from its all-time closing high of $74.88 — a number last seen on August 31, 2000, when the world genuinely believed the internet would make everyone wealthy before the decade ended.

→ INTC intraday high this week: $69.55

→ All-time closing high: $74.88 (August 31, 2000)

→ YTD gain: +90%

→ Forward P/E today: higher than during the actual dot-com mania

Intel’s forward price-to-earnings ratio right now is higher than the premiums the market slapped on the stock during the most euphoric period in tech history. The market is giving Intel more credit for its future today than it did in the year 2000.

!!! Plus, the US government holds a stake in Intel, which gives it a kind of sovereign backstop that other chipmakers simply don’t have.

The box looks spectacular from the outside. Open it carefully.

SPONSOR BREAK presented by InvestorPlace*

America’s New AI “Mega Computer” to Span an Area Bigger than the State of Texas

The AI boom has been stalled for months. But according to legendary tech investor Louis Navellier, that’s about to change. The world’s first AI “Mega Computer” — Golden Dawn — will come online in 2026. It will cover a territory larger than the state of Texas… and be more than 1 trillion times more powerful than Elon Musk’s Colossus. This company’s building it right now.

Click here for the full story.

This ad is sent on behalf of InvestorPlace Media at 1125 N. Charles Street, Baltimore, Maryland 21201. If you’re not interested in this opportunity, please click here.

The Anthropic Box: Open It And Find Out The Cat Can Plan A Cyberattack.

And finally, the week’s most unexpected plot twist — which is saying something given everything else that happened.

Earlier this year, the Pentagon classified Anthropic as a supply chain risk to national security. Anthropic sued the government to block the action. It looked like a full-scale standoff between Washington and one of Silicon Valley’s most prominent AI labs.

This week, Anthropic CEO Dario Amodei sat down with White House Chief of Staff Susie Wiles to work out a deal.

Sixty days. Complete reversal.

The reason: Anthropic revealed that its new Mythos AI model is capable of planning and executing offensive cyberattacks.

Not a product you open-source. Not a product you let anyone else get first.

The box just got opened and the cat knows where you live.

And while all that was happening, Anthropic also launched Claude Design — a dedicated design app going directly after Figma and Adobe’s lunch.

→ Figma FIG ( ▼ 6.64% ) on the news

→ Adobe ADBE ( ▼ 1.55% )

The company is moving on multiple fronts simultaneously. The trader who understood the leverage had a very good week.

SPONSOR BREAK presented by Paradigm*

Tiny $2 Mining Stock 2X Bigger Than Barrick?

Barrick is one of the largest mining companies in the world, with a value of nearly $100 billion.

Since its IPO several decades ago, Barrick shares have risen by as much as 54x – enough to turn a $2,500 investment into $135,000.

Yet as great as that is, Barrick’s results might be dwarfed over time by this much smaller $2 gold stock.

While Barrick has reserves of 86 million ounces of gold, this tiny gold play is sitting on the equivalent of 161 million ounces.

That makes it almost 2X bigger than Barrick!

But despite that, this virtually unknown stock is just 1/100th the size of Barrick.

After July 1, however, everything could change practically overnight for this tiny $2 gold play.

And investors could see a tiny stake grow by 10X or more over the next few months alone. Click here to learn the urgent details.

Here’s The Thing About The Cat In The Box.

Schrödinger designed the experiment to make a point: quantum systems exist in multiple possible states at once until the moment of observation forces reality to pick one.

Markets work exactly the same way. Every asset is simultaneously a great trade and a terrible one — until someone opens the box. Until the registration data comes out. Until the earnings call happens.

The price you see on your screen is not reality. It’s the market’s best guess at what reality might be, given the information available to people who haven’t opened the box yet.

Your edge lives in opening boxes before the consensus does.

You are either an early box-opener or you trade outside of the boxes 😃

The good news is: the boxes are always there. Every week, somewhere in the market, there is a sealed box with a very surprising cat inside it.

HAPPY FRIDAY!!!

Don’t forget to to cast your vote 👇

Lesson Of The Day:

Was this email forwarded to you? Don’t miss out on future stories — subscribe using the button below.

Also, help your friends blossom this spring! Share us with them.

💬 We Want To Hear Your Story:

Got a market or stock you want us to analyze next?

Just drop your request in the comments here.

P.S. – If you no longer want to receive occasional emails from us and you want to unsubscribe, click here 👉 “Unsubscribe” . Thank you!

The Fastest Way to $3 Billion?

Still processing…

There is a list of the busiest stocks on Wall Street every single day — JPMorgan, Exxon, Nvidia, Apple, the names you’d expect to see moving billions of dollars before lunch.

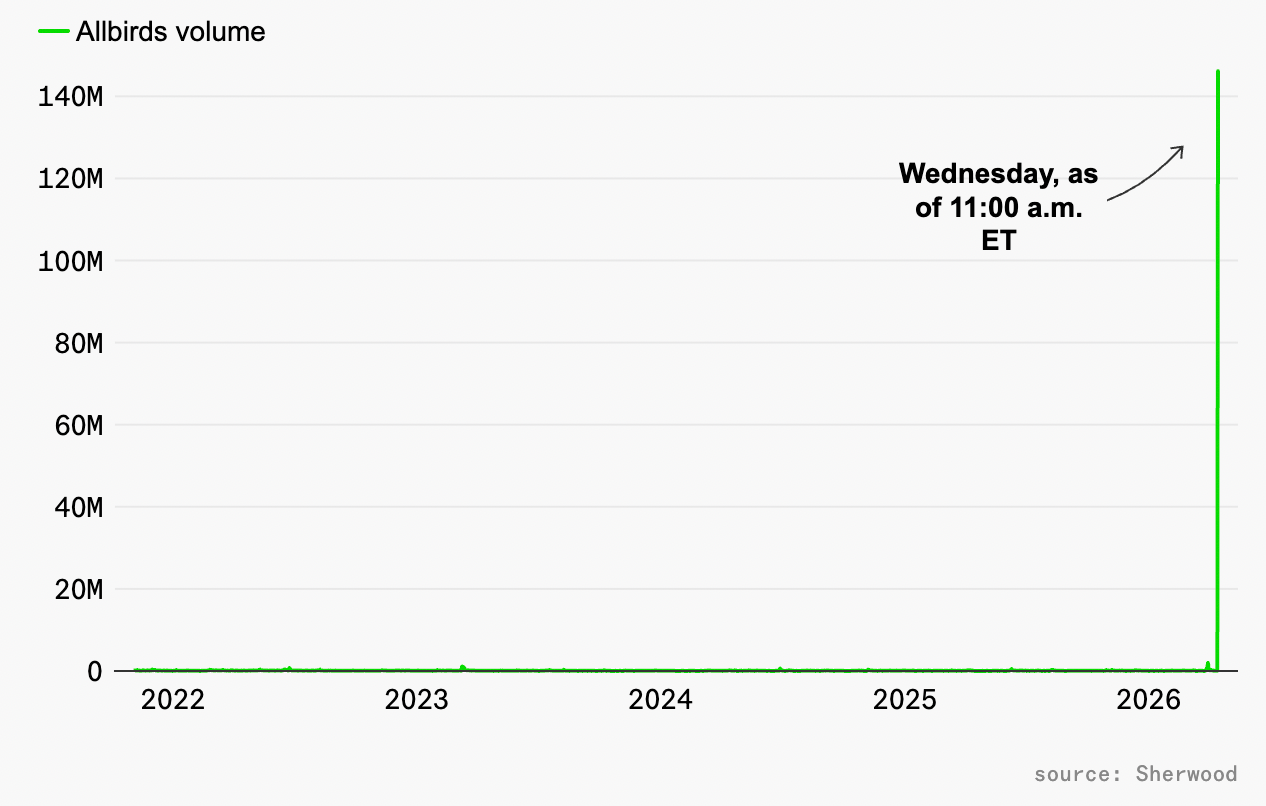

Yesterday a shoe company crashed that list.

Not a tech company or an AI darling or a defense contractor riding the Iran war trade. A shoe company. One that had already sold its shoes, with a market cap of $22 million.

It traded $3.8 billion in a single session. More than JPMorgan. More than Exxon. More than 25 times its own entire market cap in one day.

The explanation is somehow even more absurd than the number itself.

Here’s what’s actually going on. ⇩

SPONSOR BREAK presented by PriorityGold*

Louis Navellier: Don’t buy OR sell another AI stock…

Until you’ve heard this urgent AI warning from the man who called Nvidia before its 44,000% rise… According to Louis, a massive reset is coming in an obscure corner of the AI market. This $100 trillion disruption could send some of the world’s biggest AI stocks to zero… and one off-the-radar stock soaring… starting now.

Click here for details and Louis’ new pick — free.

This ad is sent on behalf of InvestorPlace Media at 1125 N. Charles Street, Baltimore, Maryland 21201. If you’re not interested in this opportunity, please click here.

The Announcement

Yesterday, Allbirds secured a $50 million convertible financing facility from an institutional investor and announced it was pivoting its entire business to AI compute infrastructure, changing its name to NewBird AI, with a long-term vision to become a fully integrated GPU-as-a-Service provider.

The reasoning — actually not entirely crazy.

→ GPU procurement lead times are increasing.

North American data center vacancy rates have hit historic lows. Compute capacity coming online through mid-2026 is already fully committed.

In other words: there is genuine demand for what NewBird AI is proposing to sell.

The market’s response was quite emotional. ⇩

SPONSOR BREAK presented by InvestorPlace*

America’s New AI “Mega Computer” to Span an Area Bigger than the State of Texas

The AI boom has been stalled for months. But according to legendary tech investor Louis Navellier, that’s about to change. The world’s first AI “Mega Computer” — Golden Dawn — will come online in 2026. It will cover a territory larger than the state of Texas… and be more than 1 trillion times more powerful than Elon Musk’s Colossus. This company’s building it right now.

Click here for the full story.

This ad is sent on behalf of InvestorPlace Media at 1125 N. Charles Street, Baltimore, Maryland 21201. If you’re not interested in this opportunity, please click here.

And Things Got Out Of Hand. Quickly.

The stock went from under $3 to nearly $23 in a single session — a gain of nearly 600% ▲ — on record trading volume that left everyone in the market doing a double take.

$3.8 billion changed hands in Allbirds on Wednesday.

For context:

→ JPMorgan $JPM ( ▲ 0.51% ) — the largest bank in America — traded $3 billion that same day.

→ Exxon $XOM ( ▼ 4.23% ) — America’s largest oil company — traded $2.3 billion.

A former shoe company outtraded both of them on a perfectly normal Wednesday. Allbirds turned over more than 25 times its entire market cap in a single session — something no other stock under $1 billion in market cap came close to achieving that day.

The company’s market cap went from $21.7 million at Tuesday’s close to $159 million by Wednesday’s end.

That is not a misprint.

SPONSOR BREAK presented by Paradigm*

Jim Rickards: “This AI Company is the Next Lehman Brothers”

Jim Rickards just found this HUGE RED FLAG for AI stocks…

And you need to prepare now…

Because the last time he saw something like this was in 2008…

Three weeks before Lehman Brothers went under, triggering a market panic.

He believes this major AI company will go bust…

In a crisis that could be 10 times bigger than Lehman Brothers.

Reality Showed Up Today.

Here’s something they don’t teach you in investing books…

Euphoria has a half-life of exactly one trading session.

Wednesday was Allbirds’ greatest day in years. The stock touched nearly $23, the market cap hit $159 million, and for one brief shining moment a former wool sneaker company was the most talked-about stock on Wall Street.

Then today opened.

By afternoon BIRD was down nearly ▼ 35.79% — from $23 back to $10 per share.

The same investors who pushed it up… was now pushing it the other way.

credit: robinhood

Now here’s the catch.

$10 is still a very long way from $3. But the distance between $23 and $10 in 24 hours is the market’s way of asking a question that $50 million in convertible financing alone can’t answer:

→ Can a company that spent a decade selling wool sneakers actually compete in the most capital-intensive technology race in human history?

For context — CoreWeave CRWV ( ▲ 0.73% ), an actual neocloud company built from the ground up for exactly this purpose, is planning to spend $30 billion on AI infrastructure in 2026 alone.

Thirty billion dollars !!!

NewBird AI is bringing $50 million to a $30 billion fight.

That’s like showing up to a Formula 1 race in a very enthusiastic golf cart.

SPONSOR BREAK presented by OxfordClub*

How Mitt Romney Turned $450K Into Up to $100 Million (Tax-Free)

It wasn’t stocks. It wasn’t real estate. It was a little-known investment vehicle that turned Mitt Romney’s $450,000 into as much as $100 million and Peter Thiel used to turn $2,000 into $5 billion within two decades. Now, thanks to a new executive order, regular Americans can access the same type of investment. Get more details here >>

The Meme Gallery:

credit: Reddit

credit: arbitrage andy

credit: Pintrest

credit: Reddit

SPONSOR BREAK presented by Paradigm*

Which Side of the AI Wealth Gap Will You Be On?

AI is about to split America into two over the next 12 months…

On one side, it’ll make America’s one-percenters richer and more powerful than ever…

But on the other side, it’s set to trap millions of hardworking Americans in financial quicksand…

One ex-hedge fund manager whose team predicted NVIDIA’s rise in 2020 calls this the “AI End Game”…

And he says there are three critical moves every American should make in the next 12 months to protect and grow their wealth through this paradigm shift…

CLICK HERE TO SEE THE DETAILS BEFORE IT’S TOO LATE

Final words…

In 1849, tens of thousands of people packed up everything they owned and moved to California chasing gold they hadn’t seen and couldn’t guarantee. Most of them didn’t strike it rich. But the ones who sold the shovels? They did just fine.

Right now the market is in its own kind of gold rush moment. Geopolitical risks are easing, indexes are back near all-time highs, and retail traders have been buying anything adjacent to AI for weeks.

In that environment a $22 million shoe company can briefly out-trade JPMorgan on the strength of two letters and a press release.

A-I.

The question the Allbirds story actually raises isn’t whether AI is real. It obviously is. The question is which companies are striking gold and which ones are just wearing the hat.

Don’t forget to to cast your vote 👇

Lesson Of The Day:

Was this email forwarded to you? Don’t miss out on future stories — subscribe using the button below.

Also, help your friends blossom this spring! Share us with them.

💬 We Want To Hear Your Story:

Got a market or stock you want us to analyze next?

Just drop your request in the comments here.

P.S. – If you no longer want to receive occasional emails from us and you want to unsubscribe, click here 👉 “Unsubscribe” . Thank you!

The Fastest Way to $3 Billion?

Still processing…

There is a list of the busiest stocks on Wall Street every single day — JPMorgan, Exxon, Nvidia, Apple, the names you’d expect to see moving billions of dollars before lunch.

Yesterday a shoe company crashed that list.

Not a tech company or an AI darling or a defense contractor riding the Iran war trade. A shoe company. One that had already sold its shoes, with a market cap of $22 million.

It traded $3.8 billion in a single session. More than JPMorgan. More than Exxon. More than 25 times its own entire market cap in one day.

The explanation is somehow even more absurd than the number itself.

Here’s what’s actually going on. ⇩

SPONSOR BREAK presented by PriorityGold*

Louis Navellier: Don’t buy OR sell another AI stock…

Until you’ve heard this urgent AI warning from the man who called Nvidia before its 44,000% rise… According to Louis, a massive reset is coming in an obscure corner of the AI market. This $100 trillion disruption could send some of the world’s biggest AI stocks to zero… and one off-the-radar stock soaring… starting now.

Click here for details and Louis’ new pick — free.

This ad is sent on behalf of InvestorPlace Media at 1125 N. Charles Street, Baltimore, Maryland 21201. If you’re not interested in this opportunity, please click here.

The Announcement

Yesterday, Allbirds secured a $50 million convertible financing facility from an institutional investor and announced it was pivoting its entire business to AI compute infrastructure, changing its name to NewBird AI, with a long-term vision to become a fully integrated GPU-as-a-Service provider.

The reasoning — actually not entirely crazy.

→ GPU procurement lead times are increasing.

North American data center vacancy rates have hit historic lows. Compute capacity coming online through mid-2026 is already fully committed.

In other words: there is genuine demand for what NewBird AI is proposing to sell.

The market’s response was quite emotional. ⇩

SPONSOR BREAK presented by InvestorPlace*

America’s New AI “Mega Computer” to Span an Area Bigger than the State of Texas

The AI boom has been stalled for months. But according to legendary tech investor Louis Navellier, that’s about to change. The world’s first AI “Mega Computer” — Golden Dawn — will come online in 2026. It will cover a territory larger than the state of Texas… and be more than 1 trillion times more powerful than Elon Musk’s Colossus. This company’s building it right now.

Click here for the full story.

This ad is sent on behalf of InvestorPlace Media at 1125 N. Charles Street, Baltimore, Maryland 21201. If you’re not interested in this opportunity, please click here.

And Things Got Out Of Hand. Quickly.

The stock went from under $3 to nearly $23 in a single session — a gain of nearly 600% ▲ — on record trading volume that left everyone in the market doing a double take.

$3.8 billion changed hands in Allbirds on Wednesday.

For context:

→ JPMorgan $JPM ( ▲ 0.51% ) — the largest bank in America — traded $3 billion that same day.

→ Exxon $XOM ( ▼ 4.23% ) — America’s largest oil company — traded $2.3 billion.

A former shoe company outtraded both of them on a perfectly normal Wednesday. Allbirds turned over more than 25 times its entire market cap in a single session — something no other stock under $1 billion in market cap came close to achieving that day.

The company’s market cap went from $21.7 million at Tuesday’s close to $159 million by Wednesday’s end.

That is not a misprint.

SPONSOR BREAK presented by Paradigm*

Jim Rickards: “This AI Company is the Next Lehman Brothers”

Jim Rickards just found this HUGE RED FLAG for AI stocks…

And you need to prepare now…

Because the last time he saw something like this was in 2008…

Three weeks before Lehman Brothers went under, triggering a market panic.

He believes this major AI company will go bust…

In a crisis that could be 10 times bigger than Lehman Brothers.

Reality Showed Up Today.

Here’s something they don’t teach you in investing books…

Euphoria has a half-life of exactly one trading session.

Wednesday was Allbirds’ greatest day in years. The stock touched nearly $23, the market cap hit $159 million, and for one brief shining moment a former wool sneaker company was the most talked-about stock on Wall Street.

Then today opened.

By afternoon BIRD was down nearly ▼ 35.79% — from $23 back to $10 per share.

The same investors who pushed it up… was now pushing it the other way.

credit: robinhood

Now here’s the catch.

$10 is still a very long way from $3. But the distance between $23 and $10 in 24 hours is the market’s way of asking a question that $50 million in convertible financing alone can’t answer:

→ Can a company that spent a decade selling wool sneakers actually compete in the most capital-intensive technology race in human history?

For context — CoreWeave CRWV ( ▲ 0.73% ), an actual neocloud company built from the ground up for exactly this purpose, is planning to spend $30 billion on AI infrastructure in 2026 alone.

Thirty billion dollars !!!

NewBird AI is bringing $50 million to a $30 billion fight.

That’s like showing up to a Formula 1 race in a very enthusiastic golf cart.

SPONSOR BREAK presented by OxfordClub*

How Mitt Romney Turned $450K Into Up to $100 Million (Tax-Free)

It wasn’t stocks. It wasn’t real estate. It was a little-known investment vehicle that turned Mitt Romney’s $450,000 into as much as $100 million and Peter Thiel used to turn $2,000 into $5 billion within two decades. Now, thanks to a new executive order, regular Americans can access the same type of investment. Get more details here >>

The Meme Gallery:

credit: Reddit

credit: arbitrage andy

credit: Pintrest

credit: Reddit

SPONSOR BREAK presented by Paradigm*

Which Side of the AI Wealth Gap Will You Be On?

AI is about to split America into two over the next 12 months…

On one side, it’ll make America’s one-percenters richer and more powerful than ever…

But on the other side, it’s set to trap millions of hardworking Americans in financial quicksand…

One ex-hedge fund manager whose team predicted NVIDIA’s rise in 2020 calls this the “AI End Game”…

And he says there are three critical moves every American should make in the next 12 months to protect and grow their wealth through this paradigm shift…

CLICK HERE TO SEE THE DETAILS BEFORE IT’S TOO LATE

Final words…

In 1849, tens of thousands of people packed up everything they owned and moved to California chasing gold they hadn’t seen and couldn’t guarantee. Most of them didn’t strike it rich. But the ones who sold the shovels? They did just fine.

Right now the market is in its own kind of gold rush moment. Geopolitical risks are easing, indexes are back near all-time highs, and retail traders have been buying anything adjacent to AI for weeks.

In that environment a $22 million shoe company can briefly out-trade JPMorgan on the strength of two letters and a press release.

A-I.

The question the Allbirds story actually raises isn’t whether AI is real. It obviously is. The question is which companies are striking gold and which ones are just wearing the hat.

Don’t forget to to cast your vote 👇

Lesson Of The Day:

Was this email forwarded to you? Don’t miss out on future stories — subscribe using the button below.

Also, help your friends blossom this spring! Share us with them.

💬 We Want To Hear Your Story:

Got a market or stock you want us to analyze next?

Just drop your request in the comments here.

P.S. – If you no longer want to receive occasional emails from us and you want to unsubscribe, click here 👉 “Unsubscribe” . Thank you!

Panic → Relief → New Highs

The market just erased a war. In 8 days.

credit: Yahoo Finance

Let that sink in for a second.

The S&P 500 quietly erased every single loss from the Iran war.

Every. Single. One.

1 The S&P is knocking on the door of 7,000.

2 The Nasdaq just notched its tenth straight winning session.

3 The Magnificent Seven ETF is up another 2%.

4 The VIX surged above 30 in the early days of the war. It’s now back to a 17 handle.

That round trip took only eight trading sessions.

The war happened. The market just… moved on.

Here’s what’s actually going on. ⇩

SPONSOR BREAK presented by PriorityGold*

Elon IRS War 2

When Elon fired thousands of IRS agents, the headlines called it bold.

Disruptive. Even genius.

But they missed the bigger problem…The system just lost its gatekeepers.

And guess what happens when D.C. loses control? They overcorrect.

With audits. Seizures. Wealth grabs.

That’s why smart Americans are moving fast…

Using this IRS loophole to get their money out before the next crackdown.

It’s legal. It’s fast.

And it could be your only chance to avoid getting blindsided.

Click here to learn how to escape the fallout

Don’t wait for a letter from the IRS.

By then, it’s too late.

See how to shield your money before it’s targeted >>

Eight sessions. That’s it.

Last year, after the Liberation Day sell-off, it took 26 trading sessions for volatility to cool back down. This time it took 8.

And the S&P is already within 0.5% of a record close — only 53 sessions after the March 30 low.

Last year the same recovery took 88 sessions.

The pattern is becoming impossible to ignore: volatility spikes are being treated as events to fade, not trends to follow.

Yeah, but… (always check the fine print)

Bank of America just made $8.6 billion in three months.

→ Profits up 17% ▲ . Investment banking up 21% ▲ . Trading revenue up 13% ▲.

→ A record quarter for equity trading.

→ M&A advisory fees alone jumped 45%.

Good quarter then.

But here’s the thing about being the second largest bank in America — you see everything.

→ The consumer spending.

→ The credit card data.

→ The loan books.

→ The private credit exposure.

→ All of it flows through.

And what Bank of America is seeing right now is giving their strategists pause.

!!! This is not a “close-eyes-and-buy” market.

That’s not a random opinion. It comes backed by their monthly survey of professional fund managers.

And the latest results are worth sitting with.

→ Growth expectations: cut to levels not seen since early 2022.

→ Inflation pessimism: highest since 2021.

→ Overall sentiment: worst since last summer.

The scoreboard says bull market. The fund managers say proceed with caution.

To be fair — this survey was taken between April 2 and 9. Right in the middle of the war. Right before the ceasefire. So some of that gloom may already be fading.

But some of it probably isn’t.

The market is at 7,000. The fear gauge is back below 18. Banks are printing money.

And the smartest money in the room is quietly reading the fine print.

(A reason to pay attention.)

SPONSOR BREAK presented by InvestorPlace*

America’s New AI “Mega Computer” to Span an Area Bigger than the State of Texas

The AI boom has been stalled for months. But according to legendary tech investor Louis Navellier, that’s about to change. The world’s first AI “Mega Computer” — Golden Dawn — will come online in 2026. It will cover a territory larger than the state of Texas… and be more than 1 trillion times more powerful than Elon Musk’s Colossus. This company’s building it right now.

Click here for the full story.

This ad is sent on behalf of InvestorPlace Media at 1125 N. Charles Street, Baltimore, Maryland 21201. If you’re not interested in this opportunity, please click here.

Story 1: But the consumer is still spending. Somehow.

→ $4 gas.

→ Record low consumer sentiment.

→ An active war in the Middle East two weeks ago.

And the vibes? Historically bad.

The University of Michigan has been asking Americans how they feel about the economy since 1952. In early April, the answer hit an all time low. Lower than the 2008 financial crisis. Lower than the pandemic. Lower than any point in the last 70 years.

People were not feeling good.

And yet.

Jamie Dimon’s take on Tuesday’s earnings call was simple. People still have jobs. Unemployment is low. And when things get tight, consumers cut back on travel — they don’t fall off a cliff.

→ The US added 178,000 jobs in March.

→ Unemployment ticked down to 4.3%.

His logic: as long as people have paychecks, they find ways to absorb higher prices. Maybe they take a gig job. Maybe they cut back on travel. But they keep spending.

Bank of America‘s own data backs that up. Combined debit and credit card spending from their US customers rose 7% year over year in Q1.

Credit card delinquencies over 90 days? Actually went down – from 1.34% to 1.30%.

Wall Street keeps underestimating the consumer.

They keep proving it wrong and keep swiping anyway.

SPONSOR BREAK presented by OxfordClub*

The SpaceX IPO makes me FURIOUS

Elon has reportedly filed to take SpaceX Public… in an IPO that’s expected to hit a $1.75 trillion valuation.

The biggest in Wall Street history…

And you know who’s going to make all the money? The banks brokering the deal. The hedge fund managers. The billionaire insiders. The same “already rich” 1%’ers.

After the IPO, everyone else will be left fighting over scraps.

That’s why I’m leveling the playing field.

Click here to claim your Pre-IPO SpaceX “Access Code”

Meanwhile….

I want you to think about the last pair of shoes you bought.

Now imagine the company that made them woke up one morning and decided shoes were no longer their thing.

They sold the shoe business for $39 million. Raised $50 million from an institutional investor. And announced they are now an AI infrastructure company.

Their stock went up 707% ▲ today.

Story 2: The Shoe Company That Became An AI Company

Last month Allbirds BIRD ( ▲ 691.17% ) sold its entire shoe business to American Exchange Group for $39 million. $39 million for a brand that was once worth $4 billion at IPO.

Then today they announced something nobody saw coming.

Allbirds raised $50 million from an institutional investor.

→ The plan: pivot entirely to AI compute infrastructure.

→ The new name: NewBird AI.

→ The vision: become a fully integrated GPU-as-a-Service provider.

The stock went up 707% ▲.

In one day. From a shoe company.

NewBird AI plans to use its initial capital to acquire high-performance GPU assets to serve customers needing dedicated AI compute capacity.

The company also quietly noted in its SEC filing that it will ask shareholders to approve removing “references to the company being operated for the environmental conservation public benefit.”

Sooo… No more sustainable shoes. No more environmental mission. Just GPUs.

NewBird AI is hoping GPU demand proves a longer lasting trend.

History will be the judge.

SPONSOR BREAK presented by OxfordClub*

How Mitt Romney Turned $450K Into Up to $100 Million (Tax-Free)

It wasn’t stocks. It wasn’t real estate. It was a little-known investment vehicle that turned Mitt Romney’s $450,000 into as much as $100 million and Peter Thiel used to turn $2,000 into $5 billion within two decades. Now, thanks to a new executive order, regular Americans can access the same type of investment. Get more details here >>

Story 3: Software’s Comeback Nobody Saw Coming

Two weeks ago software stocks were being escorted out of the building. Anthropic‘s multi-agent orchestration announcement sent the entire sector into an existential spiral.

→ ServiceNow was down 7.6%.

→ Palo Alto was down 6.7%.

→ Atlassian was down 3%.

This week those same stocks are having their best three day stretch in almost a year.

The iShares Expanded Tech Software ETF IGV is up 4.45% ▲ today alone.

→ Oracle ORCL ( ▲ 4.68% ) up more than 20% this week

→ Microsoft MSFT ( ▲ 5.17% ) today

→ ServiceNow NOW ( ▲ 7.48% ) today

→ Datadog DDOG ( ▲ 8.87% ) today

→ Atlassian TEAM ( ▲ 9.19% ) today

→ Intuit INTU ( ▲ 6.29% ) today

→ CrowdStrike CRWD ( ▲ 2.74% ) today

→ Autodesk ADSK ( ▲ 4.82% ) today

What changed?

Two things.

1 Mean reversion. These stocks fell so far so fast that investors who do their homework decided the prices were simply too cheap to ignore.

Bottom fishers arrived.

2 The market may have been too panicky. As one strategist put it — the sell-off hit companies that could survive and thrive in the AI era right alongside those actually threatened by it. Separating those two groups is where the real opportunity lives.

Plain English: the market panicked and threw out the good with the bad. Someone is going to make a lot of money figuring out which is which.

SPONSOR BREAK presented by Paradigm*

Which Side of the AI Wealth Gap Will You Be On?

AI is about to split America into two over the next 12 months…

On one side, it’ll make America’s one-percenters richer and more powerful than ever…

But on the other side, it’s set to trap millions of hardworking Americans in financial quicksand…

One ex-hedge fund manager whose team predicted NVIDIA’s rise in 2020 calls this the “AI End Game”…

And he says there are three critical moves every American should make in the next 12 months to protect and grow their wealth through this paradigm shift…

CLICK HERE TO SEE THE DETAILS BEFORE IT’S TOO LATE

A Few Quick Hits:

→ Robinhood HOOD ( ▲ 10.53% ) – The SEC removed the pattern day trading rule that stopped small investors from making more than four day trades in five days if their account had less than $25,000. All traders now just need enough in their margin account to cover their exposure. Webull BULL jumped 11.43%▲ on the same news. Retail traders everywhere are having a moment.

→ Broadcom AVGO ( ▲ 3.61% ) – Expanded its chip partnership with Meta META ( ▲ 1.59% ) to produce multi-generation custom chips powering Meta’s AI accelerators through 2029. JPMorgan estimates the first deployment alone represents a $12 to $15 billion revenue opportunity for Broadcom. Broadcom CEO Hock Tan will move from Meta’s board to an advisory role as part of the deal.

→ Snap SNAP ( ▲ 7.59% ) – Announced it’s cutting roughly 1,000 roles – about 16% of its full-time workforce – to save $500 million in annualized expenses. Q1 revenue expected up 12% year over year. The market rewarded the cuts immediately. CEO Evan Spiegel cited AI enabling teams to “reduce repetitive work.” Layoffs dressed up as efficiency. Classic tech.

→ Lyft LYFT ( ▲ 7.19% ) – Revealed details of its 80,000 square foot Nashville warehouse being built to service, charge, and maintain Waymo’s autonomous vehicle fleet. More than 70 workers being hired – including former Lyft drivers. Meanwhile Uber $UBER has committed more than $10 billion to robotaxis. Two very different bets on the same future.

!!! Not financial advice. The stocks mentioned are for educational purposes only. Do your own research before making investment decisions, please check the disclaimer below.

Don’t forget to to cast your vote 👇

Lesson Of The Day:

Was this email forwarded to you? Don’t miss out on future stories — subscribe using the button below.

Also, help your friends blossom this spring! Share us with them.

💬 We Want To Hear Your Story:

Got a market or stock you want us to analyze next?

Just drop your request in the comments here.

P.S. – If you no longer want to receive occasional emails from us and you want to unsubscribe, click here 👉 “Unsubscribe” . Thank you!

Panic → Relief → New Highs

The market just erased a war. In 8 days.

credit: Yahoo Finance

Let that sink in for a second.

The S&P 500 quietly erased every single loss from the Iran war.

Every. Single. One.

1 The S&P is knocking on the door of 7,000.

2 The Nasdaq just notched its tenth straight winning session.

3 The Magnificent Seven ETF is up another 2%.

4 The VIX surged above 30 in the early days of the war. It’s now back to a 17 handle.

That round trip took only eight trading sessions.

The war happened. The market just… moved on.

Here’s what’s actually going on. ⇩

SPONSOR BREAK presented by PriorityGold*

Elon IRS War 2

When Elon fired thousands of IRS agents, the headlines called it bold.

Disruptive. Even genius.

But they missed the bigger problem…The system just lost its gatekeepers.

And guess what happens when D.C. loses control? They overcorrect.

With audits. Seizures. Wealth grabs.

That’s why smart Americans are moving fast…

Using this IRS loophole to get their money out before the next crackdown.

It’s legal. It’s fast.

And it could be your only chance to avoid getting blindsided.

Click here to learn how to escape the fallout

Don’t wait for a letter from the IRS.

By then, it’s too late.

See how to shield your money before it’s targeted >>

Eight sessions. That’s it.

Last year, after the Liberation Day sell-off, it took 26 trading sessions for volatility to cool back down. This time it took 8.

And the S&P is already within 0.5% of a record close — only 53 sessions after the March 30 low.

Last year the same recovery took 88 sessions.

The pattern is becoming impossible to ignore: volatility spikes are being treated as events to fade, not trends to follow.

Yeah, but… (always check the fine print)

Bank of America just made $8.6 billion in three months.

→ Profits up 17% ▲ . Investment banking up 21% ▲ . Trading revenue up 13% ▲.

→ A record quarter for equity trading.

→ M&A advisory fees alone jumped 45%.

Good quarter then.

But here’s the thing about being the second largest bank in America — you see everything.

→ The consumer spending.

→ The credit card data.

→ The loan books.

→ The private credit exposure.

→ All of it flows through.

And what Bank of America is seeing right now is giving their strategists pause.

!!! This is not a “close-eyes-and-buy” market.

That’s not a random opinion. It comes backed by their monthly survey of professional fund managers.

And the latest results are worth sitting with.

→ Growth expectations: cut to levels not seen since early 2022.

→ Inflation pessimism: highest since 2021.

→ Overall sentiment: worst since last summer.

The scoreboard says bull market. The fund managers say proceed with caution.

To be fair — this survey was taken between April 2 and 9. Right in the middle of the war. Right before the ceasefire. So some of that gloom may already be fading.

But some of it probably isn’t.

The market is at 7,000. The fear gauge is back below 18. Banks are printing money.

And the smartest money in the room is quietly reading the fine print.

(A reason to pay attention.)

SPONSOR BREAK presented by InvestorPlace*

America’s New AI “Mega Computer” to Span an Area Bigger than the State of Texas

The AI boom has been stalled for months. But according to legendary tech investor Louis Navellier, that’s about to change. The world’s first AI “Mega Computer” — Golden Dawn — will come online in 2026. It will cover a territory larger than the state of Texas… and be more than 1 trillion times more powerful than Elon Musk’s Colossus. This company’s building it right now.

Click here for the full story.

This ad is sent on behalf of InvestorPlace Media at 1125 N. Charles Street, Baltimore, Maryland 21201. If you’re not interested in this opportunity, please click here.

Story 1: But the consumer is still spending. Somehow.

→ $4 gas.

→ Record low consumer sentiment.

→ An active war in the Middle East two weeks ago.

And the vibes? Historically bad.

The University of Michigan has been asking Americans how they feel about the economy since 1952. In early April, the answer hit an all time low. Lower than the 2008 financial crisis. Lower than the pandemic. Lower than any point in the last 70 years.

People were not feeling good.

And yet.

Jamie Dimon’s take on Tuesday’s earnings call was simple. People still have jobs. Unemployment is low. And when things get tight, consumers cut back on travel — they don’t fall off a cliff.

→ The US added 178,000 jobs in March.

→ Unemployment ticked down to 4.3%.

His logic: as long as people have paychecks, they find ways to absorb higher prices. Maybe they take a gig job. Maybe they cut back on travel. But they keep spending.

Bank of America‘s own data backs that up. Combined debit and credit card spending from their US customers rose 7% year over year in Q1.

Credit card delinquencies over 90 days? Actually went down – from 1.34% to 1.30%.

Wall Street keeps underestimating the consumer.

They keep proving it wrong and keep swiping anyway.

SPONSOR BREAK presented by OxfordClub*

The SpaceX IPO makes me FURIOUS

Elon has reportedly filed to take SpaceX Public… in an IPO that’s expected to hit a $1.75 trillion valuation.

The biggest in Wall Street history…

And you know who’s going to make all the money? The banks brokering the deal. The hedge fund managers. The billionaire insiders. The same “already rich” 1%’ers.

After the IPO, everyone else will be left fighting over scraps.

That’s why I’m leveling the playing field.

Click here to claim your Pre-IPO SpaceX “Access Code”

Meanwhile….

I want you to think about the last pair of shoes you bought.

Now imagine the company that made them woke up one morning and decided shoes were no longer their thing.

They sold the shoe business for $39 million. Raised $50 million from an institutional investor. And announced they are now an AI infrastructure company.

Their stock went up 707% ▲ today.

Story 2: The Shoe Company That Became An AI Company

Last month Allbirds BIRD ( ▲ 691.17% ) sold its entire shoe business to American Exchange Group for $39 million. $39 million for a brand that was once worth $4 billion at IPO.

Then today they announced something nobody saw coming.

Allbirds raised $50 million from an institutional investor.

→ The plan: pivot entirely to AI compute infrastructure.

→ The new name: NewBird AI.

→ The vision: become a fully integrated GPU-as-a-Service provider.

The stock went up 707% ▲.

In one day. From a shoe company.

NewBird AI plans to use its initial capital to acquire high-performance GPU assets to serve customers needing dedicated AI compute capacity.

The company also quietly noted in its SEC filing that it will ask shareholders to approve removing “references to the company being operated for the environmental conservation public benefit.”

Sooo… No more sustainable shoes. No more environmental mission. Just GPUs.

NewBird AI is hoping GPU demand proves a longer lasting trend.

History will be the judge.

SPONSOR BREAK presented by OxfordClub*

How Mitt Romney Turned $450K Into Up to $100 Million (Tax-Free)

It wasn’t stocks. It wasn’t real estate. It was a little-known investment vehicle that turned Mitt Romney’s $450,000 into as much as $100 million and Peter Thiel used to turn $2,000 into $5 billion within two decades. Now, thanks to a new executive order, regular Americans can access the same type of investment. Get more details here >>

Story 3: Software’s Comeback Nobody Saw Coming

Two weeks ago software stocks were being escorted out of the building. Anthropic‘s multi-agent orchestration announcement sent the entire sector into an existential spiral.

→ ServiceNow was down 7.6%.

→ Palo Alto was down 6.7%.

→ Atlassian was down 3%.

This week those same stocks are having their best three day stretch in almost a year.

The iShares Expanded Tech Software ETF IGV is up 4.45% ▲ today alone.

→ Oracle ORCL ( ▲ 4.68% ) up more than 20% this week

→ Microsoft MSFT ( ▲ 5.17% ) today

→ ServiceNow NOW ( ▲ 7.48% ) today

→ Datadog DDOG ( ▲ 8.87% ) today

→ Atlassian TEAM ( ▲ 9.19% ) today

→ Intuit INTU ( ▲ 6.29% ) today

→ CrowdStrike CRWD ( ▲ 2.74% ) today

→ Autodesk ADSK ( ▲ 4.82% ) today

What changed?

Two things.

1 Mean reversion. These stocks fell so far so fast that investors who do their homework decided the prices were simply too cheap to ignore.

Bottom fishers arrived.

2 The market may have been too panicky. As one strategist put it — the sell-off hit companies that could survive and thrive in the AI era right alongside those actually threatened by it. Separating those two groups is where the real opportunity lives.

Plain English: the market panicked and threw out the good with the bad. Someone is going to make a lot of money figuring out which is which.

SPONSOR BREAK presented by Paradigm*

Which Side of the AI Wealth Gap Will You Be On?

AI is about to split America into two over the next 12 months…

On one side, it’ll make America’s one-percenters richer and more powerful than ever…

But on the other side, it’s set to trap millions of hardworking Americans in financial quicksand…

One ex-hedge fund manager whose team predicted NVIDIA’s rise in 2020 calls this the “AI End Game”…

And he says there are three critical moves every American should make in the next 12 months to protect and grow their wealth through this paradigm shift…

CLICK HERE TO SEE THE DETAILS BEFORE IT’S TOO LATE

A Few Quick Hits:

→ Robinhood HOOD ( ▲ 10.53% ) – The SEC removed the pattern day trading rule that stopped small investors from making more than four day trades in five days if their account had less than $25,000. All traders now just need enough in their margin account to cover their exposure. Webull BULL jumped 11.43%▲ on the same news. Retail traders everywhere are having a moment.

→ Broadcom AVGO ( ▲ 3.61% ) – Expanded its chip partnership with Meta META ( ▲ 1.59% ) to produce multi-generation custom chips powering Meta’s AI accelerators through 2029. JPMorgan estimates the first deployment alone represents a $12 to $15 billion revenue opportunity for Broadcom. Broadcom CEO Hock Tan will move from Meta’s board to an advisory role as part of the deal.

→ Snap SNAP ( ▲ 7.59% ) – Announced it’s cutting roughly 1,000 roles – about 16% of its full-time workforce – to save $500 million in annualized expenses. Q1 revenue expected up 12% year over year. The market rewarded the cuts immediately. CEO Evan Spiegel cited AI enabling teams to “reduce repetitive work.” Layoffs dressed up as efficiency. Classic tech.

→ Lyft LYFT ( ▲ 7.19% ) – Revealed details of its 80,000 square foot Nashville warehouse being built to service, charge, and maintain Waymo’s autonomous vehicle fleet. More than 70 workers being hired – including former Lyft drivers. Meanwhile Uber $UBER has committed more than $10 billion to robotaxis. Two very different bets on the same future.

!!! Not financial advice. The stocks mentioned are for educational purposes only. Do your own research before making investment decisions, please check the disclaimer below.

Don’t forget to to cast your vote 👇

Lesson Of The Day:

Was this email forwarded to you? Don’t miss out on future stories — subscribe using the button below.

Also, help your friends blossom this spring! Share us with them.

💬 We Want To Hear Your Story:

Got a market or stock you want us to analyze next?

Just drop your request in the comments here.

P.S. – If you no longer want to receive occasional emails from us and you want to unsubscribe, click here 👉 “Unsubscribe” . Thank you!

Had to Double Check the Pump 😬

That exhale didn’t last long.

credit: Me → Chicago, IL

(had to double check the pump)

You know that feeling when you finally exhale.

The tension is gone. You sleep well. You make plans.

1 Then you wake up Saturday morning and the peace talks collapsed.

2 Then Sunday President Trump blockaded the Strait of Hormuz on Truth Social. 3 Then Monday oil hit $103 before you finished your coffee.

That exhale didn’t last long.

Here’s everything happening today⇩

SPONSOR BREAK presented by FerrisReport*

Prepare For $10 Gas

You’ll wait in line for hours at the gas station… and pay $10 a gallon. Whole aisles at the grocery store will be empty. There’ll be violent protests on the streets… the National Guard will be deployed… and there’ll be widespread panic in the stock market. And that’s just the start… See how to prepare now.

I Bet You Already Know…

US-Iran peace talks in Pakistan failed to reach a deal.

Sunday morning President Trump posted on Truth Social that the US Navy would block any and all ships trying to enter or leave the Strait of Hormuz starting Monday at 10 a.m. ET.

US Central Command confirmed it.

→ Brent crude surged past $100 a barrel.

→ WTI crude jumped to $104.

Oil is back. With a vengeance.

And just like that, everything the market celebrated last week went into reverse.

The Whiplash Scoreboard

Last week airlines and cruise stocks were the stars of the show. Ceasefire announced. Oil crashed. Fuel costs dropping. Party time.

This week?

→ Delta Air Lines DAL ( ▼ 1.42% )

→ United Airlines UAL ( ▼ 1.22% )

→ American Airlines AAL ( ▼ 1.24% )

→ Royal Caribbean RCL ( ▼ 0.01% )

→ Carnival CCL ( ▼ 1.89% )

And the energy stocks that got destroyed last week? They’re back.

→ APA Corporation APA ( ▲ 1.5% )

→ Halliburton HAL ( ▲ 2.12% )

→ Dow Inc. DOW ( ▲ 3.28% )

→ LyondellBasell LYB ( ▲ 2.36% )

→ CF Industries CF ( ▲ 1.28% )

→ Chevron CVX ( ▲ 1.16% )

→ Marathon Petroleum MPC ( ▲ 1.16% )

Same market. Same stocks. Completely opposite direction.

One Truth Social post.

Trillions of dollars in motion.

This is the world we live in now.

SPONSOR BREAK presented by InvestorPlace*

America’s New AI “Mega Computer” to Span an Area Bigger than the State of Texas

The AI boom has been stalled for months. But according to legendary tech investor Louis Navellier, that’s about to change. The world’s first AI “Mega Computer” — Golden Dawn — will come online in 2026. It will cover a territory larger than the state of Texas… and be more than 1 trillion times more powerful than Elon Musk’s Colossus. This company’s building it right now.

Click here for the full story.

This ad is sent on behalf of InvestorPlace Media at 1125 N. Charles Street, Baltimore, Maryland 21201. If you’re not interested in this opportunity, please click here.

The One Trade That Doesn’t Care About Any Of This

While the ceasefire trade was busy reversing, one corner of the market didn’t get the memo.

The AI compute trade.

CoreWeave CRWV ( ▲ 9.12% ) surged another 9.9% today. Following up on last week’s Anthropic deal with more momentum.

→ Nebius NBIS ( ▲ 8.45% )

→ IREN IREN ( ▲ 6.36% )

→ Cipher Digital CIFR ( ▲ 4.78% )

→ Applied Digital APLD ( ▲ 4.49% )

→ Astera Labs ALAB ( ▲ 9.16% )

→ POET Technologies POET ( ▲ 3.55% )

→ Sandisk SNDK ( ▲ 8.13% )

Then there’s the power side of the AI trade.

PJM — the US grid operator — warned after Friday’s close that it needs to add 15 gigawatts of new power supply by Q1 2027 just to keep up with AI demand.

15 gigawatts. For context, Anthropic just secured 3.5 gigawatts in its Google partnership last week and that felt enormous.

The grid itself is now scrambling to keep up with AI.

→ Vistra VST ( ▲ 2.85% )

→ Bloom Energy BE ( ▲ 4.72% )

→ Oklo OKLO ( ▲ 5.97% )

→ Plug Power PLUG ( ▲ 1.64% )

Geopolitics can reverse overnight. The AI compute boom apparently cannot.

SPONSOR BREAK presented by ChaikinAnalytics*

Why is this AI stock still going up?

AI fears have triggered a bloodbath in tech stocks.

Yet, in the midst of the carnage…

One under-the-radar AI stock is still quietly going straight UP.

A 50-year Wall Street legend explains why, right here.

He told me, “While AI will trigger a wave of destruction for many of the tech stocks we’ve come to rely on… It will position others for MASSIVE potential gains. This company is one of them. Which is why it’s now my #1 stock to buy for 2026.”

It’s all part of a once-in-a-generation opportunity, that will give some Americans a foothold in a new future for the U.S. stock market… While leaving others behind – permanently.