CATEGORY

Getting started

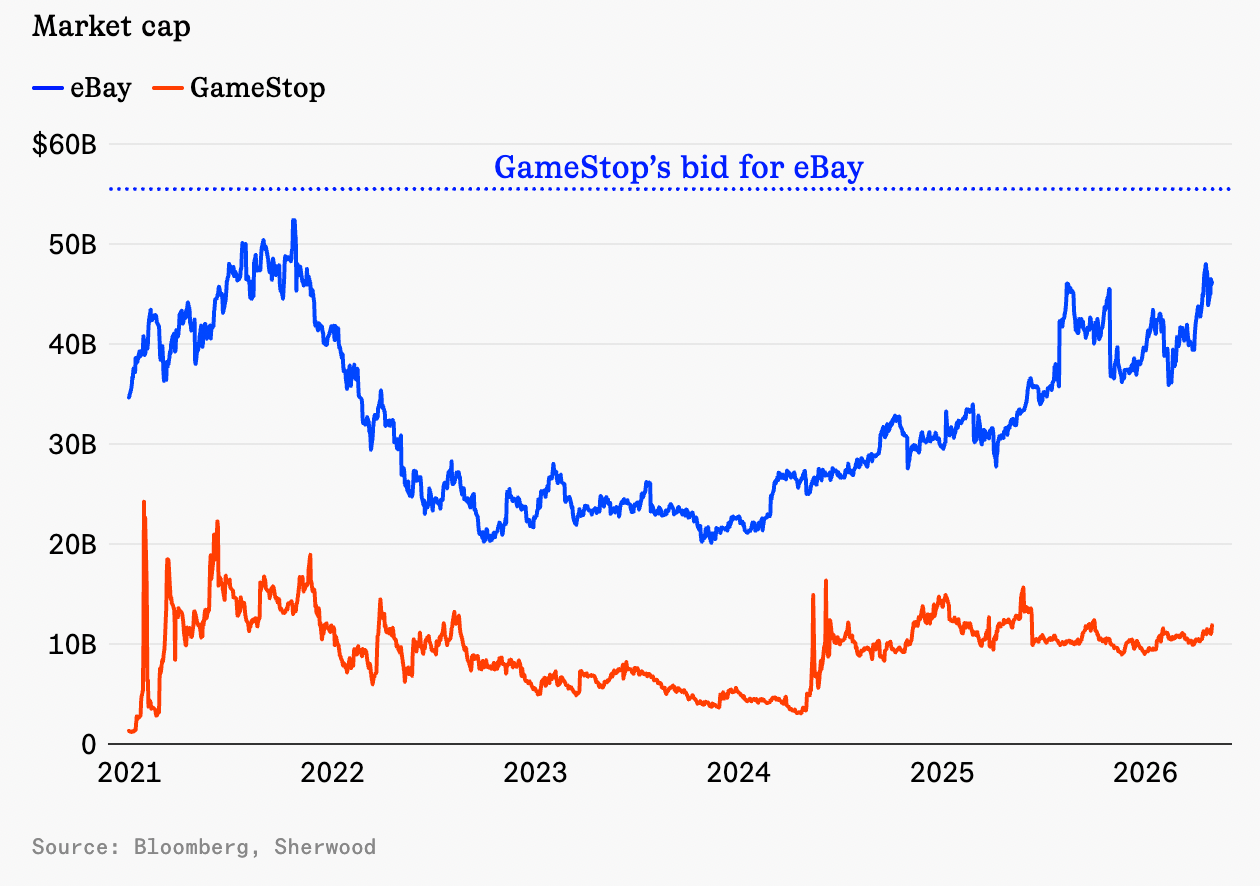

The Most Expensive “What If” Ever

The Spoiler Alert…

Before we talk numbers, we need to talk about Charlie Munger.

Munger — Warren Buffett’s right hand for 45 years, the guy who turned “I’m just a poor man’s Buffett” into a philosophy — once said something that aged so well it should be in a museum:

“When a manager with a reputation for brilliance tackles a business with a reputation for bad economics, it is the reputation of the business that remains intact.”— Charlie Munger

Translation: it doesn’t matter how smart you are. A bad business will humble you every time.

Keep that in your back pocket. We’re coming back to it.

Here’s the story ⇩

SPONSOR BREAK presented by InvestorPlace*

Trump Just Named His Secret AI Project. It’s Called “Golden Dawn.”

When a secretive project gets a name, it means we’re closer to a breakthrough than most people think. Behind the razor wire of a hidden government lab in Tennessee, 40,000 scientists are finishing work on an AI computer 283 trillion times more powerful than today’s data centers — spanning more than 700 miles and built to speed up AI breakthroughs by 36,000%. When Golden Dawn launches, it could instantly leapfrog ChatGPT, Gemini, and Grok — and trigger a $100 trillion reset of the AI markets. Louis Navellier is revealing the one stock at the center of it — down to the ticker — but only through May 5th.

The Offer

Six months ago, Ryan Cohen stood in front of GameStop shareholders and told them he was looking for an acquisition that could be “genius or totally, totally foolish.“

Most people laughed. The meme stock guy, the one who turned a dying video game retailer into a cash machine through sheer stubbornness, was going shopping. How big could he really go?

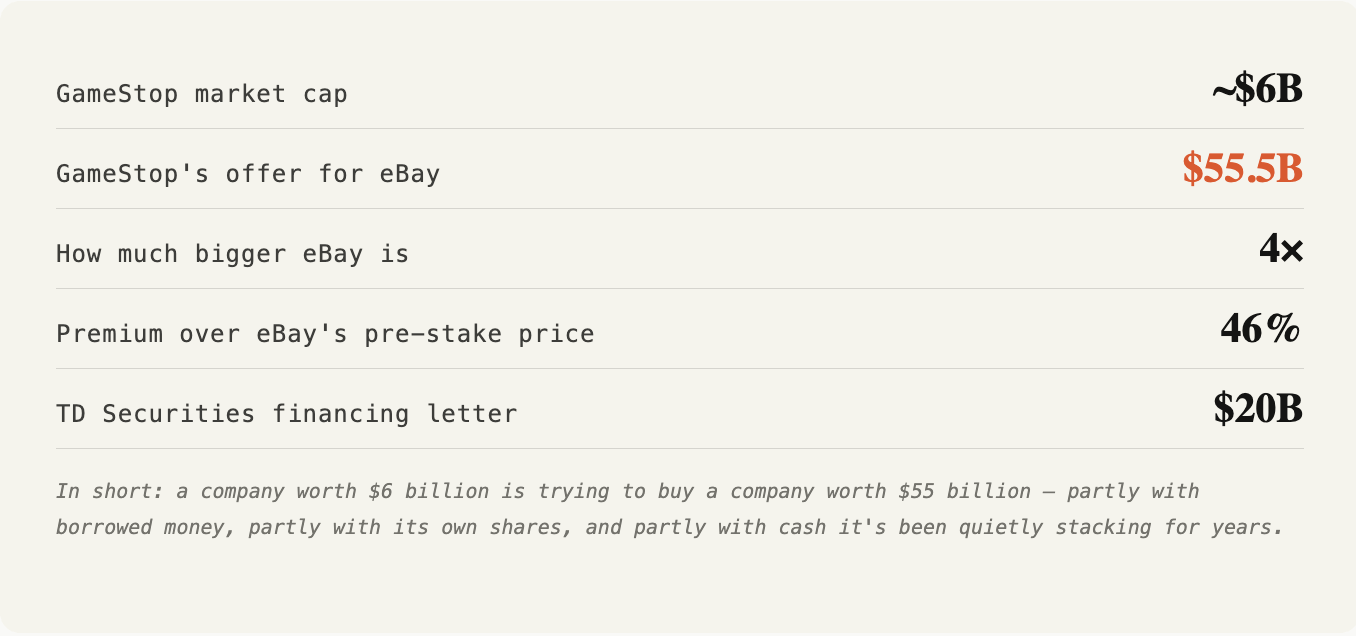

$55.5 billion, as it turns out.

On Sunday evening, GameStop submitted a formal offer to acquire eBay — the original online auction house, the website that taught an entire generation that strangers on the internet would actually mail you things.

The offer is $125 per share, a 46% premium to where eBay was trading before Cohen started quietly accumulating a 5% stake in the company.

Nobody knew he was building it. Months of silence, then a $55 billion letter in your inbox on a Sunday night.

SPONSOR BREAK presented by BanyanHill*

Hidden in Tesla’s Filing: A $12 Billion “Super Startup”

Pull up Tesla’s most recent SEC filing. Page 5.

And you’ll see a single line showing $12 billion in revenue from a brand-new “super startup” Elon Musk has been quietly incubating inside Tesla.

This new “super startup” has nothing to do with cars or robots or space or AI…

But it sits at the center of what Blackstone calls “a $23 trillion investment opportunity.”

And on July 22, Elon is expected to pull back the curtain and reveal exactly what he’s building.

But Adam O’Dell already knows… and he reveals it all in this urgent video.

The Absurd Math

The math is uncomfortable in the best possible way. GameStop is worth roughly $12 billion. The company it wants to buy is worth roughly $46 billion. The financing required — a “highly confident letter” from TD Securities for up to $20 billion — is larger than GameStop itself. About a third of the cash comes from GameStop’s own balance sheet. The rest is borrowed conviction.

Cohen told the Wall Street Journal he is “more qualified than anyone” to run eBay — pointing to his time building Chewy into a pet retail giant before selling it for $3.35 billion at 33 years old.

He also said he’s ready to go to war with shareholders if eBay says no. A proxy battle. Full send.

To be fair — Cohen has earned some audacity. He turned GameStop from a dying mall retailer into a cash-generating machine through brutal expense cuts and discipline. The meme energy got him in the door. The balance sheet kept him there.

But eBay isn’t a turnaround story. It’s a slow bleed that’s been losing ground to Amazon, Etsy, and StockX for a decade.

Great brand. Rough economics. Sound familiar?

SPONSOR BREAK presented by BehindTheMarkets*

Companies are already delaying their IPOs. Why?

Because the SpaceX offering is expected to absorb nearly all the capital in the market.

Bloomberg reported the shift. Citigroup just joined the underwriting team.

The raise could hit $50 billion. But the smart money isn’t just buying the IPO.

They’re positioning into the one chokepoint supplier this $1.75 trillion empire depends on to stay online.

Most investors will see it after the move.

The Guy Who Pressed Sell

Michael Burry — the guy who bet against the entire housing market in 2008 and won — posted three words about the deal on X:

“Makes perfect sense.”

Everyone assumed Burry was bullish.

But he was not bullish.

Burry then published a full piece dripping with sarcasm — and announced he’s selling his GameStop position this week. Here’s what he actually thinks:

Burry, unfiltered

“Neither does this seem revolutionary or ground-breaking in nature. More dilution, or more debt — really, the capital markets strategy here could not be more pedestrian.”

“If GameStop wants to dominate collectibles and used goods with billions of interest expense and all manner of covenants restricting its movements, it will not be breaking new ground. It will be trotting in well-worn ruts on the road to capitalist Hell.”

“Wall Street does indeed mistake debt for creativity, and does so constantly.”

And then Burry pulled out Munger’s quote. The exact one we opened with. He used a Munger’s words as a punchline aimed directly at a living one.

→ GameStop fell 8% Monday.

→ eBay jumped 9%.

SPONSOR BREAK presented by OxfordClub*

Only Hours To Go: Elon’s Biggest Move Ever?

After meeting Elon Musk and analyzing months of research…

Former CIA consultant Dr. Mark Skousen believes June 2026 a potential SpaceX IPO announcement could take place.

He found an “access code” that could let you get exposure ahead of it.

Learn how to claim your stake before time runs out.

So what does it all mean?

→ Ryan Cohen is betting his reputation can rescue eBay’s economics.

→ Burry is betting the economics win.

The market right now has one question it cares about: does this have anything to do with AI?

→ If yes, you get a multiple.

→ If no — whether you’re a meme legend or not — you get skepticism.

Cohen says this deal could be “genius or totally, totally foolish.”

Munger would have told him the business gets to decide.

The market, for now, is voting foolish.

Burry is walking out the door.

And somewhere in the gap between a $6 billion buyer and a $55 billion target, the answer is forming.

Don’t forget to to cast your vote 👇

Lesson Of The Day:

Was this email forwarded to you? Don’t miss out on future stories — subscribe using the button below.

Also, help your friends blossom this spring! Share us with them.

💬 We Want To Hear Your Story:

Got a market or stock you want us to analyze next?

Just drop your request in the comments here.

P.S. – If you no longer want to receive occasional emails from us and you want to unsubscribe, click here 👉 “Unsubscribe” . Thank you!

On A Diet…

Picture the most expensive restaurant you’ve ever been to.

Now imagine every major tech company walks in, sits down, and orders everything on the menu. Twice.

→ Google drops $180-190 billion.

→ Meta slaps down $145 billion.

→ Microsoft and Amazon between them are clearing $300 billion.

The total bill for Big Tech’s 2026 AI infrastructure binge is now north of $700 billion — more than the entire GDP of Switzerland, all of it pointed at data centers, chips, and the existential fear of being the one company that didn’t build enough.

Apple looked at the menu, ordered a side salad, and posted record revenue of $111.2 billion.

iPhone revenue up 20% for the second consecutive quarter.

China — the market everyone had circled in red as Apple’s biggest vulnerability — came in at $20.5 billion against expectations of $18.9 billion.

The stock jumped 5% Friday.

And Apple’s capex for the quarter? $1.9 billion. Down 36% from a year ago.

While every other megacap was shoveling coal into the furnace as fast as humanly possible, Apple spent less than it did last year and somehow came out looking like the smartest person in the room.

The diet is working.

Here’s the story ⇩

SPONSOR BREAK presented by OxfordClub*

Trump Admin to Pump $1 Billion into this “Off-the-Radar” AI Stock

The U.S. government pumped more than $1 billion into Intel. The stock popped 128%. It pumped $400 million into MP Materials. The stock popped 200%. It bought 10% of Trilogy Metals. The stock popped 500%. And now, Trump has chosen this AI stock for a $1 billion payday.

The Menu…

Everyone ordered the same thing. More and faster and bigger.

→ Amazon up 77% on capex year over year.

→ Alphabet up 107%.

→ Microsoft up 85%.

The purple line at the bottom didn’t move. That’s Apple. It also had the best week of anyone at the table.

SPONSOR BREAK presented by BehindTheMarket*

Strange Elon Crates Spotted Near the Hoover Dam

Tesla is shipping thousands of strange white crates to critical locations across America.

And Adam O’Dell, the analyst who recommended Palantir before it became the top performer in the S&P 500, has the scoop…

He says they are part of a new “super startup” that has nothing to do with electric vehicles, space, social media, crypto, biotech, robots or AI…

But it could go down as Elon’s greatest ever disruption…

The Buffet Has a Two-Speed Problem

Google and Meta both reported earnings Wednesday. Both beat expectations. Both raised their already enormous capex forecasts.

→ Alphabet up 6%,

→ Meta down nearly 9% — which tells you everything about what Wall Street actually thinks is going on beneath the surface.

Here’s the difference.

1 Google isn’t just spending on AI infrastructure — it’s selling AI infrastructure.

Those tensor processing unit chips it’s been building for internal use?

Google confirmed this week it’s going to start delivering them to outside customers, with Meta reportedly already in line.

Analysts have estimated that business alone could be worth $900 billion. Google Cloud grew 63% last quarter to over $20 billion in revenue. So when Google raises its capex forecast, it has a receipts to show for it.

2 Meta raised its forecast to $145 billion and when Morgan Stanley asked Mark Zuckerberg directly what signposts he’s watching to make sure that spend generates a return, he said something about building experiences for billions of people and monetizing at scale. Which is technically an answer. It’s just not the answer the question was asking for. And then the cherry on top — daily active users across Meta’s apps dipped for the first time since 2019. First time since 2019. While Meta is committing to its biggest infrastructure spend ever.

Google is building the restaurant and charging everyone rent. → Meta is the customer who keeps ordering more food while telling you the bill will sort itself out eventually.

SPONSOR BREAK presented by OxfordClub*

Only Hours To Go: Elon’s Biggest Move Ever?

After meeting Elon Musk and analyzing months of research…

Former CIA consultant Dr. Mark Skousen believes June 2026 a potential SpaceX IPO announcement could take place.

He found an “access code” that could let you get exposure ahead of it.

Learn how to claim your stake before time runs out.

The Most Expensive Family Dinner in History

Tesla’s amended annual filing dropped this week and it is genuinely one of the more fascinating documents in recent corporate history if you’re into the kind of thing where one billionaire’s companies spend half a billion dollars buying from each other.

Here’s the web.

→ xAI paid Tesla $430 million last year, mostly for Megapack battery storage.

→ SpaceX spent $143 million on Tesla products — a big chunk of that almost certainly the $100 million worth of Cybertrucks it purchased in Q4, which works out to roughly one in five Cybertrucks registered in the US that quarter being bought by Musk’s own rocket company.

→ Tesla then invested $2 billion in xAI, which merged with SpaceX, which means Tesla now owns a piece of SpaceX.

! The company that sold batteries to the AI startup that merged with the rocket company that bought the trucks now has equity in all of it

source: sherwood

Meanwhile the Tesla Semi finally rolled off the high-volume production line in Sparks, Nevada — about nine years after Elon Musk first unveiled it, with production targets missed in 2019, 2020, and several years after that. It’ll run you $260,000 for standard range or $290,000 for long range. Tesla is targeting 50,000 units per year. Frito-Lay has been testing it since 2022 and presumably has opinions.

Tesla’s CFO also confirmed capex will exceed $25 billion this year, pushing free cash flow negative for the rest of 2026.

The stock dropped 7% last week, recovered about 2% this week, and Elon Musk’s disclosed 2025 compensation came in at $158 billion — entirely in equity, none of it actually realized, all contingent on targets that weren’t hit, so his actual realized pay was zero.

The gap between $158 billion and zero is doing a lot of work in that sentence.

So What Does the Side Salad Mean?

Apple has real problems ahead — margin pressure from the global memory shortage, a CEO transition from Tim Cook to John Ternus in September, a foldable iPhone in the pipeline, and an AI strategy that is currently best described as “we’re working on it.” WWDC on June 8 is when that story either starts making sense or gets more complicated.

But here’s what this week actually showed: you can skip the $700 billion infrastructure arms race, partner with Google for your AI, spend 36% less than you did last year, and still post record revenue while your stock tests all-time highs.

Apple isn’t winning because of its AI strategy.

It’s winning despite not having one yet.

That’s either the most impressive thing in tech right now, or the calm before something gets very awkward in June.

Either way, the side salad is still on the table.

Don’t forget to to cast your vote 👇

Lesson Of The Day:

Was this email forwarded to you? Don’t miss out on future stories — subscribe using the button below.

Also, help your friends blossom this spring! Share us with them.

💬 We Want To Hear Your Story:

Got a market or stock you want us to analyze next?

Just drop your request in the comments here.

P.S. – If you no longer want to receive occasional emails from us and you want to unsubscribe, click here 👉 “Unsubscribe” . Thank you!

See You Wednesday 4:01pm

All In. 🃏

In poker, going “all in” means one thing.

You’re not hedging or folding. You’re pushing every chip you have to the middle of the table and telling everyone else in the room: I believe in this hand more than you believe in yours.

This Wednesday at 4:01pm, four of the most powerful companies on Earth are turning their cards over.

1 Microsoft.

2 Alphabet.

3 Meta.

4 Amazon.

They’ve already gone all in.

$670 billion committed to AI infrastructure this year alone.

→ More than Sweden’s entire GDP.

→ More than America’s entire defense budget.

→ The largest single-year capital expenditure in the history of business.

Wednesday is when we find out if the hand was worth playing.

Here’s the story ⇩

SPONSOR BREAK presented by OxfordClub*

Only Hours To Go: Elon’s Biggest Move Ever?

After meeting Elon Musk and analyzing months of research…

Former CIA consultant Dr. Mark Skousen believes June 2026 a potential SpaceX IPO announcement could take place.

He found an “access code” that could let you get exposure ahead of it.

Learn how to claim your stake before time runs out.

What $670 Billion Actually Looks Like.

To understand what $670 billion actually means, you need to understand what these companies are building.

Every time you use ChatGPT, ask Gemini a question, or get a recommendation from an AI — somewhere, a data center full of chips is doing an enormous amount of work. And those data centers need to be built, cooled, powered, and staffed.

They need:

→ land,

→ fiber,

→ electricity,

→ and above all else — chips… Nvidia chips. Lots of them.

The four hyperscalers have been building these warehouses at a pace that should make your head spin:

→ Microsoft MSFT ( ▲ 0.38% ) : ~$146 billion in capex this year — up 89% from last year

→ Alphabet GOOG ( ▼ 0.37% ) : $175-185 billion — double what it spent in 2024

→ Meta META ( ▼ 0.97% ) : $115-135 billion — Zuckerberg called it “a defining investment”

→ Amazon AMZN ( ▼ 0.73% ) : expected to cross $170 billion

→ Combined: $670 billion

→ For context: Alphabet’s entire capex five years ago was $22 billion

Goldman Sachs estimates AI investment will drive roughly 40% of all S&P 500 earnings growth in 2026.

That’s not a side bet. That’s the whole thesis.

SPONSOR BREAK presented by BehindTheMarket*

“Forget AI” Says Reagan’s #1 Futurist

While everyone’s chasing the same AI plays, George Gilder is focused on something completely different.

He says a 4-nanometer device that’s 80 MILLION times more powerful than the chip he gave Reagan is now being made in America for the first time.

And he’s identified 3 companies that control this technology.

Get the details before this BOMBSHELL announcement changes everything.

The Nervous Table.

Here’s what happened today — the day before the cards flip.

The Wall Street Journal published a report raising questions about whether OpenAI’s growth can actually support the massive data center spending commitments companies have made around it. Just a question mark showing up at the table at the worst possible moment.

The chip market answered immediately.

The PHLX Semiconductor Index had just finished an 18-day winning streak — 13 straight record highs at the end of the run. Today, it fell 3.16% in a single session. The names that ran the hardest got hit the hardest:

→ CoreWeave $CRWV ( ▼ 5.83% ) : down 3.86%

→ Oracle $ORCL ( ▼ 4.05% ) : down 3.56%

→ Nvidia $NVDA ( ▼ 1.59% ) : down 1.32%

→ Rambus, Arm, FormFactor, Wolfspeed: all under pressure

→ Even Intel — up 100% since March 30 — got pulled into the selloff

This is what happens at a poker table when someone starts to wonder if the player who went all in is bluffing — the whole table gets nervous.

Nobody has folded yet. But everyone is watching very carefully.

SPONSOR BREAK presented by BehindTheMarket*

Hate It Or Love It — Fortunes Will Be Made From This…

President Trump just signed a highly controversial new law — S.1582.

With one stroke of the pen, he’s unleashed the most radical change to America’s money in over 100 years.

Investors who understand what’s happening and position themselves now could make as much as 40X their money by 2032.

While the rest will be left scrambling in the dust, wondering how they missed it.

Go here now for details – before the wealth transfer begins on June 11th.

Wednesday At 4:01pm.

Reddit’s WallStreetBets has already named it: “the REAL WW3 on Wednesday at 4:01 PM.”

They’re not wrong about the stakes.

When Microsoft, Alphabet, Meta, and Amazon all report after the bell on Wednesday — simultaneously — the market will be laser focused on one number.

→ Capex guidance.

If these four companies raise their AI spending plans — or even hold them steady — it’s the market equivalent of flipping over a royal flush.

The chip stocks that sold off Tuesday come roaring back. The AI trade extends. The $670 billion wasn’t a bluff.

If even one of them softens the language — uses words like “digestion” or “optimization” or “measured investment pace” — the table goes quiet very fast. Traders start pressing the names that ran the farthest and today’s selloff becomes something more serious.

What to watch on Wednesday:

→ Azure growth consensus: ~38%

→ Google Cloud growth consensus: ~28%

→ AWS growth consensus: ~18%

→ Meta ad revenue: watching price per ad closely

→ Free cash flow: Alphabet’s expected to drop 70% as spending surges

→ Any softening in capex language: the most dangerous two words this week are “we’re optimizing”

SPONSOR BREAK presented by ParadigmPress*

AI could wipe out Social Security funding by 2027?

Most people have no idea this is happening…

But AI could gut the funding base for Social Security by the end of 2027…

Leaving millions of American seniors funds completely vanished.

But former $4 billion hedge fund legend has seen what’s coming and put together a presentation detailing exactly how AI could collapse the funding base for social security and what to do as AI turns the economy upside down…

Click here to see his three recommended moves.

Pot Committed.

The $670 billion is already flowing — into data centers, into chips, into cooling systems and fiber cables and land.

The hand is already played. The chips are already in the middle.

Wednesday is just the moment everyone turns their cards over.

If the capex holds — or rises — the table relaxes and the game continues. If it softens, the next few months get very interesting.

Either way, nobody at this table is getting their chips back.

Don’t forget to to cast your vote 👇

Lesson Of The Day:

Was this email forwarded to you? Don’t miss out on future stories — subscribe using the button below.

Also, help your friends blossom this spring! Share us with them.

💬 We Want To Hear Your Story:

Got a market or stock you want us to analyze next?

Just drop your request in the comments here.

P.S. – If you no longer want to receive occasional emails from us and you want to unsubscribe, click here 👉 “Unsubscribe” . Thank you!

Show Me The Money

The Verdict.

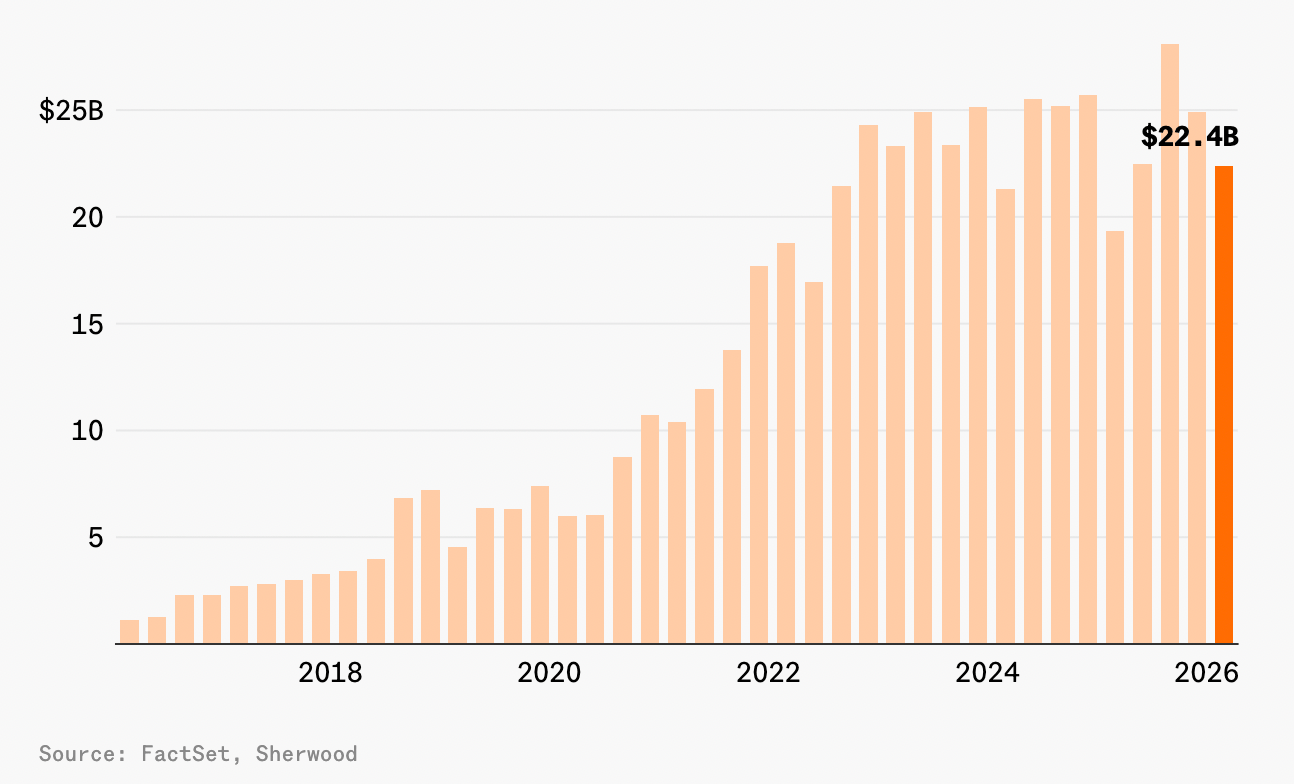

Intel walked into the bond market this week asking for $6.5 billion.

Wall Street sent back $50 billion.

That’s a verdict.

Seven times the amount requested, from the most serious, least excitable investors on Earth — pension funds, insurance companies, sovereign wealth funds. People who don’t get carried away. People who do the math and check the books.

This week three companies found out their verdict:

1 Intel got a standing ovation.

2 Walmart got a nod.

3 And Boaz Weinstein found out that even distressed investors have their limits.

Here’s the story ⇩

SPONSOR BREAK presented by OxfordClub*

Elon Musk: “The Only Thing That Can Solve It”

In a bombshell interview, Elon Musk declared that AI and robotics are “the only thing” that can solve America’s $38 trillion debt crisis. He predicts it will happen within three years. One Wall Street veteran has identified a single fund at the center of this AI buildout – and you can get in for less than $20.

See what Musk didn’t tell you >>

Intel: Everyone Was Wrong.

A year ago, Intel was the cautionary tale everyone in tech was pointing at.

Layoffs. A new CEO. Analysts quietly writing the obituary.

The company that invented the modern processor somehow missed the biggest technology wave in a generation while Nvidia became the most valuable company on Earth. If you wanted to explain what happens when a giant falls asleep, you pulled up Intel’s stock chart.

Here is what everyone missed.

AI data centers are not just Nvidia GPU farms. They need CPUs — the generalist chips that run the actual services, handle the requests, and turn all that AI software into something businesses can charge money for. Think of GPUs as the engine and CPUs as everything else that makes the car actually drive.

Intel makes those.

And as companies started building out their AI infrastructure for real, Intel’s Xeon server processors went from an afterthought to something nobody could do without.

Last week Intel’s current-quarter sales forecast shattered Wall Street expectations. Shares hit a record high. And this week they went to the bond market to raise $6.5 billion — to buy back the 49% stake in their Irish chip factory they sold to Apollo Global Management in 2024 when they desperately needed cash.

Wall Street sent back $50 billion.

→ Bond size: $6.5 billion

→ Orders received: $50 billion — 7.7x oversubscribed

→ Maturities: 5 to 40 years

→ Longest note: due 2066, priced tighter than expected

→ Use of proceeds: buy back Irish Fab 34 from Apollo

→ Intel shares: at a record high

→ US government: holds 10% stake in Intel

The company that sold its factory to survive just bought it back.

And Wall Street lined up around the block to help.

SPONSOR BREAK presented by OxfordClub*

Only Hours To Go: Elon’s Biggest Move Ever?

After meeting Elon Musk and analyzing months of research…

Former CIA consultant Dr. Mark Skousen believes June 2026 a potential SpaceX IPO announcement could take place.

He found an “access code” that could let you get exposure ahead of it.

Learn how to claim your stake before time runs out.

Walmart: The Nod.

Walmart didn’t need to do anything dramatic this week.

It never does.

The world’s largest retailer walked into the bond market asking for $3 billion and left with $4.25 billion — at a lower rate than it asked for.

During the sale process, Walmart’s borrowing costs actually went down because demand was so strong. The longest tranche priced at 0.43 percentage points above Treasuries, roughly a quarter point less than initial price talk.

That’s what happens when you are so reliable, so consistent, so utterly unshakeable that the bond market doesn’t even make you sweat.

Walmart has $648 billion in annual revenue, stores in every zip code, and a business model that grows whether the economy is booming or collapsing.

Walmart raised $4.25 billion this week. They asked for $3 billion.

The extra $1.25 billion? General corporate purposes.

→ Initial target: $3 billion

→ Final raise: $4.25 billion

→ Borrowing cost: went DOWN during the sale

→ Longest tranche: 0.43 points above Treasuries — well below initial talk

→ Part of a $24.3 billion investment grade Monday session

→ Last bond sale: $4 billion in April 2025

Walmart’s verdict came back in about thirty seconds.

“Obviously. Next.”

SPONSOR BREAK presented by ParadigmPress*

AI could wipe out Social Security funding by 2027?

Most people have no idea this is happening…

But AI could gut the funding base for Social Security by the end of 2027…

Leaving millions of American seniors funds completely vanished.

But former $4 billion hedge fund legend has seen what’s coming and put together a presentation detailing exactly how AI could collapse the funding base for social security and what to do as AI turns the economy upside down…

Click here to see his three recommended moves.

Boaz Weinstein: The Limits Of Pessimism.

Boaz Weinstein runs Saba Capital Management, he has a reputation for finding value where others see disaster. His whole business model is finding funds where investors are trapped, and quietly desperate — then offering to buy them out at a discount before things get worse.

He is essentially a professional pessimist. 🙂

This time he thought he found it in Blue Owl Capital Corp. II — one of Blue Owl’s private credit funds.

The private credit market has been under real stress.

– Concerns about loan quality.

– AI disruption eating into software company revenues.

– A rough stretch for non-traded funds.

Blue Owl even told investors in February they could no longer redeem shares quarterly — which is the kind of news that usually sends investors running for the exit.

!!! And still…less than 1% of investors said yes.

The tender offer expired last week with almost no takers.

Actually, the story is pretty simple→ Investors looked at Weinstein’s offer, → looked at their Blue Owl position, → and decided they’d rather wait than sell at a discount to someone who was betting against them.

→ Weinstein’s next move: eyeing Cliffwater and Blue Owl Credit Income Corp.

→ New position: $40 million in publicly traded FS KKR Capital Corp.

Weinstein was buying pessimism. → Turns out there wasn’t enough of it to go around.

Don’t forget to to cast your vote 👇

Read The Room.

The bond market doesn’t care about press releases, vision deck or exciting strategic pivot.

It asks one question: do we trust you with our money for the next 5, 10, 40 years?

This week Intel said “we’re back” and got believed.

Walmart said nothing and got everything it asked for.

And Boaz Weinstein learned that even stressed investors have a floor below which they won’t go.

Three verdicts. Three very different answers to the same question.

Lesson Of The Day:

Was this email forwarded to you? Don’t miss out on future stories — subscribe using the button below.

Also, help your friends blossom this spring! Share us with them.

💬 We Want To Hear Your Story:

Got a market or stock you want us to analyze next?

Just drop your request in the comments here.

P.S. – If you no longer want to receive occasional emails from us and you want to unsubscribe, click here 👉 “Unsubscribe” . Thank you!

The Sexiest IPO-s

Unsexy?

Two completely unsexy businesses just had the sexiest IPO week of 2026.

One has been making sandwiches in New Jersey since 1956. The other makes uranium pellets the size of a poppyseed.

No algorithms or AI wrapper. No founder in a black turtleneck telling you they’re changing the world.

Just sandwiches and atoms.

Between them they raised over $13 billion this week.

And Wall Street — the same Wall Street that spent the last five years throwing money at anything with “AI” in the name — couldn’t write the checks fast enough.

Here’s the story ⇩

Don’t forget to to cast your vote 👇

The Bamboo Story.

Here is a fun fact about bamboo that most people don’t know.

Bamboo spends the first five years growing entirely underground. You water it every day, nothing appears above the surface, and most people would look at that patch of dirt and assume something went wrong. Then in year five it shoots up 90 feet in six weeks — the fastest growing plant on Earth, after what looked like nothing happening at all.

In 1956, a man named Mike opened a submarine sandwich shop on the Jersey Shore. Nothing fancy. Just a sub shop, freshly baked bread, the kind of place you go because the sandwich is really good.

1975, a 17-year-old kid named Peter Cancro who worked there convinced his football coach to loan him the money to buy it. He spent the next nine years running one sandwich shop in New Jersey before he started franchising. Nine years of freshly baked bread every day, the same way it had been done since the shop opened in 1956.

Nobody was writing about Jersey Mike’s in 1984. Or 1994. Or 2004.

Subway was everywhere. Arby’s was everywhere.

And Jersey Mike’s was just quietly watering its bamboo, building its root system one freshly baked loaf at a time, in a way that the giants had long since decided wasn’t worth the operational complexity.

The Root System.

While Subway was chasing global domination and Arby’s was expanding its menu and both were doing everything that fast food chains are supposed to do to win — Jersey Mike’s was doing one thing…

→ Making a better sandwich.

Freshly baked bread on premises. Every single day. Every single location. No shortcuts, no frozen loaves, no cutting corners on the thing that matters most in a sandwich shop. Peter Cancro spent 50 years obsessing over one detail that his competitors stopped caring about the moment they got big enough to cut costs.

In an industry that had spent thirty years optimizing for cost and convenience at the expense of everything else, Jersey Mike’s had spent thirty years optimizing for the sandwich.

The result:

→ Jersey Mike’s is now America’s third largest sandwich chain by store count

→ Added 275+ new stores every year for the last three years

→ Subway store count: down 3% in 2024

→ Arby’s store count: down 1% in 2024

→ Jersey Mike’s: still growing, announcing 400 new franchises across the UK and Ireland

That’s the root system. Invisible to everyone watching the surface. Absolutely everything underground.

The 90 Feet.

In January 2025, Blackstone paid $8 billion for Jersey Mike’s.

Fifteen months later, Jersey Mike’s confidentially filed for an IPO targeting a valuation of at least $12 billion, working with Morgan Stanley, JPMorgan, and Jefferies on the offering.

A $4 billion markup in fifteen months. On a sandwich shop.

The bamboo just went 90 feet.

And the giants who had every advantage — the ones with 16,000 more locations, the ones with bigger marketing budgets and global brand recognition and decades of scale — are shrinking while a sub shop from New Jersey is announcing 400 new franchises across the UK and Ireland.

Eli Manning and Danny DeVito are investors, by the way. 😉

Boring Is The New Brilliant.

Now forget the sandwich for a second.

X-Energy makes nuclear reactors – small and modular. The kind you can build over and over in a factory rather than spending fifteen years constructing on site. And their fuel — this is the part worth pausing on — comes in the form of Triso pebbles. Tristructural isotropic uranium kernels. The size of a poppyseed.

Each one burns hotter and longer than conventional nuclear fuel. And together they power a reactor that X-Energy’s CEO Clay Sell describes with a phrase you don’t normally hear in the nuclear industry:

“We want to make nuclear boring.”

Boring meaning repeatable.

Boring meaning predictable.

Boring meaning you can build it over and over and over again and drive costs down the way you drive costs down in any manufacturing business — through repetition, standardization, and scale.

The market heard “boring nuclear” and immediately got very excited.

The Numbers.

The IPO was more than 15 times oversubscribed. Meaning for every share available, fifteen investors wanted it.

→ IPO raise: $1.02 billion — upsized from the original target

→ IPO price: $23 per share, above the marketed range of $16 to $19.

→ Opening price: $30.11 on Friday morning — 31% above the IPO price

→ Market value: nearly $12 billion

→ Times oversubscribed: 15x

→ Key customers: Amazon, Dow, Centrica

→ ARK Investment Management: interested in buying up to $105 million at IPO price

→ Target: first reactor delivery by early 2030s

→ Use case: industrial facilities and AI data centers

Amazon is already a customer. Dow is already a customer. ARK wanted $105 million worth at the IPO price. The company lost $390 million last year on $94 million in revenue — but nobody seemed to care, because the order book is real and the technology actually works.

X-Energy isn’t profitable yet. But it has something most startups spend years chasing: customers who actually need what it’s building, in an industry — AI data centers — that is so hungry for power it will take nuclear energy from a poppyseed if that’s what it takes.

The Unsexy Truth.

Turns out the most dangerous thing in any industry isn’t the loudest competitor in the room. It’s the quiet one that never stopped caring about the thing everyone else decided wasn’t worth caring about anymore.

Fresh bread. Poppyseed uranium. $13 billion.

The boring ones win eventually. They always do.

Lesson Of The Day:

Was this email forwarded to you? Don’t miss out on future stories — subscribe using the button below.

Also, help your friends blossom this spring! Share us with them.

💬 We Want To Hear Your Story:

Got a market or stock you want us to analyze next?

Just drop your request in the comments here.

P.S. – If you no longer want to receive occasional emails from us and you want to unsubscribe, click here 👉 “Unsubscribe” . Thank you!

The Sexiest IPO-s

Unsexy?

Two completely unsexy businesses just had the sexiest IPO week of 2026.

One has been making sandwiches in New Jersey since 1956. The other makes uranium pellets the size of a poppyseed.

No algorithms or AI wrapper. No founder in a black turtleneck telling you they’re changing the world.

Just sandwiches and atoms.

Between them they raised over $13 billion this week.

And Wall Street — the same Wall Street that spent the last five years throwing money at anything with “AI” in the name — couldn’t write the checks fast enough.

Here’s the story ⇩

Don’t forget to to cast your vote 👇

The Bamboo Story.

Here is a fun fact about bamboo that most people don’t know.

Bamboo spends the first five years growing entirely underground. You water it every day, nothing appears above the surface, and most people would look at that patch of dirt and assume something went wrong. Then in year five it shoots up 90 feet in six weeks — the fastest growing plant on Earth, after what looked like nothing happening at all.

In 1956, a man named Mike opened a submarine sandwich shop on the Jersey Shore. Nothing fancy. Just a sub shop, freshly baked bread, the kind of place you go because the sandwich is really good.

1975, a 17-year-old kid named Peter Cancro who worked there convinced his football coach to loan him the money to buy it. He spent the next nine years running one sandwich shop in New Jersey before he started franchising. Nine years of freshly baked bread every day, the same way it had been done since the shop opened in 1956.

Nobody was writing about Jersey Mike’s in 1984. Or 1994. Or 2004.

Subway was everywhere. Arby’s was everywhere.

And Jersey Mike’s was just quietly watering its bamboo, building its root system one freshly baked loaf at a time, in a way that the giants had long since decided wasn’t worth the operational complexity.

The Root System.

While Subway was chasing global domination and Arby’s was expanding its menu and both were doing everything that fast food chains are supposed to do to win — Jersey Mike’s was doing one thing…

→ Making a better sandwich.

Freshly baked bread on premises. Every single day. Every single location. No shortcuts, no frozen loaves, no cutting corners on the thing that matters most in a sandwich shop. Peter Cancro spent 50 years obsessing over one detail that his competitors stopped caring about the moment they got big enough to cut costs.

In an industry that had spent thirty years optimizing for cost and convenience at the expense of everything else, Jersey Mike’s had spent thirty years optimizing for the sandwich.

The result:

→ Jersey Mike’s is now America’s third largest sandwich chain by store count

→ Added 275+ new stores every year for the last three years

→ Subway store count: down 3% in 2024

→ Arby’s store count: down 1% in 2024

→ Jersey Mike’s: still growing, announcing 400 new franchises across the UK and Ireland

That’s the root system. Invisible to everyone watching the surface. Absolutely everything underground.

The 90 Feet.

In January 2025, Blackstone paid $8 billion for Jersey Mike’s.

Fifteen months later, Jersey Mike’s confidentially filed for an IPO targeting a valuation of at least $12 billion, working with Morgan Stanley, JPMorgan, and Jefferies on the offering.

A $4 billion markup in fifteen months. On a sandwich shop.

The bamboo just went 90 feet.

And the giants who had every advantage — the ones with 16,000 more locations, the ones with bigger marketing budgets and global brand recognition and decades of scale — are shrinking while a sub shop from New Jersey is announcing 400 new franchises across the UK and Ireland.

Eli Manning and Danny DeVito are investors, by the way. 😉

Boring Is The New Brilliant.

Now forget the sandwich for a second.

X-Energy makes nuclear reactors – small and modular. The kind you can build over and over in a factory rather than spending fifteen years constructing on site. And their fuel — this is the part worth pausing on — comes in the form of Triso pebbles. Tristructural isotropic uranium kernels. The size of a poppyseed.

Each one burns hotter and longer than conventional nuclear fuel. And together they power a reactor that X-Energy’s CEO Clay Sell describes with a phrase you don’t normally hear in the nuclear industry:

“We want to make nuclear boring.”

Boring meaning repeatable.

Boring meaning predictable.

Boring meaning you can build it over and over and over again and drive costs down the way you drive costs down in any manufacturing business — through repetition, standardization, and scale.

The market heard “boring nuclear” and immediately got very excited.

The Numbers.

The IPO was more than 15 times oversubscribed. Meaning for every share available, fifteen investors wanted it.

→ IPO raise: $1.02 billion — upsized from the original target

→ IPO price: $23 per share, above the marketed range of $16 to $19.

→ Opening price: $30.11 on Friday morning — 31% above the IPO price

→ Market value: nearly $12 billion

→ Times oversubscribed: 15x

→ Key customers: Amazon, Dow, Centrica

→ ARK Investment Management: interested in buying up to $105 million at IPO price

→ Target: first reactor delivery by early 2030s

→ Use case: industrial facilities and AI data centers

Amazon is already a customer. Dow is already a customer. ARK wanted $105 million worth at the IPO price. The company lost $390 million last year on $94 million in revenue — but nobody seemed to care, because the order book is real and the technology actually works.

X-Energy isn’t profitable yet. But it has something most startups spend years chasing: customers who actually need what it’s building, in an industry — AI data centers — that is so hungry for power it will take nuclear energy from a poppyseed if that’s what it takes.

The Unsexy Truth.

Turns out the most dangerous thing in any industry isn’t the loudest competitor in the room. It’s the quiet one that never stopped caring about the thing everyone else decided wasn’t worth caring about anymore.

Fresh bread. Poppyseed uranium. $13 billion.

The boring ones win eventually. They always do.

Lesson Of The Day:

Was this email forwarded to you? Don’t miss out on future stories — subscribe using the button below.

Also, help your friends blossom this spring! Share us with them.

💬 We Want To Hear Your Story:

Got a market or stock you want us to analyze next?

Just drop your request in the comments here.

P.S. – If you no longer want to receive occasional emails from us and you want to unsubscribe, click here 👉 “Unsubscribe” . Thank you!

“Leave The Gun. Take The Cannoli.“

Who does not like cannoli?

Last night I watched The Godfather again.

You know how it happens. Ninety minutes of scrolling Netflix, nothing looks good, and you end up back at… a classic.

There’s a scene where Peter Clemenza’s driver has just carried out a hit. Body in the front seat. Dark road. Clemenza, completely unbothered, turns to him and says:

“Leave the gun. Take the cannoli.”

Just a man who knows exactly what matters and what doesn’t.

I couldn’t stop thinking about that scene this week.

Because while hedge funds were staring at the gun — Iran, tariffs, oil surging, the Strait of Hormuz shutting down — retail traders were doing something completely different.

They took the cannoli.

Here’s the story ⇩

SPONSOR BREAK presented by BanyanHill*

Reagan’s Tech Prophet Issues Warning

George Gilder handed President Reagan the first microchip that helped create $6.5 trillion in wealth over the last 40 years. Now he’s stepping forward with an even bigger prediction about what’s being built in the Arizona desert.

He believes 3 little-known companies will explode when a bombshell announcement just days from now. Smart investors are already positioning themselves.

Click here to see what’s coming before the story goes mainstream.

The Gun.

Throughout April, the market had plenty of guns to look at.

1 The Iran war was escalating.

2 The Strait of Hormuz — the narrow waterway that carries roughly 20% of the world’s oil — was under pressure.

3 Oil was surging.

4 Tariffs were biting.

The kind of month where serious, institutional money managers look at their screens and start making very serious, institutional decisions.

Hedge funds sold – broadly, aggressively, defensively. They trimmed broad-based ETF exposure. The SPDR S&P 500 ETF saw massive outflows. The ProShares UltraPro QQQ followed.

The Mag 7 composite dropped from $65 at the start of the year to $55 in late March and early April. A 15% drop in the most important stocks on Earth.

Everyone was looking at the gun.

SPONSOR BREAK presented by BanyanHill*

Hate It Or Love It — Fortunes Will Be Made From This…

President Trump just signed a highly controversial new law — S.1582.

With one stroke of the pen, he’s unleashed the most radical change to America’s money in over 100 years.

Investors who understand what’s happening and position themselves now could make as much as 40X their money by 2032.

While the rest will be left scrambling in the dust, wondering how they missed it.

Go here now for details— before the wealth transfer begins on June 11th.

The Cannoli.

Retail traders did something different.

While institutions were selling everything, retail pulled back as well… but not from everything.

The exceptions were Nvidia, Tesla, Meta, Microsoft. The Magnificent Seven. The stocks retail investors have never really stopped believing in — through tariffs, through Iran, through every macro headline that sent hedge funds scrambling for the exits.

JPMorgan strategist Arun Jain flagged it in real time. Retail investors were selling into strength across ETFs and broad market exposure.

But Mag 7? They kept buying.

While the professionals debated macro risk, retail picked up the cannoli and walked out.

SPONSOR BREAK presented by OxfordClub*

How Mitt Romney Turned $450K Into Up to $100 Million (Tax-Free)

It wasn’t stocks. It wasn’t real estate. It was a little-known investment vehicle that turned Mitt Romney’s $450,000 into as much as $100 million and Peter Thiel used to turn $2,000 into $5 billion within two decades. Now, thanks to a new executive order, regular Americans can access the same type of investment. Get more details here >>

The Offer They Couldn’t Refuse.

The Mag 7 composite is now at $66.32. Above where it started the year.

The entire 15% ▼ drawdown — erased.

And hedge funds are buying back in.

Goldman Sachs’ Cullen Morgan wrote it plainly this week: hedge funds “have started buying Mag 7 stocks again this month.” JPMorgan’s own strategists noted that retail buying tends to crowd in institutional buyers — retail investors essentially forced institutions to follow them back into the trade.

Goldman even told clients directly to piggyback on stocks beloved by retail traders.

The most sophisticated money managers on Earth. Following retail. Back into the stocks retail never left.

→ Mag 7 composite: from $55 at the low back to $66.32

→ Mag 7 YTD: down just 1.3% after the full recovery

→ Amazon: up 8% YTD — top Mag 7 performer

→ Mag 7 share of S&P 500: 33.7% — up from 12.5% in 2016

→ Hedge funds: buying back in after following retail out

→ Goldman Sachs to clients: piggyback retail traders

SPONSOR BREAK presented by BehindTheMarkets*

A U.S. “birthright” claim worth trillions – activated quietly

A tiny government task force working out of a strip mall just finished a 20-year mission.

And with almost no media coverage, they confirmed one of the largest U.S. territorial expansions in modern history…

A resource claim worth an estimated $500 trillion.

Thanks to sovereign U.S. law, this isn’t just a national asset.

It’s an American birthright.

That means every citizen now has the legal right to stake a claim…

But very few even know the opportunity exists.

If you want to see how you can get in line for your portion of this record-breaking windfall…

I’ve assembled everything you need to see inside a new, time-sensitive briefing:

Get all the details here – while the claim window remains open.

Here’s The Thing About The Cannoli.

Clemenza’s wife just asked him to bring home cannoli.

And he did.

It’s normalcy inside chaos. That’s the whole story.

Mag 7 was the cannoli around the chaos.

→ Nvidia NVDA ( ▼ 1.7% ) — the picks and shovels of AI

→ Apple AAPL ( ▲ 0.45% ) — the device in everyone’s pocket

→ Microsoft MSFT ( ▼ 3.91% ) — the cloud, the office, the AI

→ Alphabet GOOG ( ▲ 0.07% ) — the internet’s landlord

→ Amazon AMZN ( ▲ 0.08% ) — commerce, cloud, everything

→ Meta META ( ▼ 2.17% ) — where 3 billion people spend their time

→ Tesla TSLA ( ▼ 3.61% ) — the EV/AI/robot wildcard

Retail went there because these are certainties dressed up as stocks. Whatever happens in the world, people still use Google, still buy on Amazon, still scroll Instagram, still need Nvidia chips.

Don’t forget to to cast your vote 👇

Lesson Of The Day:

Was this email forwarded to you? Don’t miss out on future stories — subscribe using the button below.

Also, help your friends blossom this spring! Share us with them.

💬 We Want To Hear Your Story:

Got a market or stock you want us to analyze next?

Just drop your request in the comments here.

P.S. – If you no longer want to receive occasional emails from us and you want to unsubscribe, click here 👉 “Unsubscribe” . Thank you!

“Leave The Gun. Take The Cannoli.“

Who does not like cannoli?

Last night I watched The Godfather again.

You know how it happens. Ninety minutes of scrolling Netflix, nothing looks good, and you end up back at… a classic.

There’s a scene where Peter Clemenza’s driver has just carried out a hit. Body in the front seat. Dark road. Clemenza, completely unbothered, turns to him and says:

“Leave the gun. Take the cannoli.”

Just a man who knows exactly what matters and what doesn’t.

I couldn’t stop thinking about that scene this week.

Because while hedge funds were staring at the gun — Iran, tariffs, oil surging, the Strait of Hormuz shutting down — retail traders were doing something completely different.

They took the cannoli.

Here’s the story ⇩

SPONSOR BREAK presented by BanyanHill*

Reagan’s Tech Prophet Issues Warning

George Gilder handed President Reagan the first microchip that helped create $6.5 trillion in wealth over the last 40 years. Now he’s stepping forward with an even bigger prediction about what’s being built in the Arizona desert.

He believes 3 little-known companies will explode when a bombshell announcement just days from now. Smart investors are already positioning themselves.

Click here to see what’s coming before the story goes mainstream.

The Gun.

Throughout April, the market had plenty of guns to look at.

1 The Iran war was escalating.

2 The Strait of Hormuz — the narrow waterway that carries roughly 20% of the world’s oil — was under pressure.

3 Oil was surging.

4 Tariffs were biting.

The kind of month where serious, institutional money managers look at their screens and start making very serious, institutional decisions.

Hedge funds sold – broadly, aggressively, defensively. They trimmed broad-based ETF exposure. The SPDR S&P 500 ETF saw massive outflows. The ProShares UltraPro QQQ followed.

The Mag 7 composite dropped from $65 at the start of the year to $55 in late March and early April. A 15% drop in the most important stocks on Earth.

Everyone was looking at the gun.

SPONSOR BREAK presented by BanyanHill*

Hate It Or Love It — Fortunes Will Be Made From This…

President Trump just signed a highly controversial new law — S.1582.

With one stroke of the pen, he’s unleashed the most radical change to America’s money in over 100 years.

Investors who understand what’s happening and position themselves now could make as much as 40X their money by 2032.

While the rest will be left scrambling in the dust, wondering how they missed it.

Go here now for details— before the wealth transfer begins on June 11th.

The Cannoli.

Retail traders did something different.

While institutions were selling everything, retail pulled back as well… but not from everything.

The exceptions were Nvidia, Tesla, Meta, Microsoft. The Magnificent Seven. The stocks retail investors have never really stopped believing in — through tariffs, through Iran, through every macro headline that sent hedge funds scrambling for the exits.

JPMorgan strategist Arun Jain flagged it in real time. Retail investors were selling into strength across ETFs and broad market exposure.

But Mag 7? They kept buying.

While the professionals debated macro risk, retail picked up the cannoli and walked out.

SPONSOR BREAK presented by OxfordClub*

How Mitt Romney Turned $450K Into Up to $100 Million (Tax-Free)

It wasn’t stocks. It wasn’t real estate. It was a little-known investment vehicle that turned Mitt Romney’s $450,000 into as much as $100 million and Peter Thiel used to turn $2,000 into $5 billion within two decades. Now, thanks to a new executive order, regular Americans can access the same type of investment. Get more details here >>

The Offer They Couldn’t Refuse.

The Mag 7 composite is now at $66.32. Above where it started the year.

The entire 15% ▼ drawdown — erased.

And hedge funds are buying back in.

Goldman Sachs’ Cullen Morgan wrote it plainly this week: hedge funds “have started buying Mag 7 stocks again this month.” JPMorgan’s own strategists noted that retail buying tends to crowd in institutional buyers — retail investors essentially forced institutions to follow them back into the trade.

Goldman even told clients directly to piggyback on stocks beloved by retail traders.

The most sophisticated money managers on Earth. Following retail. Back into the stocks retail never left.

→ Mag 7 composite: from $55 at the low back to $66.32

→ Mag 7 YTD: down just 1.3% after the full recovery

→ Amazon: up 8% YTD — top Mag 7 performer

→ Mag 7 share of S&P 500: 33.7% — up from 12.5% in 2016

→ Hedge funds: buying back in after following retail out

→ Goldman Sachs to clients: piggyback retail traders

SPONSOR BREAK presented by BehindTheMarkets*

A U.S. “birthright” claim worth trillions – activated quietly

A tiny government task force working out of a strip mall just finished a 20-year mission.

And with almost no media coverage, they confirmed one of the largest U.S. territorial expansions in modern history…

A resource claim worth an estimated $500 trillion.

Thanks to sovereign U.S. law, this isn’t just a national asset.

It’s an American birthright.

That means every citizen now has the legal right to stake a claim…

But very few even know the opportunity exists.

If you want to see how you can get in line for your portion of this record-breaking windfall…

I’ve assembled everything you need to see inside a new, time-sensitive briefing:

Get all the details here – while the claim window remains open.

Here’s The Thing About The Cannoli.

Clemenza’s wife just asked him to bring home cannoli.

And he did.

It’s normalcy inside chaos. That’s the whole story.

Mag 7 was the cannoli around the chaos.

→ Nvidia NVDA ( ▼ 1.7% ) — the picks and shovels of AI

→ Apple AAPL ( ▲ 0.45% ) — the device in everyone’s pocket

→ Microsoft MSFT ( ▼ 3.91% ) — the cloud, the office, the AI

→ Alphabet GOOG ( ▲ 0.07% ) — the internet’s landlord

→ Amazon AMZN ( ▲ 0.08% ) — commerce, cloud, everything

→ Meta META ( ▼ 2.17% ) — where 3 billion people spend their time

→ Tesla TSLA ( ▼ 3.61% ) — the EV/AI/robot wildcard

Retail went there because these are certainties dressed up as stocks. Whatever happens in the world, people still use Google, still buy on Amazon, still scroll Instagram, still need Nvidia chips.

Don’t forget to to cast your vote 👇

Lesson Of The Day:

Was this email forwarded to you? Don’t miss out on future stories — subscribe using the button below.

Also, help your friends blossom this spring! Share us with them.

💬 We Want To Hear Your Story:

Got a market or stock you want us to analyze next?

Just drop your request in the comments here.

P.S. – If you no longer want to receive occasional emails from us and you want to unsubscribe, click here 👉 “Unsubscribe” . Thank you!

The Matryoshka Effect🪆

Surprise!!!

In 1900, Russia brought a wooden doll to the Paris World Exhibition that nobody had seen before.

From the outside, a painted peasant woman in a traditional sarafan dress, rosy cheeks, a headscarf. Unremarkable.

But you twisted it open… another doll. Identical in design, smaller in size.

Then opened that one too. And another. Seven dolls total, each one hiding the next, all the way down to a tiny baby carved from a single piece of wood.

The craftsmen who made it had one goal in mind — to surprise.

The doll won a bronze medal. Within a decade, the whole world wanted one. The Russians called it Matryoshka — from Matryona, an old name meaning “little mother.”

The idea was simple: the outer layer is never the whole story. There is always something inside you didn’t know was there.

This week, Elon Musk opened his Matryoshka.

And Wall Street is still counting the dolls.

Here’s the story ⇩

SPONSOR BREAK presented by PriorityGold*

Leaked: Apple’s Secret “Project Mulberry” Could Shake Up $9 Trillion Industry

Bloomberg has unveiled details of Apple’s ultra-classified “Project Mulberry,” a 13-year endeavor Tim Cook hails as “Apple’s greatest contribution to mankind.” Hidden in their supply chain, an obscure company produces a revolutionary chip—smaller than a grain of sand. BlackRock holds 2.8 million shares, while Goldman Sachs boosted its stake by 340%. Act fast—this $30 stock may soar soon. Tech expert Ian King has the full story here…

Tesla’s Matryoshka

Tesla just reported Q1 earnings that beat Wall Street expectations across the board.

→ Revenue came in at $22.39 billion against $22.08 billion expected.

→ EPS hit $0.41 against $0.35 expected.

→ Gross margin landed at 21.7% against 17.7% estimated.

→ The stock jumped 3.9% after hours.

From the outside, that looks like a clean win.

Open it.

1 The core auto business delivered 358,023 vehicles globally — down from expectations, though Tesla blamed an unusually low comparison quarter due to the Model Y changeover.

→ Revenue is still down 9% year over year.

The cheapest Tesla on the market costs $35,000. A cheaper model is reportedly coming, but hasn’t arrived yet.

2 The Robotaxi service expanded to Houston and Dallas this week. Unsupervised. No safety driver. Which sounds a genuine breakthrough until you find out there is currently one car in each city.

One car.

3 Tesla is projecting capital expenditure of over $20 billion this year — more than double last year’s $8.5 billion.

→ Free cash flow is expected to go negative.

The spending is going toward:

→ Cybercab production,

→ Optimus robots,

→ AI compute,

→ new batteries, and

→ a chipmaking facility called Terafab in Austin, Texas.

Musk announced Tuesday that Tesla had completed the final design stage — “taping out” — for its upcoming AI5 chip. The chip is destined for future EVs, massive training clusters, and Optimus robots. Tesla’s own sources told Bloomberg the facility won’t begin manufacturing silicon until 2029.

The outer doll looks great.

The ones inside are still being carved.⇩

SPONSOR BREAK presented by BanyanHill*

Hate It Or Love It — Fortunes Will Be Made From This…

President Trump just signed a highly controversial new law — S.1582.

With one stroke of the pen, he’s unleashed the most radical change to America’s money in over 100 years.

Investors who understand what’s happening and position themselves now could make as much as 40X their money by 2032.

While the rest will be left scrambling in the dust, wondering how they missed it.

Go here now for details— before the wealth transfer begins on June 11th.

$9 Billion Sidequest.

SpaceX announced this week it has sealed the right to acquire Cursor — one of the fastest growing AI coding tools in the world — at a valuation of $9 billion.

A rocket company → buying a coding AI.

The deal structure is unusual even by Musk standards.

→ SpaceX gets the right to acquire Cursor later this year.

→ If the acquisition doesn’t happen, Cursor pays SpaceX $10 billion for their work together.

Either way, SpaceX wins.

Now, let’s open the doll…

SpaceX is preparing for what could be the largest IPO in American history — targeting a valuation of $1.5 trillion this summer.

In the months leading up to that IPO, Musk is acquiring:

→ a coding AI startup,

→ rebuilding xAI from the ground up after saying it “was not built right first time around,” and

→ pivoting SpaceX’s entire stated mission toward space-based data infrastructure and AI computing.

This is unusual pre-IPO behavior. Most CEOs spend the months before a public offering projecting stability, focusing on core business, and avoiding anything that might spook institutional investors.

Musk is doing the opposite.

The rocket company – the mother doll. → Inside it is an AI company. → Inside that is… nobody really knows what’s in the last doll.

That’s the whole point.

SPONSOR BREAK presented by OxfordClub*

How Mitt Romney Turned $450K Into Up to $100 Million (Tax-Free)

It wasn’t stocks. It wasn’t real estate. It was a little-known investment vehicle that turned Mitt Romney’s $450,000 into as much as $100 million and Peter Thiel used to turn $2,000 into $5 billion within two decades. Now, thanks to a new executive order, regular Americans can access the same type of investment. Get more details here >>

The Metamorphosis…

SpaceX started as a rocket company with one mission: make humanity multiplanetary. That mission made Musk a legend, attracted the best aerospace engineers on Earth, and turned SpaceX into the dominant force in commercial space travel.

Now, with the IPO approaching, the mission is quietly expanding.

And each layer you open reveals a different company than the one on the outside.

The market is being asked to value SpaceX at $1.5 trillion. (For context, Boeing’s entire market cap: $97 billion)

$1.5T is a bet on whatever is inside the next doll.

How many are left? Nobody knows.

SPONSOR BREAK presented by StansberryResearch*

Why are companies flying spy planes over Elon’s closely-guarded AI lab?

Elon did the seemingly impossible – far faster than anyone expected… And it’s sent the tech industry into PANIC MODE. ChatGPT, Claude, Google Gemini, and DeepSeek could soon become obsolete. And three little-known firms could soar 10X or higher as a result.

The Doll With No Bottom.

The whole point of Matryoshka is that there is always something inside you didn’t expect.

Musk has been building them his entire career.

Tesla was supposed to be a car company. Inside it was an energy company, a battery company, a robotics company, and now a chipmaker.

SpaceX was supposed to be a rocket company. Inside it is Starlink, xAI, a coding AI acquisition, and a $1.5 trillion IPO.

Twist it open. There’s always another one.

Don’t forget to to cast your vote 👇

Lesson Of The Day:

Was this email forwarded to you? Don’t miss out on future stories — subscribe using the button below.

Also, help your friends blossom this spring! Share us with them.

💬 We Want To Hear Your Story:

Got a market or stock you want us to analyze next?

Just drop your request in the comments here.

P.S. – If you no longer want to receive occasional emails from us and you want to unsubscribe, click here 👉 “Unsubscribe” . Thank you!

Washington Just Kissed A Toad.

Turns out the prince was in the Sonoran Desert the whole time.

In Grimm’s fairy tale, the princess kisses the toad. And it turns into a prince.

For sixty years, psychedelics have been the toad of the medical world. It was sixty years of stigma, until….

Last Saturday, Washington kissed the toad.

President Trump signed an executive order fast-tracking research and FDA approval for psychedelic treatments. The whole spectrum — mushrooms, plants, toads.

And the prince showed up immediately. Stocks across the entire sector exploded before the ink was dry.

But here’s what makes this story genuinely interesting…

The toad was already turning into a prince before anyone in Washington paid attention.

Here’s the story ⇩

SPONSOR BREAK presented by BanyanHill*

Hate It Or Love It — Fortunes Will Be Made From This…

President Trump just signed a highly controversial new law — S.1582.

With one stroke of the pen, he’s unleashed the most radical change to America’s money in over 100 years.

Investors who understand what’s happening and position themselves now could make as much as 40X their money by 2032.

While the rest will be left scrambling in the dust, wondering how they missed it.

Go here now for details— before the wealth transfer begins on June 11th.

But First…

Most people think psychedelics are a 1960s counterculture story.

Hippies. Woodstock. Tie-dye. That’s not where this started.

In the 1950s, psychedelics were legitimate medicine.

Psilocybin was being studied at Harvard. LSD was being tested by major research institutions across the US and Europe. The CIA was running its own experiments. Therapists were using these compounds with patients and reporting results that conventional medicine couldn’t come close to matching — dramatic improvements in depression, anxiety, addiction, and PTSD.

The research was serious and funding was flowing.

Then the counterculture happened.

Psychedelics escaped the labs and became the symbol of everything the establishment was trying to suppress. The anti-war movement. The rebellion. Timothy Leary telling an entire generation to “tune in, turn on, drop out.” Overnight, the drugs went from promising medicine to political liability.

Nixon declared a War on Drugs. The Controlled Substances Act of 1970 threw everything into Schedule I — the same category as heroin.

→ No accepted medical use.

→ No research.

→ No funding.

Scientists who had spent years building promising results had to walk away overnight.

The NIH actually funded ibogaine research in the 1990s — and then quietly shut it down over cardiovascular concerns, leaving the work unfinished.

So the compounds stayed in nature – in mushrooms, in plants, in a toad that lives in the American Southwest. And an entire field of medicine spent thirty years frozen.

Until…

2019, when Mike Tyson went on Joe Rogan’s podcast.⇩

SPONSOR BREAK presented by PriorityGold*

A legal loophole still allows you to move your 401(k) or IRA into a stronger, tax-free zone—before the next wave of chaos hits.

Click here to learn how to shield your money now

Because when the rules break, the rich rewrite them.

You need to make your move before they do.

The Toad That Started It All Over Again.

credit: Metro

In 2019, Tyson told the world he had been smoking secretions from the Sonoran Desert toad — a creature that lives in the American Southwest and naturally produces a substance called 5-MeO-DMT.

People started calling it “the God molecule.” Effects kick in within 30 seconds. The whole experience is over in 20 minutes. Tyson said it cured his depression, his trauma, his addiction.

Researchers got curious. Celebrity after celebrity started sharing similar stories.

→ The New York Times covered it.

→ GQ covered it.

!!! And the National Park Service issued an official warning telling Americans to stop licking the toad.

SPONSOR BREAK presented by StansberryResearch*

Why are companies flying spy planes over Elon’s closely-guarded AI lab?

Elon did the seemingly impossible – far faster than anyone expected… And it’s sent the tech industry into PANIC MODE. ChatGPT, Claude, Google Gemini, and DeepSeek could soon become obsolete. And three little-known firms could soar 10X or higher as a result.

The Science That Was There All Along.

→ Psilocybin grows in mushrooms used in indigenous ceremonies for centuries. → Ibogaine comes from the iboga plant, used in spiritual rituals in Central Africa for generations.

→ 5-MeO-DMT is secreted naturally by the Sonoran Desert toad.

When scientists quietly restarted the research in the 2010s — picking up exactly where Nixon forced them to stop — the results were hard to ignore.

→ A 2013 study found psilocybin genuinely beneficial for PTSD patients.

→ A 2016 trial showed it could treat anxiety and depression.

The data kept coming — not from fringe researchers, but from Johns Hopkins and NYU.

Psychedelics work completely differently. Early trials showed patients reaching remission in days — sometimes after a single afternoon session. A large-scale study published in Nature Medicine found that psychedelics reconfigure brain networks in ways conventional antidepressants simply cannot replicate.

The FDA noticed. In 2019 they approved a ketamine-based nasal spray called Spravato for treatment-resistant depression. It’s doing $2 billion in sales this year.

SPONSOR BREAK presented by OxfordClub*

How Mitt Romney Turned $450K Into Up to $100 Million (Tax-Free)

It wasn’t stocks. It wasn’t real estate. It was a little-known investment vehicle that turned Mitt Romney’s $450,000 into as much as $100 million and Peter Thiel used to turn $2,000 into $5 billion within two decades. Now, thanks to a new executive order, regular Americans can access the same type of investment. Get more details here >>

The Spectrum.

1 Psilocybin — from mushrooms.

The most studied. The closest to approval. Compass Pathways CMPS ( ▼ 2.38% ) is leading the race with COMP360, a pharmaceutical-grade synthetic version being tested for treatment-resistant depression, PTSD, and anorexia. They expect to be launch-ready by end of 2026 — potentially the first psychedelic formally approved by the FDA.

Their second late-stage trial met its primary endpoint earlier this year.

2 Ibogaine — from plants.

The one Trump specifically named in the executive order. Used in other countries to treat PTSD in veterans for years.

Governor Greg Abbott signed a $50 million Texas research bill in June 2025. !!!

!!! Controversial because of cardiovascular risks — irregular heart rhythms, linked to deaths in uncontrolled settings. Which is exactly why moving it into controlled clinical environments matters.

3 5-MeO-DMT — from the Sonoran Desert toad.

The God molecule. The one Tyson smoked.

GH Research GHRS ( ▼ 4.93% ) is developing an inhaled version called GH001 — effects within minutes, full session complete within an hour, early trials showed rapid reduction in depressive symptoms.

AtaiBeckley ATAI ( ▼ 1.53% ) , backed by Peter Thiel, is developing BPL-003, an intranasal version with similar rapid-acting results.

Both are advancing toward Phase 3 trials.

Three completely different substances. Three completely different mechanisms. All pointing in the same direction…

The Text Message.

So how did seventy years of history land on the president’s desk last Saturday?

Joe Rogan texted President Trump about ibogaine.

Trump read it. His response, from the Oval Office, with Rogan sitting next to him:

“Sounds great. Do you want FDA approval? Let’s do it.”

That’s the whole origin story of what is now official US government policy.

A text message.

And seventy years of underground medicine just got a fast pass to the front of the FDA queue.

FDA Commissioner Marty Makary announced priority review vouchers — dramatically accelerated approval timelines — would be issued to three psychedelic treatments this week.

Monday, the market didn’t wait for the details.

→ Compass Pathways +38.9%

→ AtaiBeckley +31%

→ GH Research +20.9%

→ Definium Therapeutics +9.7%

→ Enveric Biosciences +187%

!!! Institutional money is flooding into a space that has been dominated entirely by retail investors for years.

→ Deutsche Bank and Morgan Stanley have both initiated coverage of psychedelic biotechs — firms that wouldn’t have gone near this sector two years ago.

The toad sat in the mud for seventy years.

→ Scientists found it in the 1950s and called it medicine.

→ Politicians took it away in 1970 and called it dangerous.

→ Some people licked it anyway. (don’t do this)

→ The National Park Service told them to stop.

Last Saturday, the White House kissed it.

The prince is getting dressed.

Don’t forget to to cast your vote 👇

Lesson Of The Day:

Was this email forwarded to you? Don’t miss out on future stories — subscribe using the button below.

Also, help your friends blossom this spring! Share us with them.

💬 We Want To Hear Your Story:

Got a market or stock you want us to analyze next?

Just drop your request in the comments here.

P.S. – If you no longer want to receive occasional emails from us and you want to unsubscribe, click here 👉 “Unsubscribe” . Thank you!